Presentation on GST Annual Return Containing complete analysis of GSTR-9

Presentation on GST Annual Return Containing complete analysis of GSTR-9 RELEVANT SECTION, RULE, NOTIFICATIONS AND ORDERS Relevant Section:

Presentation on GST Annual Return Containing complete analysis of GSTR-9

RELEVANT SECTION, RULE, NOTIFICATIONS AND ORDERS

Relevant Section: Section 44 read with Rule 80

Relevant Notification: Notification No. 74/2018-Central Tax Dated 31st December 2018

Order No. 1/2018 - Central Tax- Removal of difficulty order regarding extension of due date for filing of Annual return (in FORMs GSTR-9, GSTR-9A and GSTR-9C) for FY 2017-18 till 31st March, 2019

Order No. 2/2018 - Central Tax- Seeks to extend the due date for availing ITC on the invoices or debit notes relating to such invoices issued during the FY 2017-18

Order No. 3/2018 - Central Tax- Seeks to amend Removal of Difficulty Order No. 1/2018 dated 11.12.2018 so as to extend the due date for furnishing of annual returns in FORM GSTR-9, FORM GSTR-9A and reconciliation statement in FORM GSTR-9C for the FY 2017-2018 till 30.06.2019.

GST Annual Return Containing complete analysis of GSTR-9

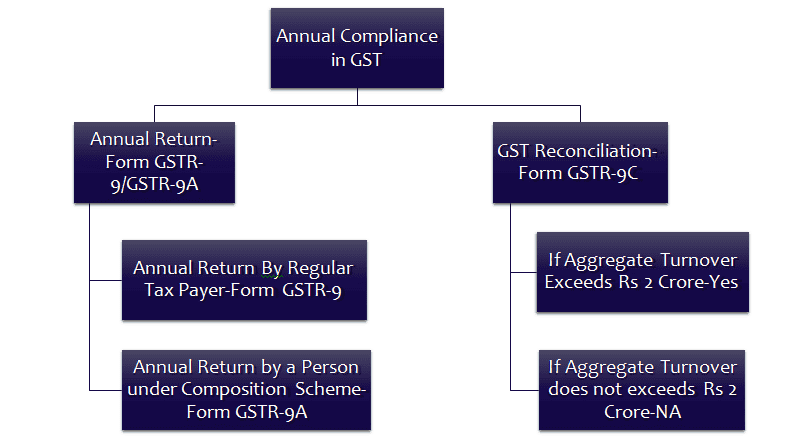

RELEVANT FORMS FOR THE PURPOSE OF ANNUAL RETURN AND RECONCILIATION FORMAT

a) GSTR-9 - Annual Return

b) GSTR-9A - Annual Return for (Composition Tax Payers)

c) GSTR-9C - Reconciliation Statement

WHO IS NOT REQUIRED TO FILE ANNUAL RETURN

1) Input Service Distributor,

2) A person paying tax under section 51 or section 52,

3) A casual taxable person and

4) A non-resident taxable person

5) Department of Central Government or State Government or local authority, whose books of account are subject to audit by the Comptroller and Auditor-General of India or an auditor appointed for auditing the accounts of local authorities under any law for the time being in force.

-

Presentation on GST Annual Return Containing complete analysis of GSTR-9

RELEVANT SECTION AND RULE

SECTION 44(1) ANNUAL RETURN

Every registered person, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non- resident taxable person, shall furnish an annual return for every financial year electronically in such form and manner as may be prescribed on or before the thirty-first day of December following the end of such financial year.

RULE 80(1) ANNUAL RETURN

Every registered person other than those referred to in the proviso to sub-section (5) of section 35, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non-resident taxable person, shall furnish an annual return as specified under sub-section (1) of section 44 electronically in FORM GSTR- 9 through the common portal either directly or through a Facilitation Centre notified by the Commissioner:

Provided that a person paying tax under section 10 shall furnish the annual return in FORM GSTR-9

Some FAQ's on GST Annual Return

| Q. N | Question | Answer |

| 1 | Is this return to be furnished by person whose registration has been cancelled during the year 2017-18 | Yes, Annual return would have to be furnished by a person whose registration has been cancelled during the Year 2017-18. Further, if a person had applied for cancellation of registration and his application for cancellation of registration was pending as on 31st March 2018, he also would be required to file Annual Return. |

| 2 | Is Annual return to be filed by the person who had migrated to GST Regime provisionally but they had not cancelled their registration by filing REG-29 under Rule 24(4) of the CGST Rules, 2017 with effect from 1st July 2017 | No, such persons would not be required to file Annual Return for the Year 2017-18. |

| 3 | Whether Annual Return can be filed without filing GSTR-1 and GSTR-3B for the Year 2017-18 | No, it is mandatory to file FORM GSTR-1 and FORM GSTR-3B for FY 2017-18 before filing Annual return in FORM GSTR-9 |

| 4 | Whether any additional liability can be declared through GSTR-9 | Yes, Additional liability for the FY 2017-18 not declared in FORM GSTR-1 and FORM GSTR-3B may be declared in this return (Instruction 3) |

| 5 | Whether any additional input tax credit can be claimed through GSTR-9 | No, taxpayers cannot claim input tax credit unclaimed during FY 2017-18 through this return (Instruction 4) |

| 6 | How would Annual Return be filed by a person who was under composition scheme for part of year and under regular scheme for remaining part of the Year | Such persons would have to file GSTR-9 for the period under which they were under Regular Scheme and GSTR-9A for the period under which they were composition scheme. |

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.