Deepak Gupta | May 22, 2019 |

how to file gstr 9 online, gstr 9 pdf, gstr 9 format, gstr 9 format in excel, gstr 9 format pdf, gstr 9 notification, gstr 9 due date, gstr 9 form pdf, GSTR-9, GST Annual Return, GSTR 9 , how to file annual return for GST, filing of GSTR 9, GSTR 9 : Annual Return Filing Format Eligibility & Rules, Filing Process of GST Annual Return GSTR 9, annual return under gst GSTR 9, How to File GST Annual Return GSTR 9, gst annual return format pdf and excel,gst annual return pdf, gst annual return format, gst annual return format in excel, gst annual return format pdf, gst annual return due date, annual return under gst pdf, gst annual return notification, gstr 9 annual return

Analysis of GST Annual Return Form GSTR 9

The taxpayers registered under GST have to file various returns including an annual return. As per the provisions of GST registered taxpayer is required to file an annual return (GSTR 9) once in a financial year on or before the 31st December following the end of such financial year. [For FY 17-18 the due date for Filing GSTR 9 has been extended to 30th June 2019] Annual Return is not for rectification of errors, but it is summarisation of all returns filed pertaining to the transaction from period 01/07/17 to 31/03/18 in a single return.

It is to be clarified that Annual GST Return (GSTR 9) is a consolidation of returns filed(GSTR 1 and GSTR 1)

Further an important point to note is that we cannot make payment of taxes while filing GSTR 9 or Annual Return. Declaring additional turnover/Taxes while filing GSTR 9 or Annual Return would simply mean informing proper officer on voluntary basis that you have not paid tax. In such cases one need to file FORM GST DRC-03 ( for making payment of taxes and interest ) and the proper officer shall issue an acknowledgement, accepting the payment made by the said person in FORM GST DRC04

| Amendment made by Notification No. 74/2018 Central Tax dated 31st December, 2018 1.) Headings in FORM GSTR-9 would be in respect of supplies etc. made during the year and not as declared in returns filed during the year. 2.) It is mandatory to file all your FORM GSTR-1 and FORM GSTR-3B for the FY 2017-18 before filing this return. The details for the period between July 2017 to March 2018 are to be provided in this return. 3.) It may be noted that additional liability for the FY 2017-18 not declared in FORM GSTR-1 and FORM GSTR-3B may be declared in this return. However, taxpayers cannot claim input tax credit unclaimed during FY 2017-18 through this return. 4.) HSN code may be declared only for those inward supplies whose value independently accounts for 10% or more of the total value of inward supplies 5.) Value of non-GST supply shall also include the value of no supply and may be reported in Table 5D, 5E and 5F of FORM GSTR-9 |

Broadly, an annual return in GSTR 9 is divided into 6 basic parts and the same are summarized here under

Through this article we have tried to analyse the broad elements of the Annual Return Form or GSTR 9.

GSTR 9 can be classified in 6 major parts, they are as follows :

| Parts | Description | Tables |

| Part 1 | Basic Details | Table 1-3 |

| Part 2 | Details of Outward and inward supplies made during the financial year | Table 4-5 |

| Part 3 | Details of ITC for the financial year | Table 6-8 |

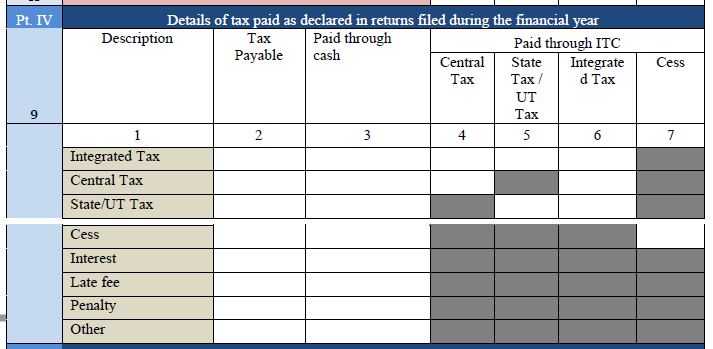

| Part 4 | Details of tax paid as declared in returns filed during the financial year | Table 9 |

| Part 5 | Particulars of the transactions for the previous FY declared in returns of April to September of current FY or upto date of filing of annual return of previous FY whichever is earlier | Table 10-14 |

| Part 6 | Other Information | Table 15-19 |

Part I comprises of Basic Details like Financial Year for which Annual Return is being filed, GSTIN Number , Legal Name and Trade Name of the Entity.

Points to be noted : Distinction between a trade name and a legal name must be clearly understood and borne out in clause 3A and 3B of Part I. Attention must be paid to the fact that the trade name and legal name are not used interchangeably.

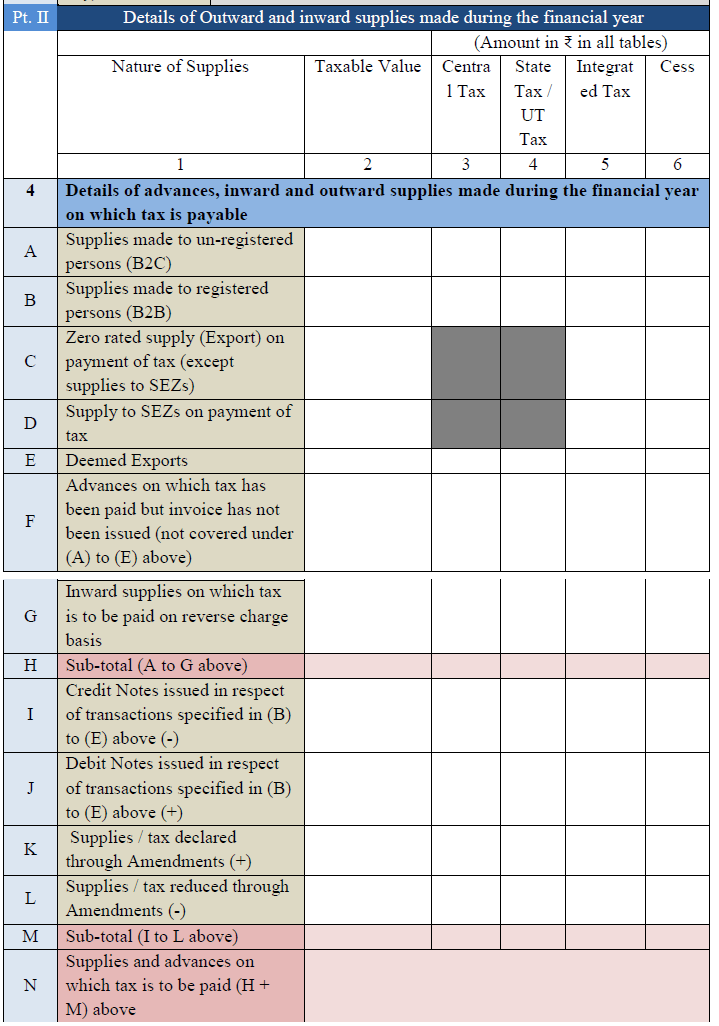

1 . Supplies made to un- registered persons (B2C)

1 . Supplies made to un- registered persons (B2C)

Aggregate value of supplies made to consumers and unregistered persons on which tax has been paid shall be declared here. These would include details of supplies made through E-Commerce operators and are to be declared as net of credit notes or debit notes issued in this regard. Table 5, Table 7 along with respective amendments in Table 9 and Table 10 of FORM GSTR-1 may be used for filling up these details.

2. Supplies made to registered persons (B2B)

Aggregate value of supplies made to registered persons (including supplies made to UINs) on which tax has been paid shall be declared here. These would include supplies made through E-Commerce operators but shall not include supplies on which tax is to be paid by the recipient on reverse charge basis. Details of debit and credit notes are to be mentioned separately. Table 4A and Table 4C of FORM GSTR-1 may be used for filling up these details.

3. Zero rated supply (Export) on payment of tax (except supplies to SEZs)

Aggregate value of exports (except supplies to SEZs) on which tax has been paid shall be declared here. Table 6A of FORM GSTR-1 may be used for filling up these details.

4. Supply to SEZs on payment of tax

Aggregate value of supplies to SEZs on which tax has been paid shall be declared here. Table 6B of GSTR-1 may be used for filling up these details.

5. Deemed Exports

Aggregate value of supplies in the nature of deemed exports on which tax has been paid shall be declared here. Table 6C of FORM GSTR-1 may be used for filling up these details.

6. Advances on which tax has been paid but invoice has not been issued (not covered under (A) to (E) above)

Details of all unadjusted advances i.e. advance has been received and tax has been paid but invoice has not been issued in the current year shall be declared here. Table 11A of FORM GSTR-1 may be used for filling up these details.

7. Inward supplies on which tax is to be paid on reverse charge basis

This would include invoices and debit notes on which tax is to be paid by the recipient (i.e.by the person filing the annual return) on reverse charge basis. This shall include supplies received from registered persons, unregistered persons on which tax is levied on reverse charge basis. This shall also include aggregate value of all import of services. Table 3.1(d) of FORM GSTR-3B may be used for filling up these details.

8. Credit Notes/Debit Notes issued in respect of transactions specified in (B) to (E) above

Aggregate value of credit notes issued in respect of B to B supplies (4B), exports (4C), supplies to SEZs (4D) and deemed exports (4E) shall be declared here. Table 9B of FORM GSTR-1 may be used for filling up these details.

9. Supplies / tax declared or reduced through Amendments

Details of amendments made to B to B supplies (4B), exports (4C), supplies to SEZs (4D) and deemed exports (4E), credit notes (4I), debit notes (4J) and Refund vouchers shall be declared here. Table 9A and Table 9C of FORM GSTR-1 may be used for filling up these details.

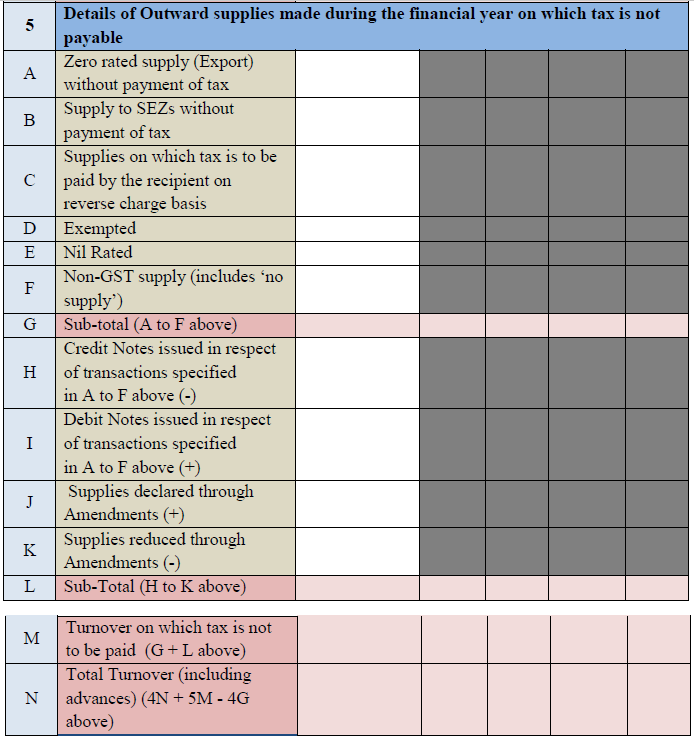

1 . Zero rated supply (Export) without payment of tax

1 . Zero rated supply (Export) without payment of tax

Aggregate value of exports (except supplies to SEZs) on which tax has not been Paid shall be declared here. Table 6A of FORM GSTR-1 may be used for filling up these details.

2. Supply to SEZs without payment of tax

Aggregate value of supplies to SEZs on which tax has not been paid shall be Declared here. Table 6B of GSTR-1 may be used for filling up these details

3. Supplies on which tax is to be paid by the recipient on reverse charge basis

Aggregate value of supplies made to registered persons on which tax is payable by the recipient on reverse charge basis. Details of debit and credit notes are to be mentioned separately. Table 4B of FORM GSTR-1 may be used for filling up these details.

4. Exempted/Nil Rated/Non-GST supply

Aggregate value of exempted, Nil Rated and Non-GST supplies shall be Declared here. Table 8 of FORM GSTR- 1 may be used for filling up these details. The value of no supply shall also be declared here.

The value of “no supply” shall be declared under Non-GST supply (5F).

5. Credit Notes/Debit Notes issued in respect of transactions specified in (A) to (F) above

Aggregate value of credit notes issued in respect of supplies declared in 5A,5B,5C, 5D, 5E and 5F shall be declared here. Table 9B of FORM GSTR-1 may be used for filling up these details.

6. Supplies declared or reduced through Amendments

Details of amendments made to exports (except supplies to SEZs) and supplies to SEZs on which tax has not been paid shall be declared here. Table 9A and Table 9C of FORM GSTR-1 may be used for filling up these details.

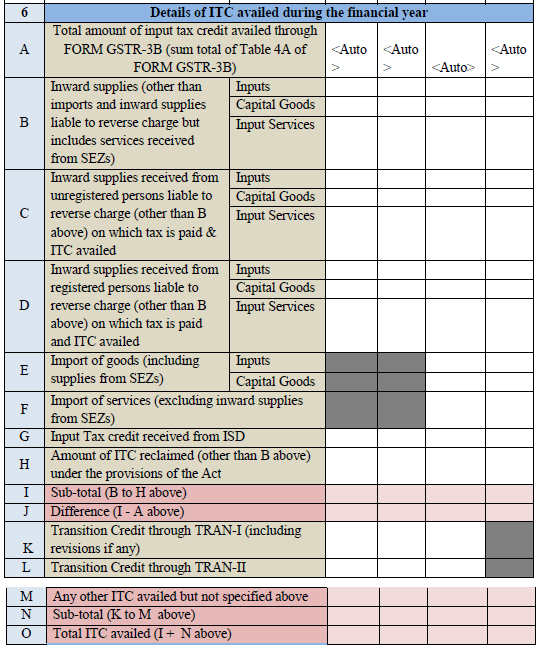

Total amount of input tax credit availed through FORM GSTR-3B (sum total of Table 4A of FORM GSTR-3B)

Total amount of input tax credit availed through FORM GSTR-3B (sum total of Table 4A of FORM GSTR-3B)

Total input tax credit availed in Table 4A of FORM GSTR-3B for the taxpayer Would be auto-populated here.

Inward supplies of Inputs, Capital Goods and Input Services (other than imports and inward supplies liable to reverse charge but includes services received from SEZs)

Aggregate value of input tax credit availed on all inward supplies except those on which tax is payable on reverse charge basis but includes supply of services Received from SEZs shall be declared here. It may be noted that the total ITC Availed is to be classified as ITC on inputs, capital goods and input services. Table 4(A)(5) of FORM GSTR-3B may be used for filling up these details. This shall not include ITC which was availed, reversed and then reclaimed in the ITC ledger. This is to be declared separately under 6(H) below.

Import of goods/Capital Goods (including supplies from SEZs)

Details of input tax credit availed on import of goods including supply of goods Received from SEZs shall be declared here. It may be noted that the total ITC Availed is to be classified as ITC on inputs and capital goods. Table 4(A)(1) of FORM GSTR- 3B may be used for filling up these details.

Import of services (excluding inward supplies from SEZs)

Details of input tax credit availed on import of services (excluding inward Supplies from SEZs) shall be declared here. Table 4(A)(2) of FORM GSTR- 3B may be used for filling up these details.

Input Tax credit received from ISD

Aggregate value of input tax credit received from input service distributor shall be declared here. Table 4(A)(4) of FORM GSTR-3B may be used for filling up These details.

Amount of ITC reclaimed (other than B above) under the provisions of the Act

Aggregate value of input tax credit availed, reversed and reclaimed under the provisions of the Act shall be declared here

Transition Credit through TRAN-I/TRAN-II

Details of transition credit received in the electronic credit ledger on filing of FORM GST TRAN-I including revision of TRAN-I (whether upwards or Downwards) or TRAN-II shall be declared here.

Any other ITC availed but not specified above

Details of ITC availed but not covered in any of heads specified under 6B to 6L Above shall be declared here. Details of ITC availed through FORM ITC01 and FORM ITC-02 in the financial year shall be declared here

Note : Ideally the difference between the total amount of input tax credit availed through FORM GSTR-3B and input tax credit declared in Annual Return should be zero.

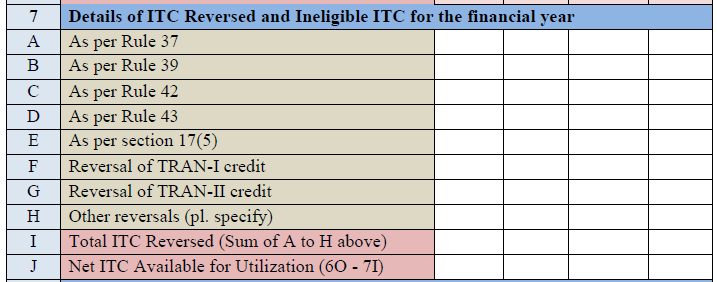

Details of input tax credit reversed due to ineligibility or reversals required Under rule 37, 39, 42 and 43 of the CGST Rules, 2017 shall be declared here. This column should also contain details of any input tax credit reversed under section 17(5) of the CGST Act, 2017 and details of ineligible transition credit claimed under FORM GST TRAN-I or FORM GST TRAN-II and then Subsequently reversed. Table 4(B) of FORM GSTR-3B may be used for filling up these details. Any ITC reversed through FORM ITC -03 shall be declared in 7H.

Details of input tax credit reversed due to ineligibility or reversals required Under rule 37, 39, 42 and 43 of the CGST Rules, 2017 shall be declared here. This column should also contain details of any input tax credit reversed under section 17(5) of the CGST Act, 2017 and details of ineligible transition credit claimed under FORM GST TRAN-I or FORM GST TRAN-II and then Subsequently reversed. Table 4(B) of FORM GSTR-3B may be used for filling up these details. Any ITC reversed through FORM ITC -03 shall be declared in 7H.

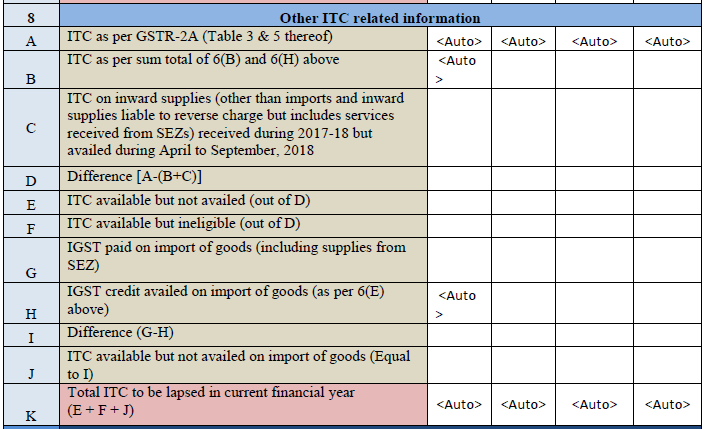

ITC as per GSTR-2A (Table 3 & 5 thereof)

The total credit available for inwards supplies (other than imports and inwards supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 and reflected in FORM GSTR-2A (table 3 & 5 only) Shall be auto-populated in this table. This would be the aggregate of all the input tax credit that has been declared by the corresponding suppliers in their FORM GSTR-I.

ITC as per sum total of 6(B) and 6(H) above shall be Auto-Populated

ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 but availed during April to September 2018

Aggregate value of input tax credit availed on all inward supplies (except those on which tax is payable on reverse charge basis but includes supply of services received from SEZs) received during July 2017 to March 2018 but credit on Which was availed between April to September 2018 shall be declared here. Table 4(A)(5) of FORM GSTR-3B may be used for filling up these details

IGST paid on import of goods (including supplies from SEZ)

Aggregate value of IGST paid at the time of imports (including imports from SEZs) during the financial year shall be declared here

Part 5: Particulars of the transactions for the previous FY declared in returns of April to September of current FY or upto date of filing of annual return of previous FY whichever is earlier

Part 5: Particulars of the transactions for the previous FY declared in returns of April to September of current FY or upto date of filing of annual return of previous FY whichever is earlier Supplies / tax declared through Amendments (+) (net of debit notes) or Supplies / tax reduced through Amendments (-) (net of credit notes)

Supplies / tax declared through Amendments (+) (net of debit notes) or Supplies / tax reduced through Amendments (-) (net of credit notes)

Details of additions or amendments to any of the supplies already declared in the returns of the previous financial year but such amendments were furnished in Table 9A, Table 9B and Table 9C of FORM GSTR-1 of April to September of the current financial year or date of filing of Annual Return for the previous financial year, whichever is earlier shall be declared here

Reversal of ITC availed during previous financial year

Aggregate value of reversal of ITC which was availed in the previous financial year but reversed in returns filed for the months of April to September of the current financial year or date of filing of Annual Return for previous financial Year, whichever is earlier shall be declared here. Table 4(B) of FORM GSTR- 3B may be used for filling up these details.

ITC availed for the previous financial year

Details of ITC for goods or services received in the previous financial year but ITC for the same was availed in returns filed for the months of April to September of the current financial year or date of filing of Annual Return for the previous financial year whichever is earlier shall be declared here. Table 4(A) of FORM GSTR-3B may be used for filling up these details

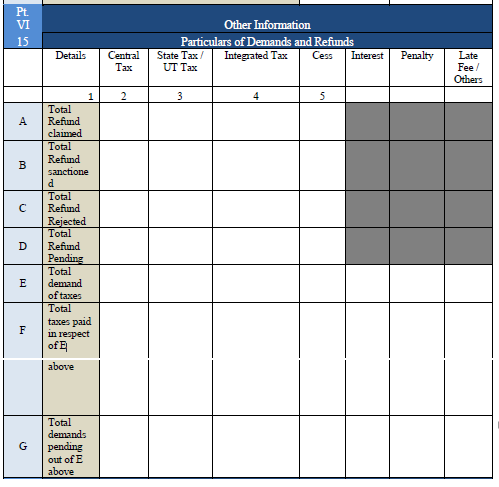

Aggregate value of refunds claimed, sanctioned, rejected and pending for Processing shall be declared here. Refund claimed would be the aggregate value of all the refund claims filed in the financial year and would include refunds which have been sanctioned, rejected or are pending for processing. Refund sanctioned means the aggregate value of all refund sanction orders. Refund pending would be the aggregate amount in all refund application for which acknowledgement has been received and would exclude provisional refunds received. These would not include details of non-GST refund claims.

Aggregate value of demands of taxes for which an order confirming the demand Has been issued by the adjudicating authority shall be declared here. Aggregate value of taxes paid out of the total value of confirmed demand as declared in 15E above shall be declared here. Aggregate value of demands pending recovery out of 15E above shall be declared here

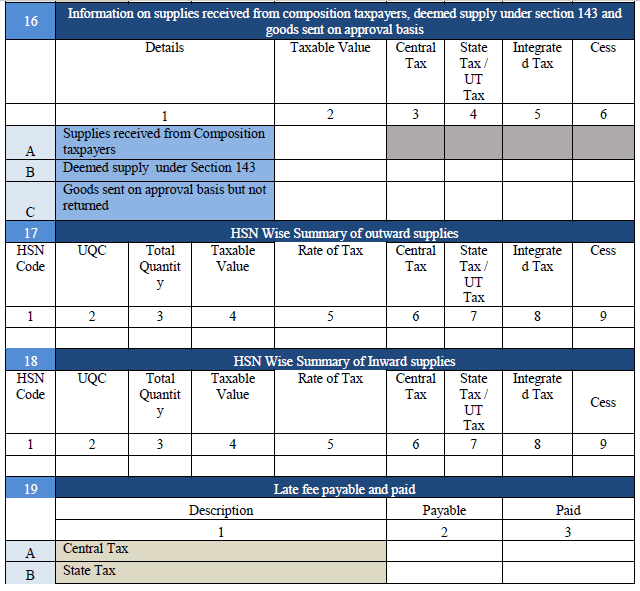

Supplies received from Composition taxpayers

Aggregate value of supplies received from composition taxpayers shall be Declared here. Table 5 of FORM GSTR-3B may be used for filling up these 7 Details.

Deemed supply under Section 143

Aggregate value of all deemed supplies from the principal to the job-worker in terms of sub-section (3) and sub-section (4) of Section 143 of the CGST Act shall be declared here.

Goods sent on approval basis but not returned

Aggregate value of all deemed supplies for goods which were sent on approval basis but were not returned to the principal supplier within one eighty days of such supply shall be declared here.

Summary of supplies effected and received against a particular HSN code is to be reported.

It would be optional for taxpayers having annual turnover up to Rs. 1.50 Cr.

It would be mandatory to report HSN code at two digits level for taxpayers having annual turnover in the preceding year above Rs. 1.50 Cr but up to Rs. 5.00 Cr and at four digits level for taxpayers having annual turnover above Rs. 5.00 Cr.

UQC details to be furnished only for supply of goods.

Note : HSN code may be declared only for those inward supplies whose value independently accounts for 10% or more of the total value of inward supplies

It is very important that Annual Return is filed carefully and with due diligence. As due date of filing annual return is coming close, it has become important for professionals to study it’s elements carefully so as to avoid future litigation.

Hope this article will help professionals in analyzing the elements of annual return.

The Author of the Article can be emailed at [email protected]

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information. In no event shall I shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information . Please refer your consultant before relying on the provisions of this article.

gst annual return format, how to file gstr 9 online, gstr 9 pdf, gstr 9 format, gstr 9 format in excel, gstr 9 format pdf, gstr 9 notification, gstr 9 due date, gstr 9 form pdf, GSTR-9, GST Annual Return, GSTR 9 , how to file annual return for GST, filing of GSTR 9, GSTR 9 : Annual Return Filing Format Eligibility & Rules, Filing Process of GST Annual Return GSTR 9, annual return under gst GSTR 9, How to File GST Annual Return GSTR 9, gst annual return format pdf and excel,gst annual return pdf, gst annual return format, gst annual return format in excel, gst annual return format pdf, gst annual return due date, annual return under gst pdf, gst annual return notification, gstr 9 annual return, gst annual return format in excel, gstr 9 format in excel, gstr 9 format pdf, gst annual return format pdf, gst annual return pdf, gstr 9 annual return format in excel, GSTR 9 : Annual Return Filing, Format, Eligibility & Rules, GSTR-9, GST Annual Return, GSTR 9 , how to file annual return for GST, filing of GSTR 9, gstr 9 pdf

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"