Meetu Kumari | Jun 23, 2026 |

High Court Restores Time-Barred Service Tax Appeal After Holding Limitation Runs from Date of Knowledge

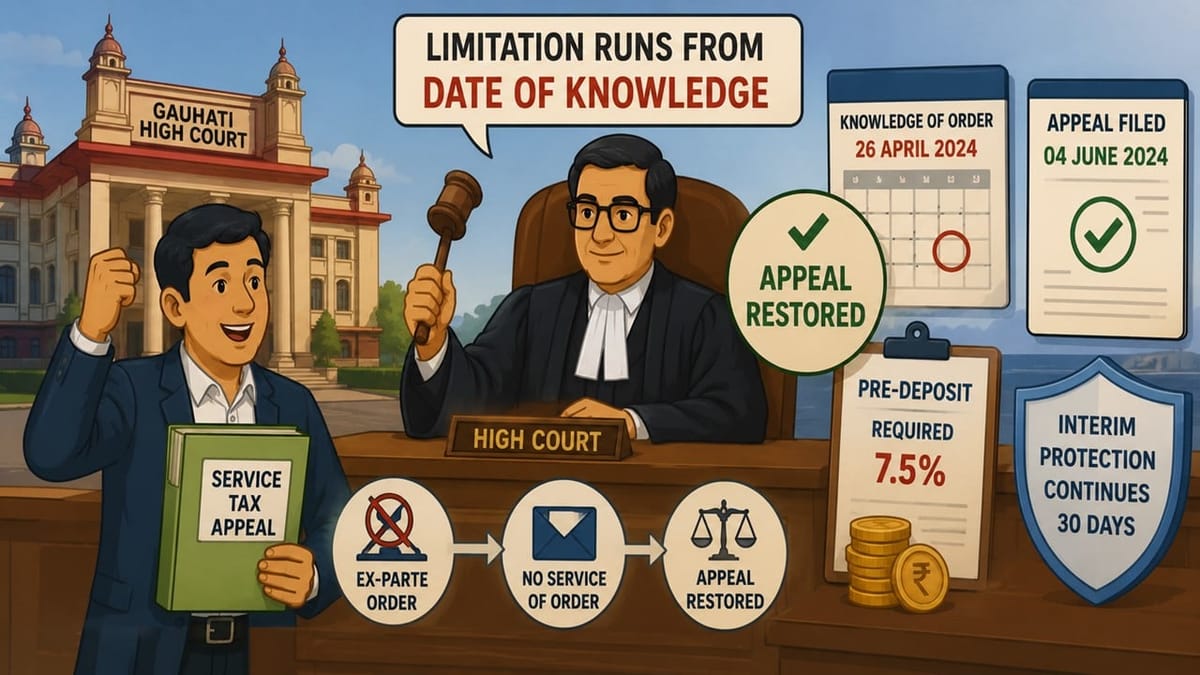

The Gauhati High Court restored a service tax appeal that had been dismissed as time-barred, holding that the limitation period should be computed from the date on which the assessee first became aware of the ex-parte adjudication order.

The petitioner, M/s Dona Food Beverages Private Limited, challenged an order of the Commissioner (Appeals) dismissing its appeal against a service tax demand. The appellate authority had rejected the appeal on two grounds: first, that it was filed beyond the statutory limitation period prescribed under Section 85 of the Finance Act, 1994, and second, that the mandatory pre-deposit of 7.5% of the disputed duty and penalty had not been made.

Before the High Court, the petitioner contended that neither the show cause notice nor the adjudication order dated 12.07.2022 had ever been served upon it. According to the petitioner, copies of the show cause notice and adjudication order were furnished only in April 2024 when its representatives visited the departmental office, following which the appeal was filed without delay. The petitioner also argued that a related issue had already been considered by the Joint Commissioner, CGST, Mumbai West, but this aspect was ignored while passing the ex-parte order.

The Revenue submitted that the dispute regarding service of the notice and order involved factual questions that could be examined by the appellate authority. However, it opposed any exemption from the statutory pre-deposit requirement, contending that Section 35F of the Central Excise Act, 1944, as made applicable to service tax matters, mandated payment of the prescribed amount before an appeal could be entertained.

Justice Devashis Baruah observed that the adjudication order had been passed ex-parte and that the petitioner claimed to have acquired knowledge of the proceedings only on 26.04.2024. In such circumstances, the Court held that the limitation period ought to be reckoned from the date of knowledge of the order rather than from the date on which the order was originally passed.

Exercising its writ jurisdiction under Article 226 of the Constitution, the High Court condoned the delay and directed that the appeal filed on 04.06.2024 be treated as having been filed within the prescribed period. At the same time, the Court declined to waive the mandatory pre-deposit requirement, holding that compliance with Section 35F was a statutory condition for consideration of the appeal on merits.

Thus, the High Court set aside the order of the Commissioner (Appeals), restored the appeal to its file, granted the petitioner 30 days to make the required pre-deposit, and directed that the interim protection already operating in the matter would continue for 30 days.

To Read Full Judgment, Download PDF Given Below

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"