GST Rule 86B misconceptions, How Taxpayers are interpreting it wrongly

GST Rule 86B misconceptions, How Taxpayers are interpreting it wrongly As per GST Notification number, 94/2020-Central Tax dated 22nd Dec 2020, GST r…

GST Rule 86B misconceptions, How Taxpayers are interpreting it wrongly

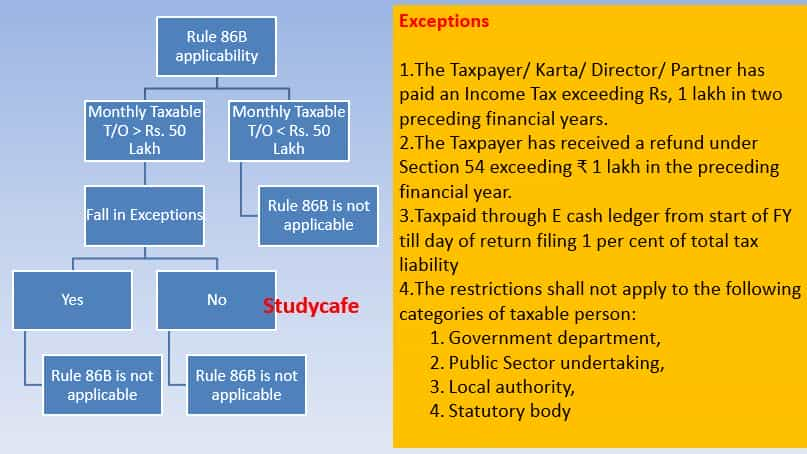

As per GST Notification number, 94/2020-Central Tax dated 22nd Dec 2020, GST rule 86B has been introduced which has imposed 99% restricted on ITC (Input Tax Credit) available in electronic credit ledger of Registered Person. This means 1% of Output liability to be paid in cash. This restriction is applicable in the case of Registered taxpayers having a monthly turnover of more than Rs. 50 Lakh.

This move is getting a large amount of criticism from the Taxpayers. There is a common myth, that everyone whose monthly turnover is more than Rs. 50 Lakh will fall under this rule. Through this article, let us try to understand the provisions more deeply and understand why these provisions were introduced.

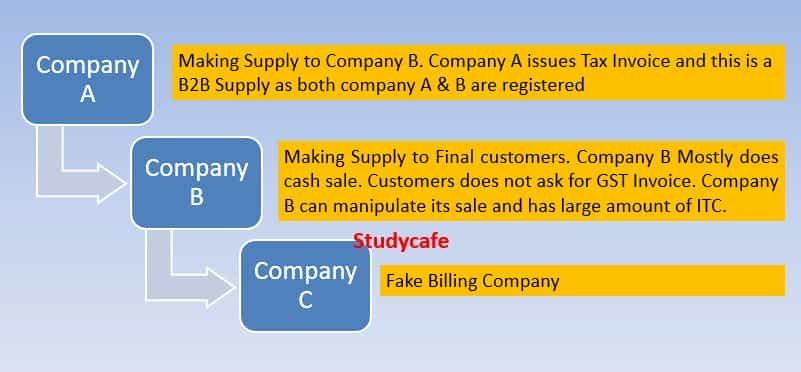

Firstly we need to understand that this rule has been introduced to curb the menace of Fake GST Invoicing. The practice of fake GST invoicing has made the entire GST ecosystem hollow.

Let us understand that who actually will come in clutches of rule 86B and why I am saying that genuine taxpayers will never fall in newly inserted Rule 86B.

For that, we need to understand the exceptions who will never fall in Rule 86B. [Proviso a to d of rule 86B of CGST Rules 2017]

Rule 86b exceptions

GST Rule 86B misconceptions, How Taxpayers are interpreting it wrongly[/caption]

In my opinion, the claim of the taxpayer rather seems suspicious.

I am not saying that everyone is wrong. There can be some genuine Taxpayers who are falling in the above-given situation:

GST Rule 86B misconceptions, How Taxpayers are interpreting it wrongly[/caption]

In my opinion, the claim of the taxpayer rather seems suspicious.

I am not saying that everyone is wrong. There can be some genuine Taxpayers who are falling in the above-given situation:

- The Taxpayer/ Karta/ Director/ Partner has paid an Income Tax exceeding Rs, 1 lakh in two preceding financial years.

- The Taxpayer has received a refund under Section 54 exceeding ₹1 lakh in the preceding financial year.

- The Taxpayer has paid outward tax liability in cash which cumulatively exceeds 1 per cent of total tax liability for the financial year till date.

- The restrictions shall not apply to the following categories of taxable person:

- Government department,

- Public Sector undertaking,

- Local authority,

- Statutory body

GST Rule 86B misconceptions, How Taxpayers are interpreting it wrongly[/caption]

In my opinion, the claim of the taxpayer rather seems suspicious.

I am not saying that everyone is wrong. There can be some genuine Taxpayers who are falling in the above-given situation:

- Startup having a large amount of loss and ITC on amount of huge capital expenditure.

- Taxpayers who are doing seasonal business or AMCs [Annual Maintenance Contracts]

- New Professions where billing instances are occasional. [For Example Newly Setup CA Firm]

- Company A is a genuine company selling goods to Company B. This is a B2B transaction and Company A issues tax invoice to Company B.

- Company B is having cash sales. Company B makes sales to retail customers, who don't need a tax invoice. Company B can manipulate it sales and has large amount of ITC.

- Company C is a fake company, involved in Fake GST Billing. Company B shows sale to company C. The Black money of Company B is converted to White and Company B uses it ITC to setoff its Liability. Company B manipulates its sale and never pays ITC in Cash. It also never shows profit in Income Tax.

- Company C also gets ITC and this fake ITC is passed to needy firms by company C.

- Rule 86 has been introduced to curb such practices that have made roots of GST Hollow.

क्या हम GST Rule 86B को सही Interpret कर रहे हैं?

Tags: GSTAbout Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts