ITAT Allows Section 10AA Claim Despite Filing Wrong Form; Procedural Error Held Curable:

ITAT holds incorrect audit form filing is curable and cannot defeat eligible deduction.

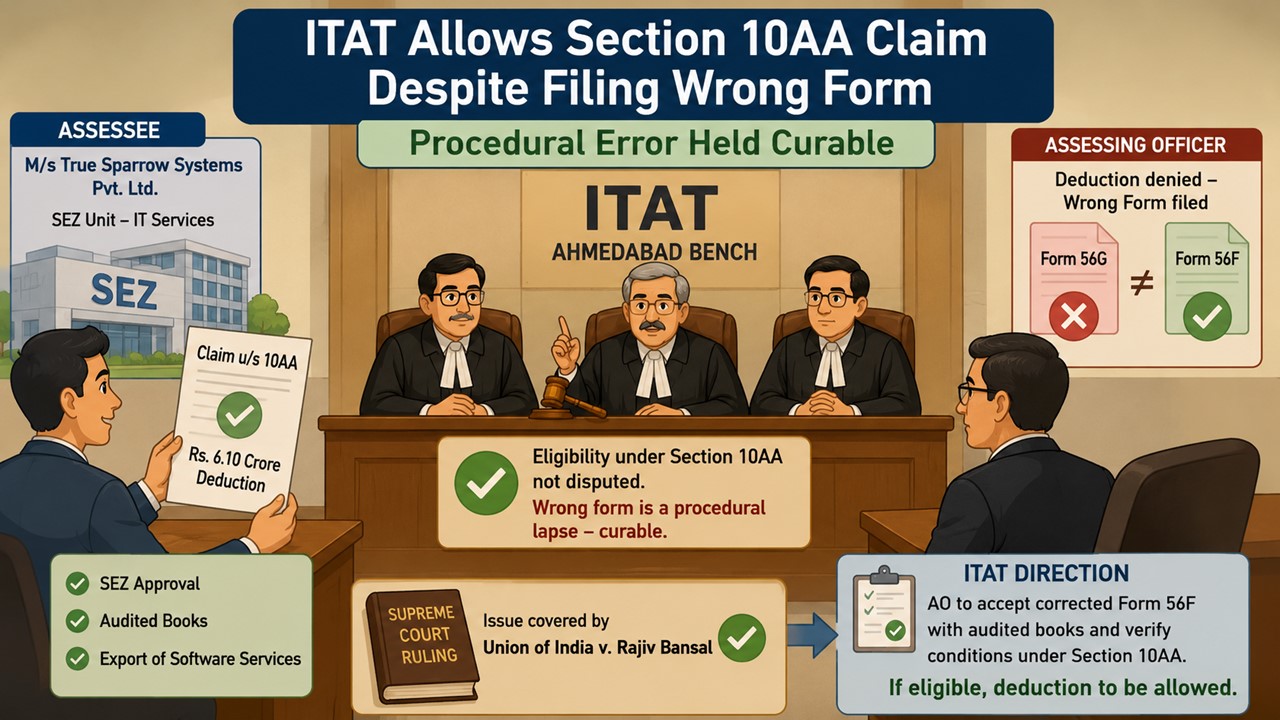

Filing Wrong Audit Form Treated as Procedural and Curable Defect

The Ahmedabad Bench of the ITAT held that filing the wrong prescribed form for claiming deduction under Section 10AA of the Income Tax Act is a procedural defect that can be rectified and cannot, by itself, justify denial of an otherwise eligible deduction.

The assessee, M/s True Sparrow Systems Private Limited, was engaged in providing information technology services and operated from a Special Economic Zone (SEZ). For AY 2014-15, it claimed deduction of Rs.6.10 crore under Section 10AA after obtaining approval from the SEZ authorities. The return was originally scrutinized under Section 143(3), and the deduction was accepted without any addition.

Subsequently, the assessment was reopened, and the Assessing Officer denied the deduction on the ground that the assessee had filed Form 56G instead of the prescribed Form 56F. According to the department, compliance with the prescribed form requirement was mandatory, and the deduction could not be allowed in its absence.

Before the Tribunal, the assessee contended that all substantive conditions for claiming deduction under Section 10AA were fulfilled. The unit had valid SEZ approval, its books were duly audited, and it earned income exclusively from export of software services. The filing of Form 56G instead of Form 56F was merely an inadvertent error by the Chartered Accountant and did not affect the assessee’s eligibility for the deduction.

For AY 2015-16, the Tribunal observed that the issue was covered by the decision of the Supreme Court in Union of India v. Rajiv Bansal and granted relief to the assessee.

The Tribunal noted that neither the Assessing Officer nor the CIT(A) had disputed the assessee’s substantive eligibility under Section 10AA. The only objection was the filing of an incorrect form. It held that such a procedural lapse is curable and should not result in denial of a legitimate tax benefit.

Thus, the ITAT directed the Assessing Officer to accept the corrected Form 56F along with the audited books of account and verify whether all conditions prescribed under Section 10AA are satisfied. If the assessee fulfills the statutory requirements, the deduction should be allowed.

To Read Full Order, Download PDF Given Below.

About Author

Meetu Kumari

Content Manager

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2229

2229My Recent Articles

- High Court Quashes Section 148 Notice Based on Wrong Assessee's Investigation ReportPremium

- ITAT Allows Set-Off of Brought Forward Business Loss Against Section 50 Capital GainsPremium

- High Court Quashes Reassessment Based on Mere Change of Opinion After ScrutinyPremium

- ITAT Refuses to Condoned 2,376-Day Delay, Dismisses Time-Barred Income Tax AppealPremium

- ITAT Restores Section 68 Addition Case After CIT(A) Rejects Fresh EvidencePremium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts