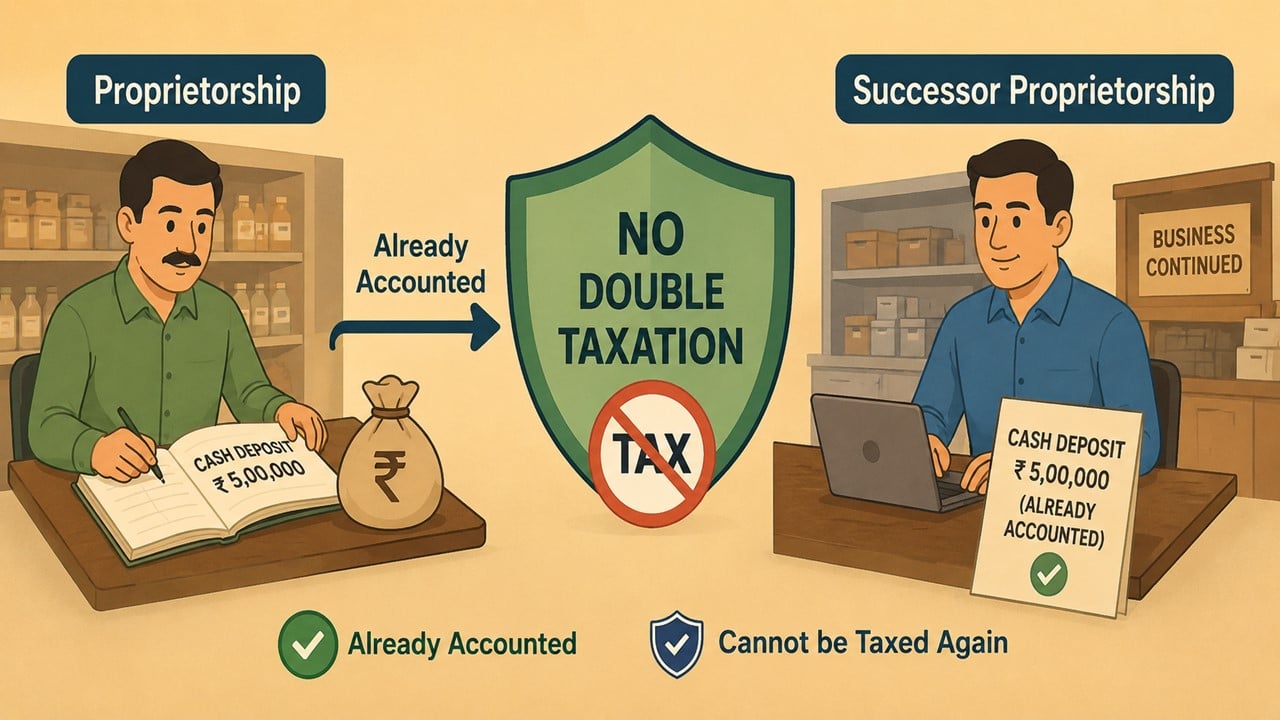

If Deposits Are Already Included in Proprietor’s Income, They Cannot Be Taxed Again: ITAT:

ITAT held that cash deposits already recorded and taxed in the successor proprietorship concern cannot be taxed again in the hands of the dissolved partnership firm and remanded the matter for verification.

ITAT Directs AO to Verify Taxability of Cash Deposits

Premium

If Deposits Are Already Included in Proprietor’s Income, They Cannot Be Taxed Again: ITAT

ITAT held that cash deposits already recorded and taxed in the successor proprietorship concern cannot be taxed again in the hands of the dissolved partnership firm and remanded the matter for verification.

Also Read

ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentITAT Allows Fresh Opportunity in Dispute Over Suppressed Sales and Commission ExpensesEarlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATITAT Deletes Rs 2.13 Crore Addition Under Section 68, Grants Major Tax Relief

About Author

Vanshika verma

Content Writer

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1636

1636My Recent Articles

- ITAT Allows Fresh Opportunity in Dispute Over Suppressed Sales and Commission ExpensesPremium

- ITAT Deletes Rs 2.13 Crore Addition Under Section 68, Grants Major Tax ReliefPremium

- ITAT: Protective Addition Cannot Survive After Substantive Assessment Is QuashedPremium

- ITAT Remands Rs 8.12 Crore Cash Withdrawal Disallowance Case to AO for Fresh AssessmentPremium

- ITAT Deletes Rs 1.20 Crore Disallowance on Business Development and Marketing ExpensesPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts