Assessment Against Deceased Person Invalid Despite Legal Heir Participation: ITAT:

Tribunal quashes assessment framed against deceased assessee despite department's prior knowledge of death.

Jurisdictional Defect Cannot be Cured Through Legal Heir Participation

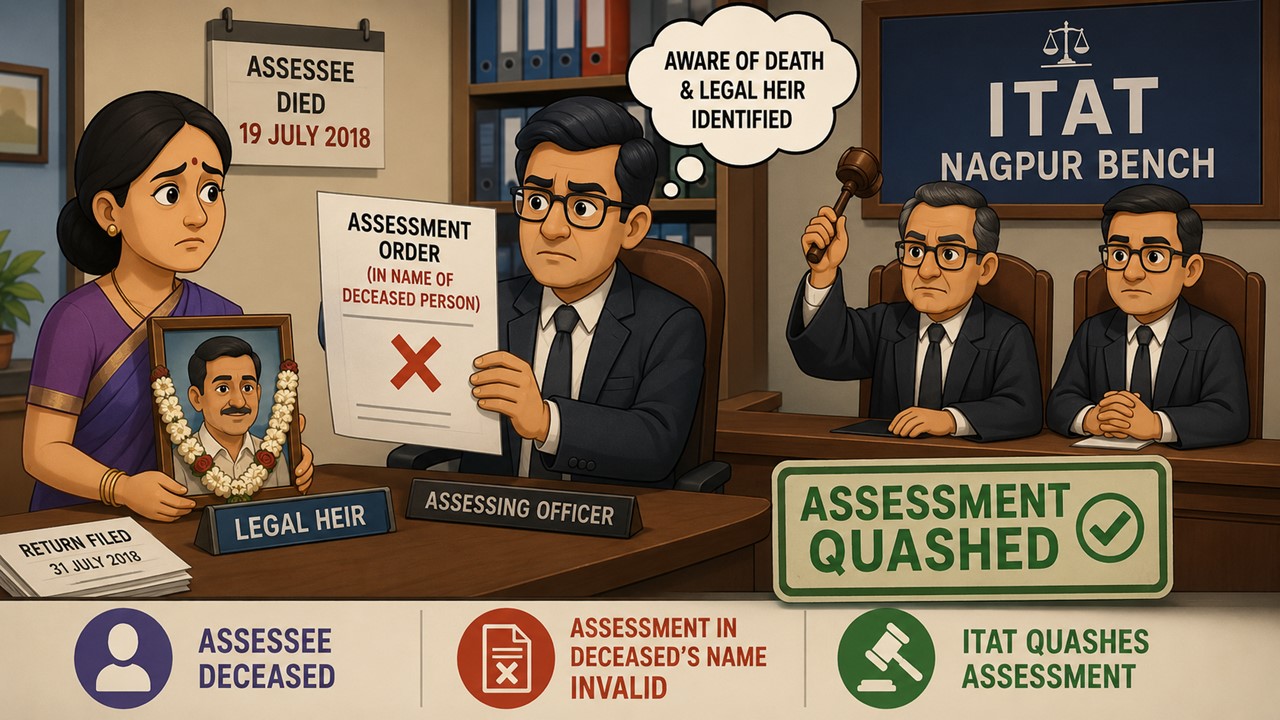

The Nagpur Bench of the Income Tax Appellate Tribunal (ITAT) has quashed an assessment order passed in the name of a deceased taxpayer, holding that once the Assessing Officer was aware of the death and the legal heir had been identified, completion of assessment in the deceased person's name was a jurisdictional defect that rendered the entire proceedings invalid.

The appeal was filed by Smt. Sunita Pankaj Patel, legal heir of late Shri Pankajbhai Natwarlal Patel, who was engaged in the business of financing through his proprietary concern, M/s Ganga Finances. The assessee had died on 19 July 2018, while the return of income for AY 2018-19 was filed on 31 July 2018. Subsequently, scrutiny proceedings were initiated and an assessment order under Section 143(3) was passed in the name of the deceased taxpayer. The CIT(A) later upheld the assessment.

Before the Tribunal, the legal heir challenged the validity of the assessment on the ground that both the notice and assessment order had been issued in the name of a dead person. The Revenue argued that the legal heir had participated in the proceedings without objection and that the defect was merely technical, as the legal heir’s name appeared in the annexures to the notices. It was also contended that the proceedings were effectively conducted against the legal heir and that the error in the name arose due to technical glitches.

The Tribunal rejected the Department’s stand. It noted that the Assessing Officer was fully aware of the assessee’s death and had even recorded in the assessment order that the case was transferred from the National Faceless Assessment Centre for bringing legal heirs on record. The widow, Smt. Sunita Patel, had also furnished her consent to represent the estate as legal heir.

The Bench observed that although the Department attempted to justify the notices by referring to technical issues, the assessment itself had ultimately been completed in the name of the deceased person and even the demand notice was issued against the deceased. Such a defect could not be treated as a mere procedural irregularity or an error in caption.

The Tribunal further held that there is no statutory obligation upon legal heirs to intimate the death of the assessee. In any event, the Revenue was already aware of the death and had knowledge of the legal heirs before completing the assessment. Therefore, the jurisdictional defect went to the root of the matter and could not be cured by participation of the legal heir in the proceedings.

Thus, the Tribunal allowed the appeal and quashed the assessment order in its entirety without examining the additions made on merits.

To Read Full Order, Download PDF Given Below

About Author

Meetu Kumari

Content Manager

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2231

2231My Recent Articles

- ITAT Restricts Bogus Purchase Addition to 1.15% Profit Element Despite Seller DenialsPremium

- ITAT Upholds Reassessment, Rejects Challenge Over Absence of Section 143(2) NoticePremium

- High Court Quashes Section 148 Notice Based on Wrong Assessee's Investigation ReportPremium

- ITAT Allows Set-Off of Brought Forward Business Loss Against Section 50 Capital GainsPremium

- High Court Quashes Reassessment Based on Mere Change of Opinion After ScrutinyPremium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts