Know GSTR 1 closely

Know GSTR 1 closely [caption id="attachment_85984" align="aligncenter" width="96"] Riddhi Amin[/caption] GSTR-1 is a monthly or quarterly re

Know GSTR 1 closely

[caption id="attachment_85984" align="aligncenter" width="96"] Riddhi Amin[/caption]

GSTR-1 is a monthly or quarterly return that should be filed by every registered dealer. It contains details of all outward supplies i.e. sales. Let’s understand it in detail.

FURNISHING DETAILS OF OUTWARD SUPPLIES (Section 37):

(1) Persons liable to furnish the details of outward supply [Section 37(1)]:

The details of outward supplies of both goods and services are required to be furnished by every registered person including casual registered person except the following

i) an Input Service Distributor (ISD).

ii) a non-resident taxable person, (NRTP)

iii) a person paying tax under the provisions of Section 10 i.e. Composition Scheme,

iv) a person paying tax under the provisions of Section 51 i.e. person deducting tax at source,

v) a person paying tax under the provisions of Section 52 i.e. person collecting tax at source i.e. e-commerce operator (ECO), not being an agent,

vi) a supplier of online information and database access or retrieval services (OIDAR).

The above excluded persons have to file special returns.

(2) Form for submission of details of outward supplies [Section 37(1)]:

The details of outward supplies are required to be furnished, electronically, in Form GSTR-1. Such details can be furnished through the common portal, either directly or from a notified Facilitation Centre.

(3) Due date of submission of GSTR-1 - upto 10th of next month [Section 37(1)] :

GSTR-1 for a particular month is filed on or before the 10th day of the immediately succeeding month. In other words, GSTR-1 of a month can be filed any time between 1 and 10th day of the succeeding month.

i) Extension of time limit by Commissioner: The due date of filing GSTR-1 may be extended by the Commissioner/ Commissioner of State GST/Commissioner of UTGST for reasons to be recorded in writing, by notification, for a class of taxable persons.

ii) Details cannot be furnished from 11th to 15th of succeeding month : The registered person shall not be allowed to furnish the details of outward supplies i.e. GSTR-1 during the period from 11th day to 15th day of month succeeding the tax period.

Point to be noted: As a measure of easing the compliance requirement for small tax payers, GSTR-1 has been allowed to be filed quarterly by small tax payers with aggregate annual turnover up to 1.5 crore in the preceding financial year or the current financial year. Tax payers with annual aggregate turnover above 1.5 crore will however continue to file GSTR-1 on a monthly basis.

GSTR-1 cannot be furnished before the end of tax period:

A taxpayer cannot file GSTR-1 before the end of the current tax period i.e. to say for the month of November before 30th of November. However, following are the exceptions to this rule:

(1) Cancellation of GSTIN of a normal taxpayer

(2) Casual taxpayers, after the closure of their business.

A taxpayer who has applied for cancellation of registration will be allowed to file GSTR-1 after confirming receipt of the application.

(4) What kind of details of outward supplies are required to be furnished in GSTR-1

Contents of information in GSTR-1 [Explanation to Section 37 read with Rule 59(2) of CGST Rules]:

Basic & Other Details:

1. GSTIN

2. Legal Name & Trade Name

3. Aggregate Turnover in previous year

4. Tax Period

5. HSN-wise summary of Outward supplies

6. Details of documents issued

7. Advances received/advances adjusted

Details of Outward Supplies:

1. B2B

2. B2C

3. Zero rated & Deemed exports

4. Amendments for prior period

5. Nil Rated/Exempted/Non GST

6. Debit/Credit notes issued

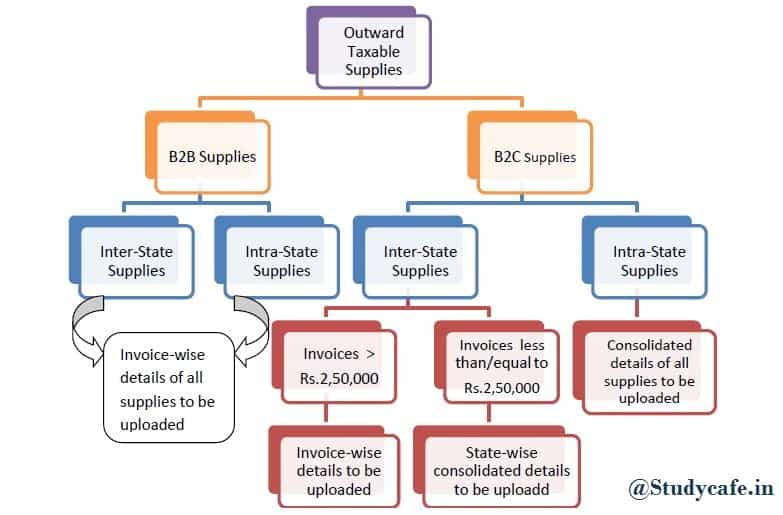

(5) Invoice wise & consolidated details:

The registered person is required to furnish details of Invoices & revised invoices issued in relation to supplies made by him to registered & unregistered persons during a month in GSTR-1 in the following manner:

Invoice-wise details of ALL

i) Inter-state & Intra-state supplies made to registered persons i.e. B2B supplies.

ii) Inter-state supplies made to unregistered persons with invoice value exceeding Rs.2,50,000 i.e. B2C supplies.

Consolidated details of ALL

i) Intra-state supplies made to unregistered persons for each rate of tax

ii) Inter-state supplies made to unregistered persons with invoice value upto Rs.2,50,000 for each rate of tax separately for each State

Thus, uploading of invoices depends on whether the supply is B2B or B2C plus whether the supply is intra-State or inter-State.

B2B means business to business transaction. In such type of transactions, the recipient is also a registered supplier and hence, takes ITC. B2C means business to consumer transaction. In such type of transactions, the recipient is consumer or unregistered and hence, will not take or cannot take ITC.

B2B supplies: For such supplies, all invoices will have to be uploaded irrespective of whether they are intra State or inter-State supplies. This is so because the recipient will take ITC and thus, invoice matching is required to be done.

B2C supplies: For B2C supplies, uploading in general may not be required as the buyer will not be taking ITC. However, still in order to implement the destination based principle, invoices of value more than 2.5 lakh in inter-State B2C supplies will have to be uploaded. For inter-State invoices below 2.5 lakh, State wise summary will be sufficient and for all intra-State invoices, only consolidated details will have to be given. Invoices can be uploaded at any time during the tax period and not just at the time of filing.

Note: See following chart for better & quick understanding of Invoice-wise details.

(6) Debit notes & Credit notes :

The registered person is required to furnish details of debit & credit notes ,if any ,issued during the month for invoices issued previously.

Riddhi Amin[/caption]

GSTR-1 is a monthly or quarterly return that should be filed by every registered dealer. It contains details of all outward supplies i.e. sales. Let’s understand it in detail.

FURNISHING DETAILS OF OUTWARD SUPPLIES (Section 37):

(1) Persons liable to furnish the details of outward supply [Section 37(1)]:

The details of outward supplies of both goods and services are required to be furnished by every registered person including casual registered person except the following

i) an Input Service Distributor (ISD).

ii) a non-resident taxable person, (NRTP)

iii) a person paying tax under the provisions of Section 10 i.e. Composition Scheme,

iv) a person paying tax under the provisions of Section 51 i.e. person deducting tax at source,

v) a person paying tax under the provisions of Section 52 i.e. person collecting tax at source i.e. e-commerce operator (ECO), not being an agent,

vi) a supplier of online information and database access or retrieval services (OIDAR).

The above excluded persons have to file special returns.

(2) Form for submission of details of outward supplies [Section 37(1)]:

The details of outward supplies are required to be furnished, electronically, in Form GSTR-1. Such details can be furnished through the common portal, either directly or from a notified Facilitation Centre.

(3) Due date of submission of GSTR-1 - upto 10th of next month [Section 37(1)] :

GSTR-1 for a particular month is filed on or before the 10th day of the immediately succeeding month. In other words, GSTR-1 of a month can be filed any time between 1 and 10th day of the succeeding month.

i) Extension of time limit by Commissioner: The due date of filing GSTR-1 may be extended by the Commissioner/ Commissioner of State GST/Commissioner of UTGST for reasons to be recorded in writing, by notification, for a class of taxable persons.

ii) Details cannot be furnished from 11th to 15th of succeeding month : The registered person shall not be allowed to furnish the details of outward supplies i.e. GSTR-1 during the period from 11th day to 15th day of month succeeding the tax period.

Point to be noted: As a measure of easing the compliance requirement for small tax payers, GSTR-1 has been allowed to be filed quarterly by small tax payers with aggregate annual turnover up to 1.5 crore in the preceding financial year or the current financial year. Tax payers with annual aggregate turnover above 1.5 crore will however continue to file GSTR-1 on a monthly basis.

GSTR-1 cannot be furnished before the end of tax period:

A taxpayer cannot file GSTR-1 before the end of the current tax period i.e. to say for the month of November before 30th of November. However, following are the exceptions to this rule:

(1) Cancellation of GSTIN of a normal taxpayer

(2) Casual taxpayers, after the closure of their business.

A taxpayer who has applied for cancellation of registration will be allowed to file GSTR-1 after confirming receipt of the application.

(4) What kind of details of outward supplies are required to be furnished in GSTR-1

Contents of information in GSTR-1 [Explanation to Section 37 read with Rule 59(2) of CGST Rules]:

Basic & Other Details:

1. GSTIN

2. Legal Name & Trade Name

3. Aggregate Turnover in previous year

4. Tax Period

5. HSN-wise summary of Outward supplies

6. Details of documents issued

7. Advances received/advances adjusted

Details of Outward Supplies:

1. B2B

2. B2C

3. Zero rated & Deemed exports

4. Amendments for prior period

5. Nil Rated/Exempted/Non GST

6. Debit/Credit notes issued

(5) Invoice wise & consolidated details:

The registered person is required to furnish details of Invoices & revised invoices issued in relation to supplies made by him to registered & unregistered persons during a month in GSTR-1 in the following manner:

Invoice-wise details of ALL

i) Inter-state & Intra-state supplies made to registered persons i.e. B2B supplies.

ii) Inter-state supplies made to unregistered persons with invoice value exceeding Rs.2,50,000 i.e. B2C supplies.

Consolidated details of ALL

i) Intra-state supplies made to unregistered persons for each rate of tax

ii) Inter-state supplies made to unregistered persons with invoice value upto Rs.2,50,000 for each rate of tax separately for each State

Thus, uploading of invoices depends on whether the supply is B2B or B2C plus whether the supply is intra-State or inter-State.

B2B means business to business transaction. In such type of transactions, the recipient is also a registered supplier and hence, takes ITC. B2C means business to consumer transaction. In such type of transactions, the recipient is consumer or unregistered and hence, will not take or cannot take ITC.

B2B supplies: For such supplies, all invoices will have to be uploaded irrespective of whether they are intra State or inter-State supplies. This is so because the recipient will take ITC and thus, invoice matching is required to be done.

B2C supplies: For B2C supplies, uploading in general may not be required as the buyer will not be taking ITC. However, still in order to implement the destination based principle, invoices of value more than 2.5 lakh in inter-State B2C supplies will have to be uploaded. For inter-State invoices below 2.5 lakh, State wise summary will be sufficient and for all intra-State invoices, only consolidated details will have to be given. Invoices can be uploaded at any time during the tax period and not just at the time of filing.

Note: See following chart for better & quick understanding of Invoice-wise details.

(6) Debit notes & Credit notes :

The registered person is required to furnish details of debit & credit notes ,if any ,issued during the month for invoices issued previously.

[ The above summary chart shows Invoice-wise details to be uploaded in case of B2B & B2C transaction]

Other Aspects :

I) Invoices can be modified/deleted any number of times till the submission of GSTR-1 of a Tax period .The uploaded invoice details are in a draft version till the GSTR-1 is submitted & can be changed irrespective of due date.

II) There is no need to upload scanned copies of invoices .Only certain prescribed fields of information from invoices need to be uploaded e.g. invoice number ,date ,value ,taxable value, rate of tax, amount of tax etc . In case there is no consideration, but the activity is a supply by virtue of Schedule 1 of CGST Act, the taxable value will have to be worked out as prescribed & uploaded.

III) Description of each item in the invoice will not be uploaded. Only HSN Code in respect of supply of goods & accounting code in respect of supply of services will have to be entered. The same depends upon the annual turnover of preceding financial year. As per Notification No. 12/2017-CT dated 28/06/2017, the number of digits of HSN Code to be quoted are as under :

[ The above summary chart shows Invoice-wise details to be uploaded in case of B2B & B2C transaction]

Other Aspects :

I) Invoices can be modified/deleted any number of times till the submission of GSTR-1 of a Tax period .The uploaded invoice details are in a draft version till the GSTR-1 is submitted & can be changed irrespective of due date.

II) There is no need to upload scanned copies of invoices .Only certain prescribed fields of information from invoices need to be uploaded e.g. invoice number ,date ,value ,taxable value, rate of tax, amount of tax etc . In case there is no consideration, but the activity is a supply by virtue of Schedule 1 of CGST Act, the taxable value will have to be worked out as prescribed & uploaded.

III) Description of each item in the invoice will not be uploaded. Only HSN Code in respect of supply of goods & accounting code in respect of supply of services will have to be entered. The same depends upon the annual turnover of preceding financial year. As per Notification No. 12/2017-CT dated 28/06/2017, the number of digits of HSN Code to be quoted are as under :

Other Aspects:

I) GSTR-1 needs to be filed even if there is no business activity (Nil Return) in the tax period.

II) Filing of GSTR-1 for current month is possible only when GSTR-1 for the previous month has been filed.

III) Taxpayer opting for voluntary cancellation of GSTIN will have to file GSTR-1 for active period.

IV) In cases where a taxpayer has been converted from a normal taxpayer to composition taxpayer, GSTR-1 will be available for filing only for the period during which the taxpayer was registered as normal taxpayer.

(7) How are the details of Outward supply furnished in prior periods amended

Amendment in the details of outward supply furnished for prior period [Section 37(3)]:

A) Scope of amendment/correction entries:

Amendment on communication of mismatch report: Tables 9, 10 and 11(II) of GSTR-1 provide for amendments in details of taxable outward supplies furnished in earlier periods. The supplier can make amendments in the particulars furnished in GSTR-1 filed by him for the prior periods if he agrees to the mismatch report communicated to him by the system every month after the processing of the return The details of original debit notes/ credit notes refund vouchers issued by the tax payer in the current tax period as also the revision in the debit notes/ credit notes/refund vouchers issued in the earlier tax periods are required to be shown in Table 9 of the GSTR-1.

Ordinarily in Amendment Table the supplier is required to give details of original invoice (No. and Date), the particulars of which have been wrongly entered in GSTR-1 of the earlier months and are now sought to be amended. However, it may happen that, a supplier altogether forgets to include the entire original invoice while furnishing the GSTR-1 for a particular month. In such cases also, he would be required to show the details of the said missing invoice which was issued in earlier month in the Amendment Table only, as such type of errors would also be regarded as data entry error.

(b) Rectification of unmatched entries and in case of short-payment of tax - Tax and interest to be paid [Section 37(3)]:

Any registered person who has furnished the details under this Section for any tax period and which have remained unmatched under section 42 or section 43, shall, upon discovery of any error or omission therein, rectify such error or omission in such manner as may be prescribed in the tax period in which it is noticed and shall pay the tax and interest, if any, in case there is a short payment of tax on account of such error or omission, in the return to be furnished for such tax period.

(8) What are the precautions that a taxpayer is required to take for a hassle free compliance under GST

1. Timely uploading of the details of outward supplies in Form GSTR-1: One of the most important things under GST is the timely uploading of the details of outward supplies in GSTR-1 by 10th of next month. How best this can be ensured will depend on the number of B2B invoices that the taxpayer issues. If the number is small, the taxpayer can upload all the information in one go. However, if the number of invoices is large, the invoices for debit/credit notes) should be uploaded on a regular basis.

2. Regular uploading of invoices: GST common portal allows regular uploading of invoices even on a real time basis. Till the statement is actually submitted, the system also allows the taxpayer to modify the uploaded invoices. Therefore, it would always be beneficial for the taxpayers to regularly upload the invoices. Last minute rush makes uploading difficult and comes with higher risk of possible failure and default.

3. Follow up with suppliers to upload the invoices of inward supplies: The second thing would be to ensure that taxpayers follow up on uploading the invoices of their inward supplies by their suppliers. This would be helpful in ensuring that the ITC is available without any hassle and delay. Recipients can also encourage their suppliers to upload their invoices on a regular basis instead of doing it on or case to the due date. The system would allow recipients to see if their suppliers have uploaded invoices pertaining to them.

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

For Regular Updates Join : https://t.me/Studycafe

Tags : GST, GST Return

This Article has been shared by By Riddhi Amin. She is a CA Final student and Founder of TaxKnowledge Facebook Page. She Can be contacted at [email protected] or +91 73592 69145

Riddhi Amin[/caption]

GSTR-1 is a monthly or quarterly return that should be filed by every registered dealer. It contains details of all outward supplies i.e. sales. Let’s understand it in detail.

FURNISHING DETAILS OF OUTWARD SUPPLIES (Section 37):

(1) Persons liable to furnish the details of outward supply [Section 37(1)]:

The details of outward supplies of both goods and services are required to be furnished by every registered person including casual registered person except the following

i) an Input Service Distributor (ISD).

ii) a non-resident taxable person, (NRTP)

iii) a person paying tax under the provisions of Section 10 i.e. Composition Scheme,

iv) a person paying tax under the provisions of Section 51 i.e. person deducting tax at source,

v) a person paying tax under the provisions of Section 52 i.e. person collecting tax at source i.e. e-commerce operator (ECO), not being an agent,

vi) a supplier of online information and database access or retrieval services (OIDAR).

The above excluded persons have to file special returns.

(2) Form for submission of details of outward supplies [Section 37(1)]:

The details of outward supplies are required to be furnished, electronically, in Form GSTR-1. Such details can be furnished through the common portal, either directly or from a notified Facilitation Centre.

(3) Due date of submission of GSTR-1 - upto 10th of next month [Section 37(1)] :

GSTR-1 for a particular month is filed on or before the 10th day of the immediately succeeding month. In other words, GSTR-1 of a month can be filed any time between 1 and 10th day of the succeeding month.

i) Extension of time limit by Commissioner: The due date of filing GSTR-1 may be extended by the Commissioner/ Commissioner of State GST/Commissioner of UTGST for reasons to be recorded in writing, by notification, for a class of taxable persons.

ii) Details cannot be furnished from 11th to 15th of succeeding month : The registered person shall not be allowed to furnish the details of outward supplies i.e. GSTR-1 during the period from 11th day to 15th day of month succeeding the tax period.

Point to be noted: As a measure of easing the compliance requirement for small tax payers, GSTR-1 has been allowed to be filed quarterly by small tax payers with aggregate annual turnover up to 1.5 crore in the preceding financial year or the current financial year. Tax payers with annual aggregate turnover above 1.5 crore will however continue to file GSTR-1 on a monthly basis.

GSTR-1 cannot be furnished before the end of tax period:

A taxpayer cannot file GSTR-1 before the end of the current tax period i.e. to say for the month of November before 30th of November. However, following are the exceptions to this rule:

(1) Cancellation of GSTIN of a normal taxpayer

(2) Casual taxpayers, after the closure of their business.

A taxpayer who has applied for cancellation of registration will be allowed to file GSTR-1 after confirming receipt of the application.

(4) What kind of details of outward supplies are required to be furnished in GSTR-1

Contents of information in GSTR-1 [Explanation to Section 37 read with Rule 59(2) of CGST Rules]:

Basic & Other Details:

1. GSTIN

2. Legal Name & Trade Name

3. Aggregate Turnover in previous year

4. Tax Period

5. HSN-wise summary of Outward supplies

6. Details of documents issued

7. Advances received/advances adjusted

Details of Outward Supplies:

1. B2B

2. B2C

3. Zero rated & Deemed exports

4. Amendments for prior period

5. Nil Rated/Exempted/Non GST

6. Debit/Credit notes issued

(5) Invoice wise & consolidated details:

The registered person is required to furnish details of Invoices & revised invoices issued in relation to supplies made by him to registered & unregistered persons during a month in GSTR-1 in the following manner:

Invoice-wise details of ALL

i) Inter-state & Intra-state supplies made to registered persons i.e. B2B supplies.

ii) Inter-state supplies made to unregistered persons with invoice value exceeding Rs.2,50,000 i.e. B2C supplies.

Consolidated details of ALL

i) Intra-state supplies made to unregistered persons for each rate of tax

ii) Inter-state supplies made to unregistered persons with invoice value upto Rs.2,50,000 for each rate of tax separately for each State

Thus, uploading of invoices depends on whether the supply is B2B or B2C plus whether the supply is intra-State or inter-State.

B2B means business to business transaction. In such type of transactions, the recipient is also a registered supplier and hence, takes ITC. B2C means business to consumer transaction. In such type of transactions, the recipient is consumer or unregistered and hence, will not take or cannot take ITC.

B2B supplies: For such supplies, all invoices will have to be uploaded irrespective of whether they are intra State or inter-State supplies. This is so because the recipient will take ITC and thus, invoice matching is required to be done.

B2C supplies: For B2C supplies, uploading in general may not be required as the buyer will not be taking ITC. However, still in order to implement the destination based principle, invoices of value more than 2.5 lakh in inter-State B2C supplies will have to be uploaded. For inter-State invoices below 2.5 lakh, State wise summary will be sufficient and for all intra-State invoices, only consolidated details will have to be given. Invoices can be uploaded at any time during the tax period and not just at the time of filing.

Note: See following chart for better & quick understanding of Invoice-wise details.

(6) Debit notes & Credit notes :

The registered person is required to furnish details of debit & credit notes ,if any ,issued during the month for invoices issued previously.

[ The above summary chart shows Invoice-wise details to be uploaded in case of B2B & B2C transaction]

Other Aspects :

I) Invoices can be modified/deleted any number of times till the submission of GSTR-1 of a Tax period .The uploaded invoice details are in a draft version till the GSTR-1 is submitted & can be changed irrespective of due date.

II) There is no need to upload scanned copies of invoices .Only certain prescribed fields of information from invoices need to be uploaded e.g. invoice number ,date ,value ,taxable value, rate of tax, amount of tax etc . In case there is no consideration, but the activity is a supply by virtue of Schedule 1 of CGST Act, the taxable value will have to be worked out as prescribed & uploaded.

III) Description of each item in the invoice will not be uploaded. Only HSN Code in respect of supply of goods & accounting code in respect of supply of services will have to be entered. The same depends upon the annual turnover of preceding financial year. As per Notification No. 12/2017-CT dated 28/06/2017, the number of digits of HSN Code to be quoted are as under :

| Annual turnover in the preceding financial year | Number of Digits of HSN Code |

| Upto Rs.1.5 crore | Nil |

| More than Rs.1.5 crore & upto Rs.5 crore | 2 |

| More than Rs.5 crore | 4 |

About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts