Basic Detailsfor GST Annual Returns :

GST Annual Return isto be filed once in a year by the registered taxpayers under GST including those registered under composition levy scheme. This form consists of details regarding the supplies made and received during the year under different tax heads i.e. CGST, SGST and IGST. It consolidates the information furnished in the monthly/quarterly returns during the year.

Through this article we have tried to complied basic questions on Basic Detailsfor GST Annual Returns.

Basic Detailsfor GST Annual Returns

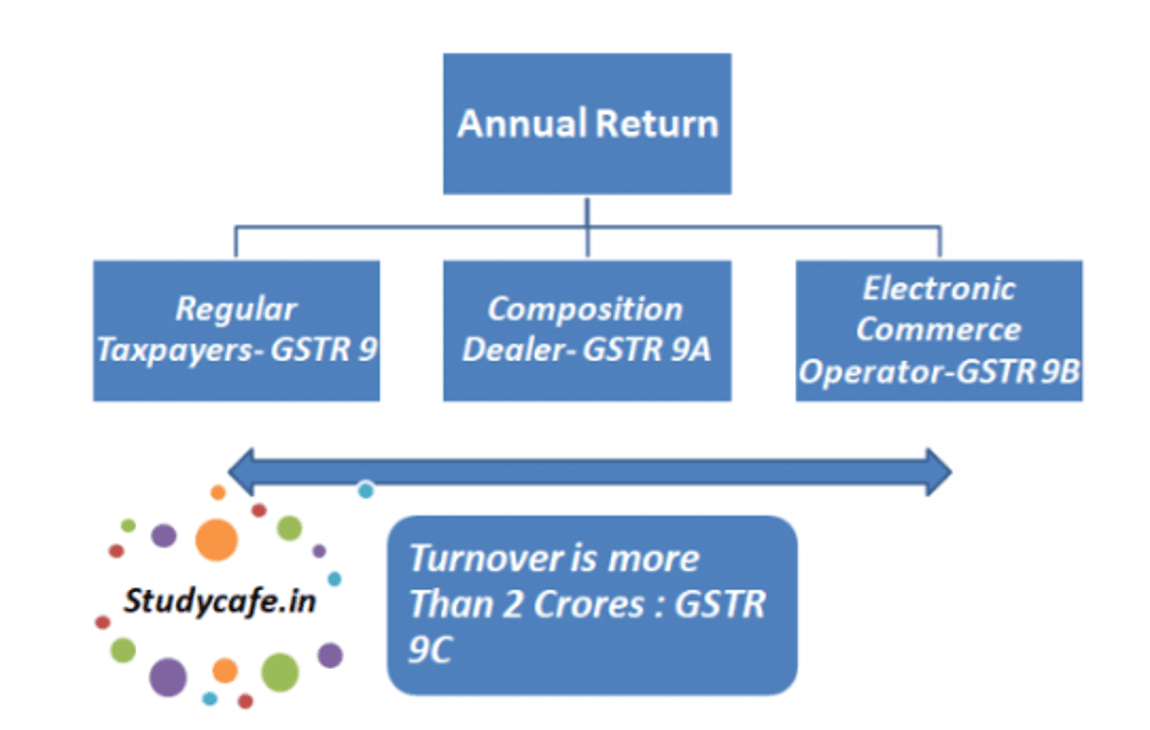

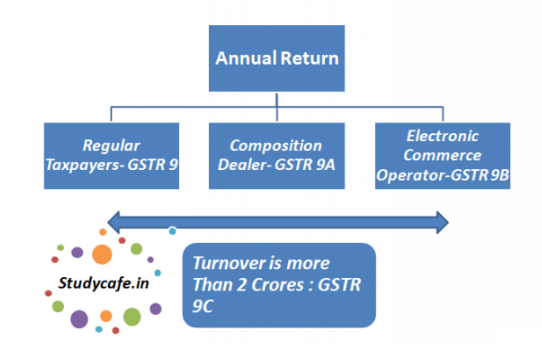

Question : How may types of Annual Return are there in GST

There are 4 types of return under GSTR 9 :

- GSTR 9: GSTR 9 should be filed by the regular taxpayers filing GSTR 1, GSTR 2, GSTR 3.

- GSTR 9A: GSTR 9A should be filed by the persons registered under composition scheme under GST.

- GSTR 9B: GSTR 9B should be filed by the e-commerce operators who have filed GSTR 8 during the financial year.

- GSTR 9C: GSTR 9C should be filed by the taxpayers whose annual turnover exceeds Rs 2 crores during the financial year.

4 types of return under GST

| For FY 17-18 no GST annual return for electronic commerce operator or GSTR 9B has been notified. Also the provisions of TDS and TCS were notified after March 2018, so it is quite clear that no GST 9B is required to be filed for FY 17-18 |

Question :Who all are required to file GSTR 9C and get there accounts audited

GSTR 9C should be filed by the taxpayers whose annual turnover exceeds Rs 2 crores during the financial year.All such taxpayers are also required to get their accounts audited and file a copy of audited annual accounts and reconciliation statement of tax already paid and tax payable as per audited accounts along with GSTR 9C.

Question : What is the due date of FilingGST Annual Return

The due date for filing GST Annual Returnfor FY 2017-18 is 30th June 2019.

Question : Who all are the persons who are not required to file GST Annual Return

Following persons are not required to file GSTR 9:

A. Casual Taxable Person

B. Input service distributors (ISD)

C.Non-resident taxable persons

D. Persons paying TDS under section 51.

Question : What is the penalty for late filing of GST Annual Return

1. Notice to defaulters: A notice shall be issued to defaulter requiring him to furnish such return within fifteen days in such form and manner as may be prescribed.

2. Late Fee : for delayed filing Late fee of Rs. 100/- per day for delay in furnishing GST Annual Return, subject to a maximum amount of quarter percent (0.25%) of the turnover in the State or Union Territory shall be imposed. Similar provisions for levy of late fee exist under the State / Union Territory GST Act, 2017. Therefore it can be concluded that a late fee of Rs.200/- per day (Rs. 100 under CGST law +Rs. 100/- under State / Union Territory GST law) could be levied which would be capped to a maximum amount of half percent (0.25% under the CGST Law + 0.25% under the SGST / UTGST Law) of turnover in the State or Union Territory.

3. General Penalty : for Contravention of Provisions A General Penalty may extend to twenty-five thousand rupees has been provided under CGST Act. An equal amount of penalty under the SGST/UTGST Act would also be applicable. To sum up a penalty of up to Rs.50,000/- (25000 under CGST Act + 25000 under SGST Act) could be levied. As of now the Due date of submitting Annual Return and GST Audit is 31st March 2018 [For FY 17-18]. Professionals should take due care of this date and do this compliance on time to avoid any penalty or litigation.

What is the process of filing GST Annual Return

GSTR 9 : Annual Return or Form GSTR-9 can be filed through both online and offline utility

Online Utility

- Online Based on GSTR-1 and GSTR-3B filed during the year, facility to download system computed GSTR-9 as PDF format will be available.

- Based on GSTR-1 filed, consolidated summary of GSTR-1 will be made available as PDF download.

- Based on GSTR-3B filed, consolidated summary of GSTR-3B will be made available as PDF download.

- In each table of GSTR-9, values will be auto-populated to the extent possible based on GSTR-3B and GSTR-1 of the year.

- All the values will be editable with some exceptions (table 6A, 8A and tax payment entries in table 9).

- Nil return can be filed through single click.

Offline Utility

- Offline tool to be downloaded from the portal.

- Auto-populated GSTR-9 (System computed json) to be downloaded from the portal before filling up values.

- Table 6A and table 8A will be non-editable.

- Other values will be editable barring tax payment entries in table 9.

- After filling up the values, json file to be generated and saved.

- After logging on the portal, the json file to be uploaded.

- File will be processed and error if any will be shown.

- Error file to be downloaded from the portal and opened in the Excel tool.

- After making corrections, file will again be uploaded on the portal.

- Correction can be made online also except table 17 & 18 if the number of records exceeds 500 in each table.

- After filing, return can be downloaded as PDF and/or Excel.

- Revision facility is not there, therefore, return should be filed after reconciling the information provided in the return and in the books.

GSTR-9A :Annual Return or Form GSTR-9A can be filed through both online and offline utility

Online Utility

- Online utility is Based on GSTR-4 filed during the year, facility to download system computed GSTR-9A as PDF format will be available.

- Based on GSTR-4 filed, consolidated summary of GSTR-4 will be made available as PDF download.

- In each table of GSTR-9A, values will be auto-populated to the extent possible based on GSTR-4 of the year. All the values will be editable with some exceptions.

- Nil return can be filed through single click.

Offline Utility

- Offline tool to be downloaded from the portal

- Auto-populated GSTR-9A (System computed json) to be downloaded from the portal before filling up values.

- Values will be editable with few exceptions.

- After filling up the values, json file to be generated and saved.

- After logging on the portal, the json file to be uploaded.

- File will be processed and error, if any will be shown.

- Error file to be downloaded from the portal and opened in the Excel tool.

- After making corrections, file will again be uploaded on the portal.

- After filing, return can be downloaded as pdf and/or Excel.

- Revision facility is not there, therefore, return should be filed after reconciling the information provided in the return and in the books.

GSTR-9C : Return to be prepared by Auditor (Chartered Accountant or Cost Accountant)

- Excel tool to be provided for preparation of the return.

- Auditor will generate json and handover to taxpayer after attaching DSC, who will upload the same on the portal.

- Other documents comprising Profit and Loss statement/ Income and expenditure statement etc. also to be uploaded.

- Turnover values will be based on GSTR-9 in few tables.

- A pdf of such values will be made available to taxpayer. Auditor may have the same from the taxpayer for use in preparing GSTR-9C.

- File will be processed on the portal and error, if any will be indicated. Taxpayer will download the file and handover to Auditor who will make correction. File to be uploaded again as it was uploaded originally.

- Processed file will be filed by taxpayer.

- Download option will be available at draft stage and after filing as well in pdf.

- Navigation option to make payment will be available which can be made through GST DRC-03.

Question : Can we make payment with annual return

No payment is to be made with annual return except late fee and Payment to be made on voluntary basis in DRC-03. While filing GSTR 9C taxpayer can make payment of taxes based on auditors recommendation but in that case also payment will be made by form DRC-03 andNavigation option to make payment will be available in GSTR 9C which will be linked with GSTR DRC-03

Download GST Annual Return Formats in Excel

Click here to Download Excel and word Formats of GST Annual Return.

After Reading this article viewers are requested to comment there queries on comment section given below. There queries will be incorporated in this article after due research.

(The Author of this Article can be reached at [email protected])

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information.In no event shall I shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information. Please refer your consultant before relying on the provisions of this article.

StudyCafe Membership

Join StudyCafe Membership. For More details about Membership Click Join Membership Button

Join MembershipIn case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"