Assessments by the GST Department officers under GST Law, 2017

Assessments by the GST Department officers under GST Law, 2017 Dear Colleagues I am preparing article on ASSESSMENTS Under GST Law as I m ge

Assessments by the GST Department officers under GST Law, 2017

Dear Colleagues I am preparing article on ASSESSMENTS Under GST Law as I m getting many queries on the above subject. Now GSTN share of tax payers data from 01.07.2017 to 31.03.2019 to CGST, SGST officers. Based on that data GST officers will be issue notices and informed over phone for submission of records and conduct surprise visits under GST Scenario and ready to finalize the assessments. As a upcoming tax professionals you must know about the procedure of assessments under GST Scenario and what are the procedures followed by the Assessing officers under GST scenario as per section from 59 to 64 of the CGST Act, 2017. I will be preparing and providing notes on daily basis. Kindly provide your feedback on my mail i.d. [email protected] and whats app no. 9848099490.

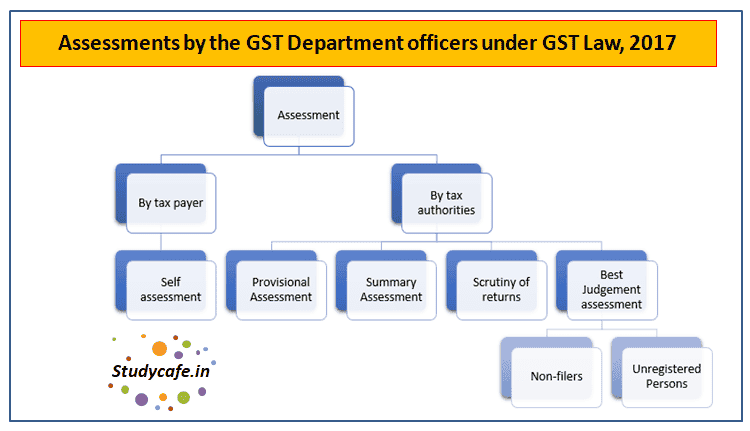

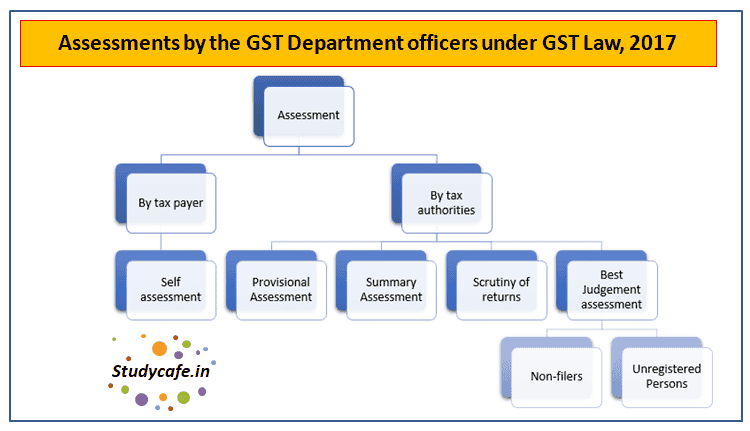

1. What is the meaning of Assessment under GST Law

As per Section 2(11) of CGST Act, 2017, "Assessments" means determining the tax liability under This Act and includes self-assessment, re-assessment, provisional assessment, summary assessment and best judgment assessment.

2. Self Assessment: As per Section 59 of the CGST Act, 2017, every registered person shall self-assess the taxes and payable under this Act and furnish a return for each tax period specified under section 39.

3. Provisional Assessment: As per Section 60 of CGST Act, 2017 subject to the provisions of sub-section (2), where the taxable person is unable to determine the value of goods or services or both or determine the rate of tax applicable thereto, he may request the proper officer in writing giving reasons for payment of tax on a provisional basis and the proper officer in writing giving reasons for pass an order, within a period not later than 90 days from the date of receipt of such request, allowing payment of tax on provisional basis at such rate or on such value as may be specified by him.

FROM GST ASMT-01: As per Rule 98(1) of the CGST Rules, 2017, states that every registered person requesting for payment of tax on a provisional basis in accordance with the provisions of sub-section (1) of section 60 shall furnish an application along with the document in support of his request, electronically in FORM GST ASMT-01 on the Common Portal, either directly or through GST Practitioner.

FORM GST ASMT-02: Notice to appear in person or furnish additional information/documents, as per 98(2) of the CGST Act, 2017, states that the proper officer may, on recipient of the application under sub-rule (1), issue a notice in FORM GST ASMT-02 requiring the registered person to furnish additional information or documents in support of his request and the applicant shall file a reply to the notice in FOR GST ASMT-03 and may appear in person before the said officer if he sodesires.

What are the records and documents to be submit before GST Officer for completion of Assessment under GST Law:

(a) Verification of records by GST Officer at the time of take up assessment for prepare audit notes:

The proper officer authorized to conduct of the records and books of account of the registered person shall with the assistance of the team of officers and officials accompanying him, verify the documents and statements furnished under the Act and rules made thereunder , to check the correctness of following:-

i. The turnover,

ii. Exemptions and deductions claimed,

iii. The rate of tax applied in respect of supply of goods or services,

iv. The input tax availed and utilized,

v. Refund claimed, proper officer and his team will examine other relevant issued ad record the observations in is audit notes.

(b) To afford the necessary facility to verify the books of accounts or other documents he may require,

The taxable person submit these following records to GST officer:

i) Cash book for the audit period mentioned by the audit officer in said notice,

ii) Ledger of inward supply of goods, services,

iii) Ledger of out ward supply of goods, services,

iv) Returns forms like GST Form 3B, GSTR-1, GSTR-2 and GSTR-3 and GSTR-4 etc., maintained by the taxable person as per GST Act, Maintenance of Records Rules,

v) Payments challans,

vi) Ledger of Bank account,

vii) Details of E way bill for the audit period for inward and out ward supply of goods and services,

viii) GST registration certificate details like principle place of business, branch and other place of details whether incorporate or not,

ix) Ledger of stock maintained at Where house by the taxable person,

x) Trial Balance for the audit period and Profit and Loss Account,

xi) Copy and details of Trans-1, Trans-2 and 2A and Trans-3 etc., for the year 2017-18 along with stock register and copies of original invoice relating to ITC claimed in Trans-1 for the period prior to July 2017 as per Sec. 143 of CGST Act, 2017.

Form and manner of issuance of order:

As per Rule 98(3) of CGST Act,2017 ,that the proper officer shall issue an order in FORM GST ASMT-04 , allowing payment of tax on a provisional basis indicating the value or the rate or both on the basis of which the assessment is to be allowed on a provisional basis and the amount for which the bond is to be executed and security to be furnished not exceeding twenty five percent, of the amount covered under the bond.

Bond with security:

As per sec.60(2) of the CGST Act,2017, the payment of tax on provisional basis may be allowed, if the taxable person executes a bond in such form as may be prescribed and with such surety or security as the proper officer may deem fir, binding the taxable person for payment of the difference between the amount of tax as may be finally assessed and the amount of tax provisionally assessed.

Rule 98(4) of the CGST Act,2017, the registered person shall execute a bond in accordance with the provisions of sub-section (2) of section 60 in FORM GST ASMT-05 along with a security in the form of a bank guarantee for an amount as determined under sub-rule (3).

Provided that a bond furnished to the proper officer under the CGST SGST//UTGST/IGST Acts shall be deemed to be a bond furnished under the provisions of this Act and the rules made thereunder.

Explanation:- For the purpose of this rule, the term amount shall include the amount of integrated tax, central tax, State tax, or Union territory tax and cess payable in respect of the transaction.

Time Limit for passing final order:

As per section 60(3) of the CGST Act,2017 the proper officer shall, within a period not exceeding six months from the date of the communication of the order issued under sub-section (1), pass the final assessment order after taking into account such information as may be required for finalizing the assessment.

Provided that the period specified in this sub-section may, on sufficient cause being shown and for reasons to be recorded in writing, be extended by the Joint Commissioner or Additional Commissioner for a further period not exceeding six months and by the Commissioner for such further period not exceeding four years.

As per Rule 98)5) of the CGST Act,2017, the proper officer shall issue a notice in FORM GST ASMT-06, calling for information and records required for finalization of assessment under sub-section (3) of section 60 and shall issue a final assessment order, specifying the amount payable by the registered person or the amount refundable, if any in FORM GST ASMT-07.

As per rule 98(6) of the CGST Act,2017, the applicant may file an application in FORM GST ASMT-08 for release of security furnished under sub-rule (4) after issue of order under sub-rule (5).

As per rule 98(7) of CGST Act, 2017, the proper officer shall release the security furnished under sub-rule (4), after ensuring that the applicant has paid the amount specified in sub-rule (5) and issue an order in FORM GST SMT-09 within a period of seven working days from the date of receipt of the application under sub-rule(6).

Payment of Interest:

As per section 60(4) of the CGST Act, 2017, the registered person shall be liable to pay interest on any tax payable to pay interest on any tax payable on the supply of goods or services or both under provisional assessment but not paid on the due date specified under subsection (7) of section 39 or the rules made thereunder, at the rate specified under sub-section (1) of section 50, from the first day after the due date of payment of tax in respect of the said supply of goods or services or both till the date of actual payment, whether such amount is paid before or after the issuance of order for final assessment.

Refund:

As per section 60(5) of the CGST Act, 2017, where the registered person is entitled to a refund consequent to the order of final assessment under sub-section (3) , subject to the provisions of sub-section (8) of section 54, interest shall be paid on such refund as provided in section 56.

Scrutiny of Returns:

As per sec.61 of the CGST Act, 2017, provides:-

(1) The proper officer may scrutinize the return and related particulars furnished by the registered person to verify the correctness of the return and inform him of the discrepancies noticed if any, in such manner as may be prescribed ad seek his explanation thereto.

(2) In case the explanation is found acceptable , the registered person shall be informed accordingly and no further action shall be taken in this regard.

(3) In case no satisfactory explanation is furnished within a period of thirty days of being informed by the proper officer or such further period as may be permitted by him or where the registered person, after accepting the discrepancies , fails to take the corrective measure in his return for the month in which the discrepancy is accepted, the proper officer may initiate appropriate action including those under sec. 65 or sec. 66 or sec. 67, or proceed to determine the tax and other dues under sec. 73 or sec. 74.

Manner of Scrutiny of Returns:

As per rule 99 of the CGST Rules, 2017 provides for the manner of scrutiny of returns:-

(1) Where any return furnished by a registered person is selected for scrutiny , the proper officer shall scrutinize the same in accordance with the provisions of section 61 with reference to the information available with him, and in case of any discrepancy, he shall issue a notice to the said person in FORM GST ASMT-10, informing him of such discrepancy and seeking his explanation thereto within such time , not exceeding thirty days from the date of service of the notice or such further period as may be permitted by him and also, where possible, quantifying the amount of tax, interest and any other amount payable in relation to such discrepancy.

(2) The registered person may accept the discrepancy mentioned in the notice issued under sub-rule (1) , and pay the tax, interest and any other amount arising from such discrepancy and inform the same or furnish an explanation for the discrepancy in FORM GST ASMT-11 to the proper officer.

(3) Where the explanation furnished by the registered person or the information submitted under sub-rule (2) is found to be acceptable, the proper officer shall inform him accordingly in FORM GST ASMT-12.

Assessment of Non-Fillers of GST Return:

As per Section 62 of the CGST Act, 2017 provides :-

(1) Notwithstanding anything to the contrary contained in sec. 73 or sec. 74, where a registered person fails to furnished the return under sec. 39 or sec. 45, ever after the service of a notice under sec. 46, the proper officer may proceed to assess the tax liability of the said person to the best of his judgment taking into account all the relevant material which is available or which he has gathered and issue an assessment order within a period of five years from the date specified under sec. 44 or furnishing of the annual return for the financial year to which the tax not paid relates.

(2) Where the registered person furnishes a valid return within thirty days of the service of the assessment order under sub-section(1), the said assessment order shall be deemed to have been withdrawn but the liability for payment of interest under sub-section () of section 50 or for the payment of late fee under sec. 47 shall continue.

(3) As per rule 100(1) of CGST Act, 2017, The order of assessment made under sub-section (1) of section 62 shall be issued in FORM GST ASMT-12.

Assessment of Unregistered Person in GST:

As per section 63 of the CGST Act,2017, provides:-

Notwithstanding anything to the contrary contained in section 73 or sec.74, where a taxable person fails to obtain registration even though liable to do so or whose registration has been cancelled under sun-section (2) of section 29 but who was liable to pay tax, the proper officer may proceed to assess the tax liability of such taxable person to the best of his judgment for the relevant tax periods and issue an assessment order within a period of five years from the date specified under section 44 for furnishing of the annual return for the financial year to which the tax not paid relates:

Provided that no such assessment order shall passed without giving the person an opportunity of being heard .

As per Rule 100(2) of CGST Act,2017,the proper officer shall issue a notice to a taxable person in accordance with the provisions of sec.63 in FORM GST ASMT-14 containing the grounds on which the assessment is proposed to be made on best judgment basis and after allowing a time of fifteen days o such person to furnish his reply if any, pass an order in FOR GST ASMT-15.

Summary of Assessment in Certain Cases:

As per sec.64(1) of CGST Act, 2017, the proper officer may, on any evidence showing a tax liability of a person coming to his notice , with the previous permission of Additional Commissioner or Joint Commissioner, proceed to assess the tax liability of such person to protect the interest of revenue and issue an assessment order, if he has sufficient grounds to believe that any delay in doing so may adversely affect the interest of revenue.

Provided that where the taxable person to whom the liability pertains is not ascertainable and such liability pertains to supply of goods, the person in charge of such goods shall be deemed to be the taxable person liable to be assessed and liable to pay tax and any other amount due under this section.

As per Rule 100(3) of CGST Act,2017, The order of summary assessment under sub-section(1) of section 64 shall be issued in FROM GST ASMT-16.

As per sec.64(2) of the CGST Act,2017, provides that on application made by the taxable person within thirty days from the date of receipt of order passed under sub-section (1) or on his own motion, if the Additional Commissioner or Joint Commissioner considers that such order is erroneous, he may withdraw such order and follow the procedure laid down in section 73 or section 74.

As per rule 100(5) of CGST Act,2017,The person referred to in sub-section (2) of section 64 may file an application for withdrawal of the summary or, as the case may be, rejection of the application under sub-section (2) of section 64 shall be issued in FORM GST ASMT-18.

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

Dear Professional colleagues, I have completed my notes on "ASSESSMENTS" under various sections under GST Law, 2017.

Wish you all the best

With Best Regards,

B.S.Seethapathi Rao Chairman,

AIFTP (Southern Zone)

About Author

B.S. Seethapathi Rao

Author

13

13My Recent Articles

- Tax Practitioner Fraternity under threat - Problems & solutions

- Transfer of development rights or long term lease by landowner to promoter GST Scenario

- Grievance Redressal on implementation of GST Law

- Real Estate Services involving in owned or leased property under GST Scenario

- Role of the Practitioner in Business Society under GST Scenario

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts