Reversal of Input Tax Credit-real Estate Sector

Reversal of Input Tax Credit-real Estate Sector As you are aware that implementation of Goods and Services Ac,2017 (GST) is one of the most important…

Table of Contents

Reversal of Input Tax Credit-real Estate Sector

As you are aware that implementation of Goods and Services Ac,2017 (GST) is one of the most important act of this NDA Government. Through implementation of GST the concept “ One Tax one Nation” has been fulfilled and the tax system of India has been totally overhauled. We know that before its implementation there are number of central and state acts which govern business transactions, each state has its own Sales tax, Entertainment tax, Luxury Tax, Cess, VAT, Octroi, etc. The rates , the procedures, the book keeping methods etc. are different in each state. This was very hard to handle for the traders. There are a lot of compliances and submission of returns in various laws and the officers of the department were given more power or collection and Levy of taxes. There was tax on taxes , producing cascading effect , since on manufacture or production of any product , excise duty was first levied and then after ,when product reached in the market, the state governments levied VAT, Sales Tax etc.

The GST has removed above lacunas of previous acts and has brought a seamless process of flow of Input tax credit (ITC) at all stages of manufacturing/production/ sale of goods and provision of services. The ITC concept of GST is the most appreciated and welcome concept ,given much awaited relief to the persons engaged in the business or trading. The GST has brought down the rate of taxes applicable in old regime and help in furtherance of ease of doing business.

The main feature of GST Act,2017 is seamless or continuous flow of Input Tax Credits at each stage of supply of goods and services. Since GST if a consumption based that it means that the supply under GST will be taxable in the state in which goods are consumed or services are utilized. The Government through GST Act,2017 trusted the persons engaged in the business to self -assess and submit GST with the government after utilizing all available Input tax they have paid on input goods and services utilized to produces output goods and services. But there should be some checks ,so that above provisions should not be mis utilized.

LET’S CONSIDER A QUESTION FOR MORE UNDERSTANDING OF REVERSAL OF ITC:

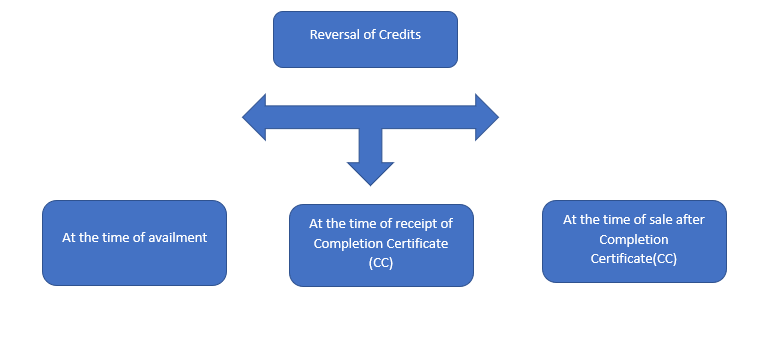

The Above three possible events which May attracts reversal;

The Above three possible events which May attracts reversal;

(c) How does intention to use make a difference?

Section 16(1) allows credit of tax charged on inputs used or intended to be used for making taxable supplies. The word,” used” also covers the intention to use. However the machinery provisions i.e. Rule 42 of CGST Rules, 2017 mentioned that reversal is required only for those inputs which are intended to be used for the purpose other than taxable supplies.

We can interpret above provisions that no reversal of Input Tax Credit is required if same has been used or intended to be used in past for supplies of taxable goods and services. The intention theory is applied only in cases, where input tax credits were used for supplies of taxable as well as exempt goods or services. The reversal should be done on prorate basis.

(d ) How to determine the amount of credit to be reversed in Real Estate Sector?

Rule 42- prescribed the method of reversal of common inputs. However the said method is not workable for Real Estate sector. The reversal of credit may be made based on the Square Feet Area, sold after and before receiving of Completion Certificate (CC).

LET’S CONSIDER AN EXAMPLE: Lets consider total area of a project be 10,000 Sq.Ft. Out of this 5000 Sq.Ft., is sold before receipt of Completion Certificate. In this scenario the available ITC is restricted to 50% whereas remaining 50% shall be subject to reversal.

(e ) When the material is given to a contract laborer for job work, whether credit is to be reversed?

According to the provisions of Section 19(1), the principal is allowed the credit of inputs sent to job work.

Section 19(3) of CGST Act,2017- provides that any supply of goods to a job worker would be treated as supply if it is not received back by the principal within stipulated time of one year.

Section 143 provides that a principal may send any inputs or capital goods without payment of tax , to a job worker under an intimation and conditions as may be prescribed.

Section 2(68) of CGST Act,2017- defines Job Work as “ Job Work” means any treatment or process undertaken by a person on goods belonging to another registered person and the expression “ Job Worker” shall be construed accordingly.

(c) How does intention to use make a difference?

Section 16(1) allows credit of tax charged on inputs used or intended to be used for making taxable supplies. The word,” used” also covers the intention to use. However the machinery provisions i.e. Rule 42 of CGST Rules, 2017 mentioned that reversal is required only for those inputs which are intended to be used for the purpose other than taxable supplies.

We can interpret above provisions that no reversal of Input Tax Credit is required if same has been used or intended to be used in past for supplies of taxable goods and services. The intention theory is applied only in cases, where input tax credits were used for supplies of taxable as well as exempt goods or services. The reversal should be done on prorate basis.

(d ) How to determine the amount of credit to be reversed in Real Estate Sector?

Rule 42- prescribed the method of reversal of common inputs. However the said method is not workable for Real Estate sector. The reversal of credit may be made based on the Square Feet Area, sold after and before receiving of Completion Certificate (CC).

LET’S CONSIDER AN EXAMPLE: Lets consider total area of a project be 10,000 Sq.Ft. Out of this 5000 Sq.Ft., is sold before receipt of Completion Certificate. In this scenario the available ITC is restricted to 50% whereas remaining 50% shall be subject to reversal.

(e ) When the material is given to a contract laborer for job work, whether credit is to be reversed?

According to the provisions of Section 19(1), the principal is allowed the credit of inputs sent to job work.

Section 19(3) of CGST Act,2017- provides that any supply of goods to a job worker would be treated as supply if it is not received back by the principal within stipulated time of one year.

Section 143 provides that a principal may send any inputs or capital goods without payment of tax , to a job worker under an intimation and conditions as may be prescribed.

Section 2(68) of CGST Act,2017- defines Job Work as “ Job Work” means any treatment or process undertaken by a person on goods belonging to another registered person and the expression “ Job Worker” shall be construed accordingly.

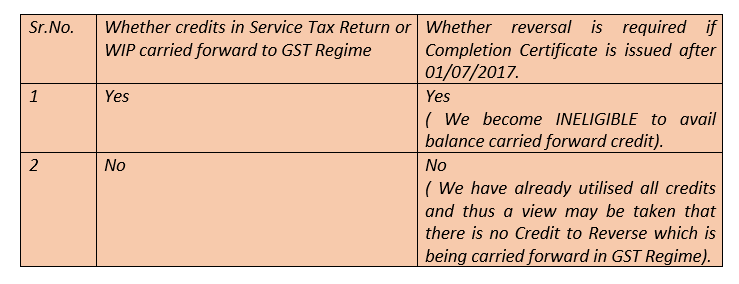

- A , a developer has sold the part units before completion certificate and part units after receipt of Completion Certificate of its residential project. Describe the provisions regarding reversal of input tax credit in case of common inputs attributable to taxable as well as non taxable supplies ?

- The recipient fails to pay consideration to the supplier (whether fully or partly) for a particular supply. (Rule 37 of CGST Rules);

- ITC has been availed on ‘blocked credits’ as per Section 17(5) of CGST Act.

- Inputs have been used to make a full or partial exempt supply or supply which is not for business purpose or used for personal consumption. (Rule 42 of CGST Rules).

- Inputs used in goods that were given out as free samples or used in goods that were lost, destroyed, stolen, etc.

- Cancellation of GST registration or switches to Composition Scheme. (Rule 44 of CGST Rules).

- Inputs taken on Capital Goods for supply of wholly exempt goods or taxable and exempt goods. (Rule 43 of CGST Rules)

- Depreciation under the Income Tax Act has been claimed on the GST component of capital goods purchased.

- Reversal of 50% of ITC by banking and other financial companies under special rules.

- Credit note issued to Input Service Distributor(ISD). (Rule 39 of CGST Rules).

- Reversal of ITC under Rule 37:You being a recipient, if you fail to pay the invoice amount to the supplier within 180 days the ITC has to be reversed. If part of the invoice is paid the ITC will be reversed on a proportionate basis.

- Reversal of ITC under Rule 42 & 43:Both rules pertain to reversal of Inputs utilized for supplies that are exempt or used for personal consumption. If the credit can specifically be attributable to a supply – either taxable, non- taxable, or supply consumed for personal use, such ITC amount should be distinguished from the total ITC since it can be easily identified. Taxpayer must reverse that amount of ITC directly attributable to a particular supply that is non-taxable/used for personal consumption, only when wrongly availed.

a) Inputs or input services- covered by Rule 42.

b) Capital goods- covered by Rule 43.

Reversal of ITC under Rule 44: The aim of this rule is to reverse all the ITC that has been availed by a registered person in the event that he chooses to pay tax under the composition scheme or his registration gets cancelled for any reason. For inputs held in stock or contained in semi-finished goods and finished goods in stock, the ITC which is to be reversed should be calculated proportionate to corresponding invoices on which credit was taken. In case of capital goods, ITC availed will be based on the useful life (in months) and shall be computed on a pro-rata basis. Reversal of ITC the availment of which is blocked under Section 17(5): Inputs on goods or services used for personal consumption, inputs on goods which are lost, stolen, destroyed or written off or disposed of by way of gift or free samples, and any ITC availed which is blocked as per Section 17(5) needs to be reversed by the recipient. INTEREST ON REVERSAL OF ITC Chapter X of the CGST Act, 2017 enumerates the provisions relating to ‘payment of tax’. Section 50 in this Chapter lays down the circumstances in which interest would be required to be paid. The Section provides for payment of interest in two circumstances: -- Where a person liable to pay tax fails to pay the same [Section 50(1)].

- Where a person makes an undue or excess claim of input tax credit under the provisions relating to matching of ITC [Section 50(3)].

- Inputs intended to be used exclusively for the purpose other than business.

- Inputs intended to be used exclusively for exempt supply.

- Inputs partly used for business and partly for other purposes.

- Inputs partly used for effecting taxable supplies including zero rated supply and partly used for effecting exempt supplies.

- Inputs INELIGIBLE to claim as credit as per Section 17(5) i.e. Blocked Credits.

- Common Credit in proportion of turnover from the business of exempt supplies. Turnover has to be seen for the tax period for which input tax credit is to be calculated.

- 5% of Common Credits shall be deemed to be attributed to non-business purposes, if common imputes are used for non-business purposes.

The Above three possible events which May attracts reversal;

- At the time of availment of credit , one cannot judge that inputs are to be consumed whether in effecting exempt or non-taxable supplies. Therefore , it is not possible to reverse credit at the time of availment.

- Time of receipt of Completion Certificate is a reasonable time to reverse credit availed earlier. The logic behind this is that the law requires requires reversal, when we use or intend to use the inputs for effecting other than taxable supplies. When we receive Completion Certificate , we cannot intend to use inputs for effecting taxable supplies. Further Credit Reversal is required to be made on a tax period basis therefore ,we may reverse credit in the period in which Completion Certificate is received.

- Reversing Credit at the time of sale of units may additionally attract levy of interest as mentioned above.

(c) How does intention to use make a difference?

Section 16(1) allows credit of tax charged on inputs used or intended to be used for making taxable supplies. The word,” used” also covers the intention to use. However the machinery provisions i.e. Rule 42 of CGST Rules, 2017 mentioned that reversal is required only for those inputs which are intended to be used for the purpose other than taxable supplies.

We can interpret above provisions that no reversal of Input Tax Credit is required if same has been used or intended to be used in past for supplies of taxable goods and services. The intention theory is applied only in cases, where input tax credits were used for supplies of taxable as well as exempt goods or services. The reversal should be done on prorate basis.

(d ) How to determine the amount of credit to be reversed in Real Estate Sector?

Rule 42- prescribed the method of reversal of common inputs. However the said method is not workable for Real Estate sector. The reversal of credit may be made based on the Square Feet Area, sold after and before receiving of Completion Certificate (CC).

LET’S CONSIDER AN EXAMPLE: Lets consider total area of a project be 10,000 Sq.Ft. Out of this 5000 Sq.Ft., is sold before receipt of Completion Certificate. In this scenario the available ITC is restricted to 50% whereas remaining 50% shall be subject to reversal.

(e ) When the material is given to a contract laborer for job work, whether credit is to be reversed?

According to the provisions of Section 19(1), the principal is allowed the credit of inputs sent to job work.

Section 19(3) of CGST Act,2017- provides that any supply of goods to a job worker would be treated as supply if it is not received back by the principal within stipulated time of one year.

Section 143 provides that a principal may send any inputs or capital goods without payment of tax , to a job worker under an intimation and conditions as may be prescribed.

Section 2(68) of CGST Act,2017- defines Job Work as “ Job Work” means any treatment or process undertaken by a person on goods belonging to another registered person and the expression “ Job Worker” shall be construed accordingly.

LET’S SUMMARIZED ABOVE

- The Principal is supposed to avail the credit of goods sent to Job-Worker , if the goods after Job-Work is return of sold within the stipulated time of one year.

- If point (1) is not applicable ,that is the goods are not returned within stipulated time then, the supply from the principal to Job-Worker will be treated as supply, the principal will charge tax and the Job-Worker will get credit.

- CGST Amendment Act,2018 empowers the Commissioner to extend the time limit of one year in desired cases.

- In this case there is no need for reversal of input tax credits availed by the principal, because in second case mentioned above , the transfer of goods to the Job-Worker will be considered as supply and the Principal is liable to levy tax and on the other hand Job-Worker is eligible for Input Tax Credit.

- Please keep in mind the above provisions are applicable in case of only registered principal and not on unregistered.

- The Job-Worker may be registered or unregistered entity.

- for transfer of Capital goods , if the Capital Goods are of the nature specifies in provision provided above , then the tax shall be payable on transaction value determined as per provisions of Section 15 of the CGST Act, 2017.

- If the Capital Goods are of the nature not covered as mentioned in the proviso of section 18(6) then tax shall be payable as Specified as per Rule 44 given below.

Rule 44 (6) CGST Rules,2017

1) The amount of inputs tax credit relating to inputs held in stock, inputs contained in semi-finished and finished goods held in stock, and capital goods held in stock shall, for the purposes of subsection (4) of section 18 or sub-section (5) of section 29, be determined in the following manner, namely,-- for inputs held in stock and inputs contained in semi-finished and finished goods held in stock, the input tax credit shall be calculated proportionately on the basis of the corresponding invoices on which credit had been availed by the registered taxable person on such inputs;

- for capital goods held in stock, the input tax credit involved in the remaining useful life in months shall be computed on the pro-rata basis, taking the useful life as five years.

- Capital goods have been in use for 4 years, 6 month and 15 days.

- The useful remaining life in months= 5 months ignoring a part of the month

- Input tax credit is taken on such capital goods= C

- Input tax credit attributable to remaining useful life= C multiplied by 5/60

- Provided that where the amount so determined is more than the tax determined on the transaction value of the capital goods, the amount determined shall form part of the output tax liability and the same shall be furnished in FORM GSTR-1.

About Author

FCS DEEPAK P. SINGH

Manager Legal & Compliance

SBI GENERAL INSURANCE COMPANY LIMITED

SBI GENERAL INSURANCE COMPANY LIMITED Mumbai, Maharashtra, India

Mumbai, Maharashtra, India 53

53My Recent Articles

- Surveyor Cannot Apply Deductions Arbitrarily On Amount Of Assessed Loss: Supreme Court Of India

- Insurance Company Cannot Impose Condition That Will Impossible To Comply By Insured

- Mergers & Acquisitions- Under Provisions of ITA,1961

- The Disputes between Landlord & Tenant Governed by Transfer of Property Act 1882 are Arbitrable in Nature

- Damage Caused by the Insurers Taking Possession of Insured Premises & Judicial Opinions

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts