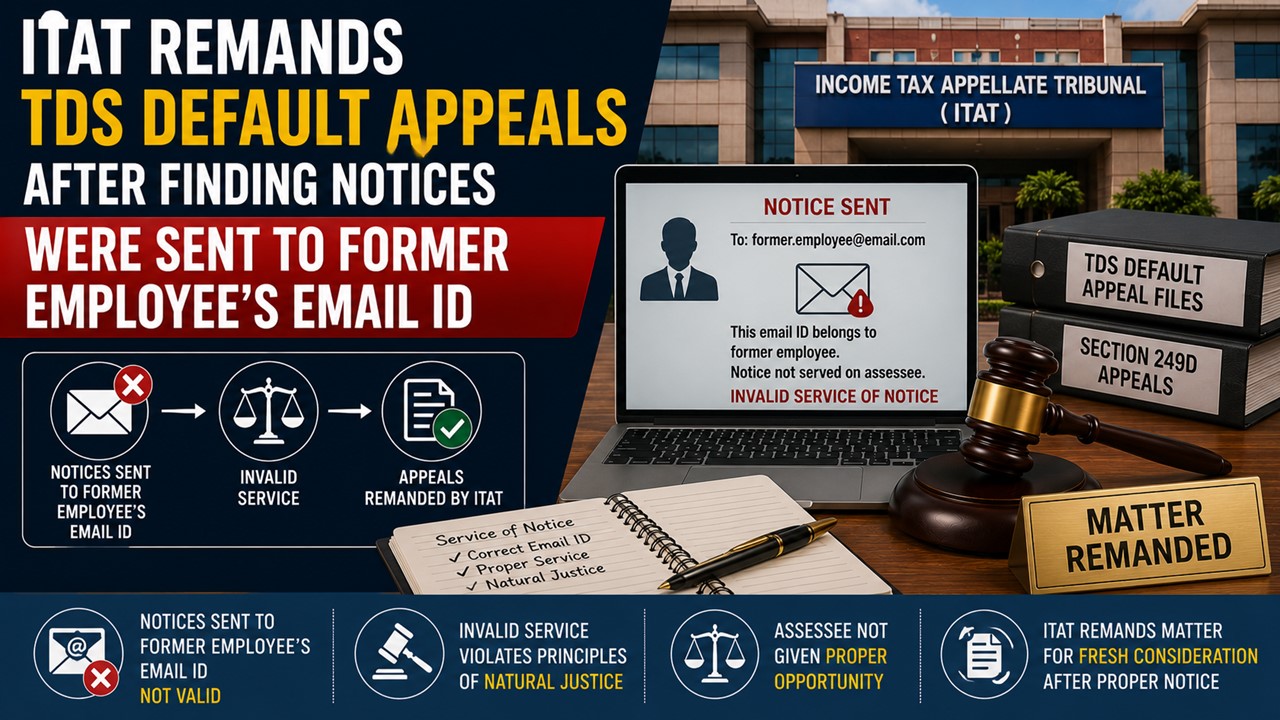

ITAT Remands TDS Default Appeals After Finding Notices Were Sent to Former Employee’s Email ID:

The Income Tax Appellate Tribunal (ITAT) Mumbai found that notices had been sent to an old email address belonging to a former employee and assessee was prevented by sufficient cause to comply with notice.

ITAT directs CIT(A) to adjudicate appeals afresh on merits

ITAT Remands TDS Default Appeals After Finding Notices Were Sent to Former Employee’s Email ID

The Income Tax Appellate Tribunal (ITAT) Mumbai held that the assessee was unable to comply with notices issued to it for default under Sections 201(1) and 201(1A) of the Income Tax Act because they were being communicated through an old email ID of a former employee.

The assessee is a partnership firm engaged in the business of construction and was subjected to proceedings under Sections 201(1) read with 201(1A) of the Income Tax Act, 1961, wherein the AO treated it as an “assessee in default” on account of alleged non-deduction and non-payment of tax at source. Aggrieved by the orders, the assessee preferred appeals before the CIT(A).

However, the CIT(A) dismissed the appeals on the grounds of delay in filing and non-compliance with notices issued during the appellate proceedings.

Before the Income Tax Appellate Tribunal, the assessee submitted that the notices issued by the appellate authority had been sent to an old email address belonging to a former employee who had already left the firm and contended that although a fresh email address had been furnished while filing the appeals, no notices were issued on that address, resulting in the assessee remaining unaware of the proceedings.

The Tribunal observed that the notices during the appellate proceedings had admittedly been issued to the earlier email address and not to the email address furnished by the assessee in its appeal documents, noting that the assessee had been prevented by sufficient cause from appearing before the CIT(A). The Bench deemed it appropriate to set aside the impugned orders and restore the matters to the file of the CIT(A). Accordingly, the appeals were allowed for statistical purposes, and the CIT(A) was directed to consider the reasons for delay wherever applicable and decide the appeals afresh on merits in accordance with law after providing a reasonable opportunity of hearing to the assessee.

About Author

Saima

Content Writer

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 224

224My Recent Articles

- ITAT Holds Fresh Application for Registration Under Sections 12AB and 80G Must Be Examined IndependentlyPremium

- ITAT Allows Full Tax Exemption on BSNL VRS Retrenchment CompensationPremium

- ITAT Deletes Disallowance of Marketing Expenses After Assessee Corroborates Ledger Entries with Debit NotesPremium

- ITAT Rules Executive Search Fee Not Taxable as FTS Under India-Netherlands DTAAPremium

- ITAT Holds Reimbursement of Common Expenses Without Profit Not Liable for TDSPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts