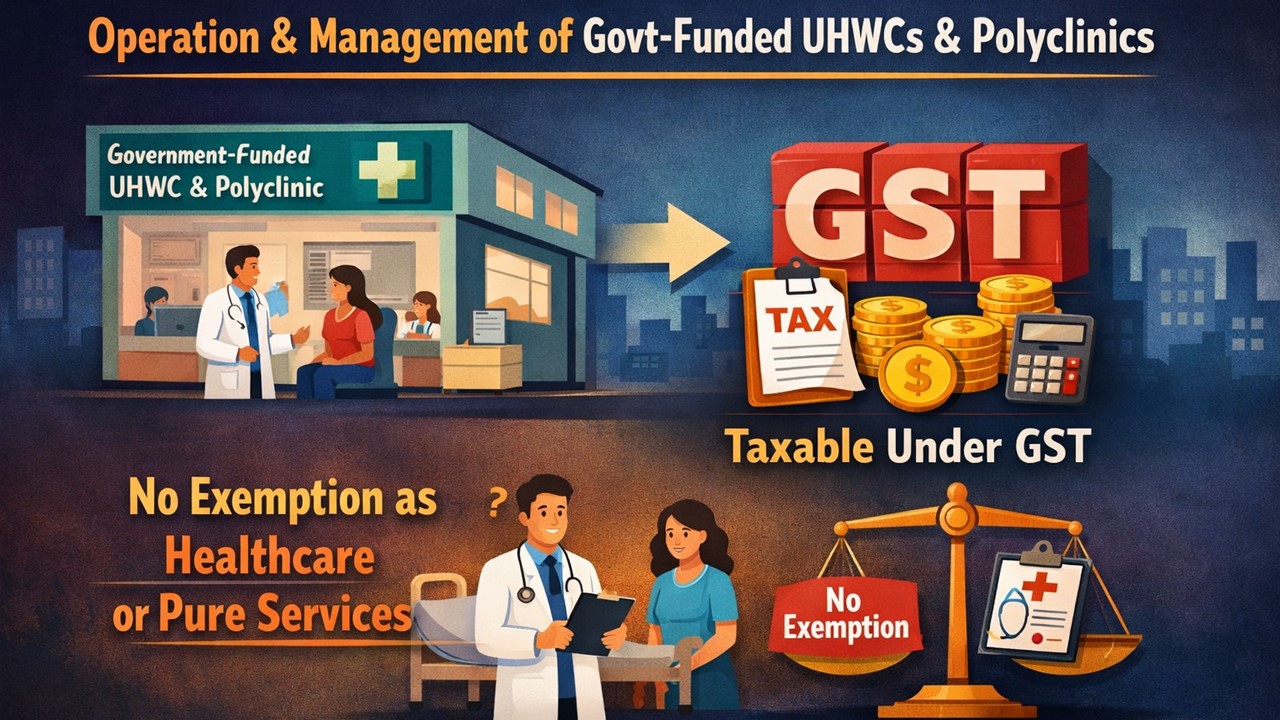

GST on Public Health Services: AAR Denies Exemption to UHWC and Polyclinic Services:

AAR rules that operation and management of government-funded UHWCs and polyclinics are taxable under GST, denying exemption as healthcare or pure services.

No GST Relief for Government-Funded Health Centres: AAR

GST on Public Health Services: AAR Denies Exemption to UHWC and Polyclinic Services

M/s Indovation Healthcare LLP has filed an application (No. 03/2025-26) seeking the Goods and Services Tax (GST) Authority for Advance Ruling (AAR) Uttarakhand under Sub-Section (1) of Section 97 of the Central Goods and Services Tax Act 2017 and Uttarakhand State Goods & Service Tax Act 2017. The authority received the application on December 20, 2025, and heard the matter on January 29, 2026. The applicant is registered under the GST Act and is located at F-79, Industrial Area, Bahadrabad, Haridwar, Uttarakhand 249402.

The applicant is involved in operating and handling the Government Urban Health and Wellness Centres (UHWCs) and Polyclinics in the State of Uttarakhand under a public healthcare programme funded by the government. The programme was implemented consequent to the 15th Finance Commission's suggestions. Government-owned facilities are used to provide these healthcare services. These services are completely funded by government health grants. The applicant provides primary healthcare services to the public at no cost, in adherence to the instructions of the Government of India.

Questions Asked by AAR Uttarakhand:

The following are the questions asked by the applicant seeking the AAR Uttarakhand:

"Question 1: Whether the operation and management of Government Urban Health & Wellness Centres (UHWCs) / Ayushman Arogya Mandirs and Polyclinics by the Applicant under identical Operation & Management Agreements with Braithwaite & Co. Ltd. (PSU-executing agency), funded exclusively through 15th Finance Commission health grants routed via Braithwaite and Company Limited and providing healthcare services to citizens free of cost, constitutes exempt 'healthcare services by a clinical establishment' under Entry 74 of Notification No. 12/2017-Central Tax (Rate)?

Question 2: Whether, in the alternative, the said activities qualify as "pure services" provided to the State Government (through its designated PSU executing agency under a formal MoU) in relation to Article 243W functions (public health, hospitals, dispensaries - Twelfth Schedule Entries 6, 8, 23) and are therefore exempt under Entry 3 of Notification No. 12/2017-Central Tax (Rate)?"

Answers Given by AAR Uttarakhand:

The following are the answers given by the AAR Uttarakhand to the questions asked by the applicant:

Answer 1: The running and managing of the Government Urban Health & Wellness Centres (UHWCs) / Ayushman Arogya Mandirs and Polyclinics by the applicant under identical Operation & Management Agreements with Braithwaite & Co. Ltd. (PSU-executing agency), which is entirely funded through 15th Finance Commission health grants, does not qualify for the "health care services by a clinical establishment" tax exemption under Entry 74 of Notification No. 12/2017-Central Tax (Rate).

Answer 2: The said activity also does not qualify as "pure services" provided to the State Government (through its designated PSU executing agency under a formal MoU) in accordance with Article 243W functions (public health, hospitals, dispensaries-Twelfth Schedule Entries 6, 8, 23) and are consequently not eligible for tax exemption under Entry 3 of Notification No. 12/2017-Central Tax (Rate).

In conclusion, the services provided by the applicant are GST payable under the CGST/SGST Acts.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2491

2491My Recent Articles

- ITAT Holds CIT(A) Cannot Dismiss Taxpayer’s Appeal Merely Over Non-Prosecution Without Merit HearingPremium

- ITAT Remands TDS Appeal After CIT(A) Failed to Decide Actual CAM Charges IssuePremium

- ITAT Rules in Taxpayer's Favour, Holds Delay in Filing Form 67 Cannot Be Sole Ground to Deny Foreign Tax CreditPremium

- ITAT Revives Tax Appeals for Six AYs After Finding Insufficient Hearing Time and Ignored Adjournment RequestPremium

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts