AS-18 - Related Party Disclosures, Significant Influence, KMPs

As mandated by section 129 of the companies act, 2013 (“the Act”), every company needs to prepare its annual financial statements in compliance with the accounting standards notified under section 133 of the Act. The Central Government may prescribe the standards of accounting, as recommended by the Institute of Chartered Accountants of India, constituted under section 3 of the Chartered Accountants Act, 1949 (38 of 1949), in consultation with and after examination of the recommendations made by the National Financial Reporting Authority.

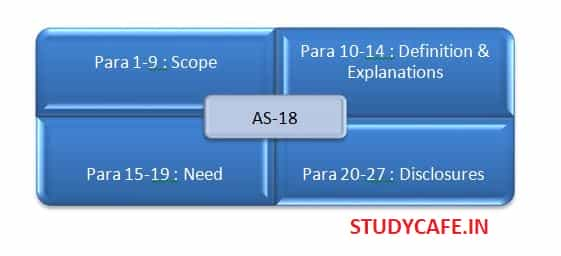

AS-18 has been notified in December, 2006 by the institute which needs to be complied by the companies while preparing their financials. Following is the bird eye view of the whole standard which needs to be understood before having the depth of the whole standard. Standard has 27 paragraphs which are divided as follows:

[caption id="attachment_86640" align="aligncenter" width="561"]

AS-18 - Related Party Disclosures, Significant Influence, KMPs[/caption]

SCOPE: PARA 1-9

Scope of this standard is not confined to standalone financials only, it is also mandatory for consolidated financial statements. This standard deals with following related party relationships:

| S. No. |

Related Party |

| (a) |

Holding Companies, Subsidiaries and Fellow Subsidiaries; |

| (b) |

Associates and Joint ventures; |

| (c) |

Individuals with voting power that gives them control or significant influence over the enterprise, and their relatives; |

| (d) |

KMPs and their relatives; |

| (e) |

Enterprises over which (c) or (d) has significant influence. |

And, following deemed not to be related parties as provided by para 4-

| S |

Not Related Party |

Exception |

| 1 |

Companies with common director; |

Director is able to affect the policies of both companies. |

| 2 |

Single customer, supplier, franchiser, distributor or general agent merely on account of economic dependence; |

NA |

| 3 |

Provider of finance, trade unions, public utilities, government departments and government agencies. |

NA |

Further, there are some matters which required no action under AS-18 which are as follows-

• Conflict with the duties of confidentiality as specifically required in terms of a statute or by any regulator or similar competent authority.

• In case a statute prohibits the enterprise to disclose certain information which is required to be disclosed as per this Standard.

• Intra-group transections in CFS.

• Transactions between members of a group in CFS.

• Relation of one state-controlled enterprise with other.

DEFINITIONS & EXPLANATIONS: PARA 10-14

a. Related Party-

If at any time during the reporting period one party has the ability to control the other party or exercise significant influence over the other party in making financial and/or operating decisions.

b. Control-

(i) Ownership, directly or indirectly, of more than one half of the voting power of an enterprise, or

(ii) Control of the composition of the governing body in case of any other enterprise, or

(iii) A substantial interest in voting power and the power to direct, by statute or agreement, the financial and/or operating policies of the enterprise.

c. Significant Influence-

Participation in the financial and/or operating policy decisions of an enterprise, but not control of those policies

d. Relatives-

In relation to an individual, means the spouse, son, daughter, brother, sister, father and mother who may be expected to influence, or be influenced by, that individual in his/her dealings with the reporting enterprise

e. Subsidiary-

In which another company (the holding company) holds, either by itself and/or through one or more subsidiaries, more than one-half in nominal value of its equity share capital; or

Of which another company (the holding company) controls, either by itself and/or through one or more subsidiaries, the composition of its board of directors

f. KMPs-

KMPs are those persons who have the authority and responsibility for planning, directing and controlling the activities of the reporting enterprise. It includes-

• Managing director(s)

• Whole time director(s)

• Manager(s)

• Person on whose direction BOD are accustomed to act.

• Non-executive directors of the company. (Specifically Excluded)

• Non-executive director if he has authority and responsibility for planning, controlling and directing the activities.

NEED: PARA 15-17

There is a General presumption that transactions are consummated on an arm’s length price. Operating results and financial position of an enterprise may be affected by a related party relationship. Operating results and financial position of an enterprise may be affected by a related party relationship. This may influence the decision of shareholders and stakeholders. So the disclosure of related party transection is required.

DISCLOSURES: PARA 20-27

1. Name of related party and nature of related party relationship,

• where control exist,

• Irrespective of having transactions or not.

2. If there have been transactions between related parties, then following disclosures required-

• Name of related party;

• Description of relationship between parties;

• Nature of transaction;

• Volume of transaction (Amount or an appropriate proportion);

• Other elements of transaction, necessary for understanding of financial Statements;

• Outstanding balances and provisions at balance sheet date;

• Amounts written off or written back.

Items of a similar nature may be disclosed in aggregate by “related party relationships” except when separate disclosure is necessary for an understanding of the effects of related party transactions on the financial statements of the reporting enterprise.

Examples of transactions related to AS-18 - Related Party Disclosures -

• Purchases or sales of goods,

• Purchases or sales of fixed assets,

• Rendering or receiving of services,

• Agency arrangements,

• Leasing or hire purchase arrangements,

• Guarantees and collaterals,

• Management contracts including for deputation of employees

8

8