ITAT Grants 12AB Registration to Trust Despite Wrong Section Code in Form 10AB:

Tribunal grants registration, holding incorrect clause selection cannot defeat genuine charitable activities.

Genuine Charitable Activities Established Despite Incorrect Clause Selection in Form

Nagpur ITAT holds that a clerical error in selecting the wrong section code while filing Form 10AB cannot be a ground to deny registration when the trust’s charitable activities and documents are otherwise found genuine.

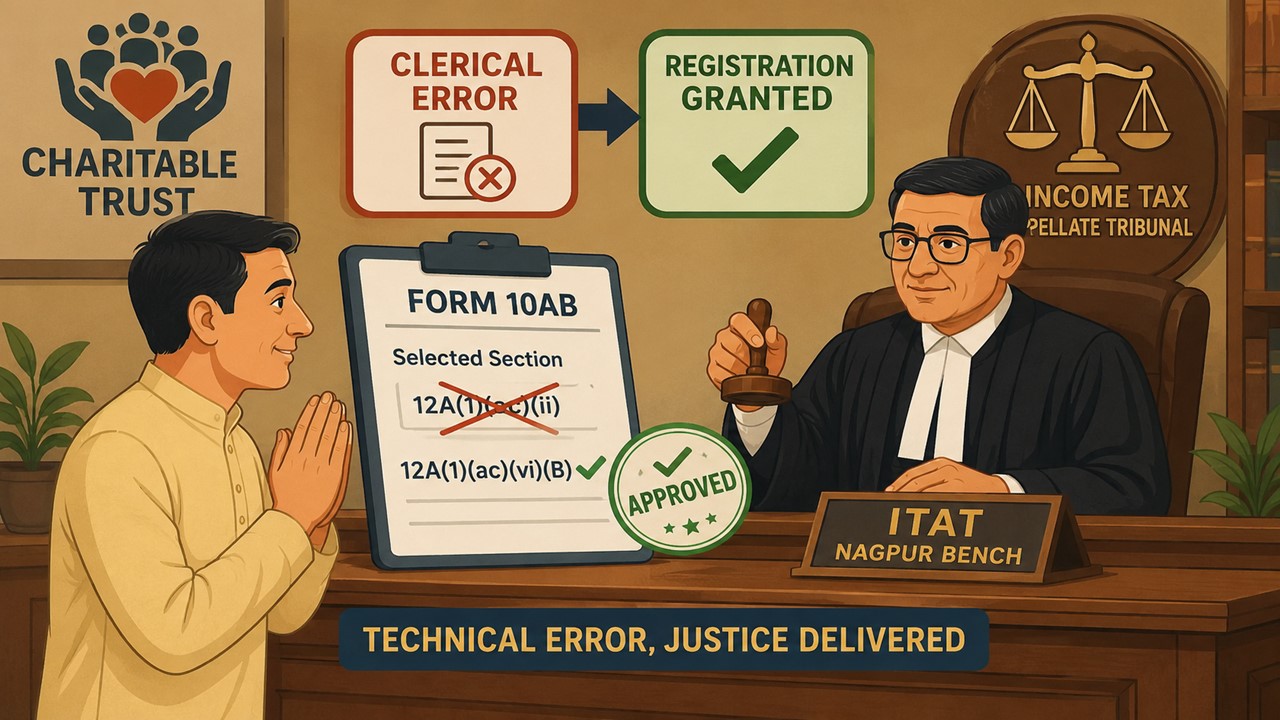

The Nagpur Bench of the Income Tax Appellate Tribunal (ITAT) allowed the appeal of Shree Shyam Mitra and directed the Commissioner of Income Tax (Exemption), Pune, to grant registration under Section 12AB of the Income-tax Act. The Tribunal observed that the trust’s application had been rejected solely because the wrong section code was selected in Form 10AB, despite the trust having furnished all relevant documents and established the genuineness of its charitable activities.

The assessee-trust, registered under the Bombay Public Trust Act, 1950 since 1983, had applied for registration under Section 12AB by filing Form 10AB on 6 March 2025. While filing the online application, the trust inadvertently selected Section 12A(1)(ac)(ii) instead of the appropriate clause, Section 12A(1)(ac)(vi)(B). Based on this technical error, the CIT(E) treated the application as non-maintainable and rejected it.

Before the Tribunal, the assessee submitted that the mistake was purely clerical and bona fide. It was pointed out that the trust had already commenced charitable activities and had furnished extensive supporting documents, including its registration certificate, trust deed and financial statements. The assessee further argued that the authorities had not identified any defect in its objects, activities or supporting evidence.

The Tribunal noted that the documents filed along with Form 10AB clearly demonstrated that the trust was carrying on charitable activities and that its application should have been considered under the correct statutory provision. It observed that during the proceedings, the trust had complied with all notices and furnished the details sought by the CIT(E). The only reason for rejection was the incorrect selection of the section code in the online form.

Relying on its earlier decision in Gospel India Ministries, the Tribunal reiterated that quoting a wrong provision or selecting an incorrect clause in an application cannot defeat a legitimate claim when the substantive conditions prescribed under the law are satisfied. It emphasized that registration under Section 12AB cannot be denied on mere technicalities when no discrepancy has been found in the trust’s charitable objects or activities.

Thus, the Tribunal set aside the order of the CIT(E) and directed the department to grant registration under Section 12AB to the assessee-trust.

The appeal was allowed and the ITAT directed the Revenue authorities to grant registration under Section 12AB, holding that a clerical error in selecting the section code in Form 10AB cannot justify rejection of a genuine charitable trust’s registration application.

To Read Full Order, Download PDF Given Below.

About Author

Meetu Kumari

Content Manager

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2231

2231My Recent Articles

- ITAT Restricts Bogus Purchase Addition to 1.15% Profit Element Despite Seller DenialsPremium

- ITAT Upholds Reassessment, Rejects Challenge Over Absence of Section 143(2) NoticePremium

- High Court Quashes Section 148 Notice Based on Wrong Assessee's Investigation ReportPremium

- ITAT Allows Set-Off of Brought Forward Business Loss Against Section 50 Capital GainsPremium

- High Court Quashes Reassessment Based on Mere Change of Opinion After ScrutinyPremium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts