Corporate Compliance Calendar-January 2020

ABOUT ARTICLE :

This article contains various Compliance requirements under Statutory Laws. Compliance means

“adhering to rules and regulations.”

Compliance Requirement Under

1. Income Tax Act, 1961

2. Goods & Services Tax Act, 2017 (GST)

3. Other Statutory Laws

4. Foreign Exchange Management Act, 1999 (FEMA)

5. SEBI (Listing Obligations And Disclosure Requirements) (LODR) Regulations, 2015

6. SEBI Takeover Regulations 2011

7. SEBI (Prohibition of Insider Trading) Regulations, 2015

8. SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018

9. SEBI (Buyback of Securities) Regulations, 2018

10. Companies Act, 2013 (MCA/ROC and LLP Compliance)

11. Investor Education and Protection Fund

12. ICSI Updates on e-CSIN

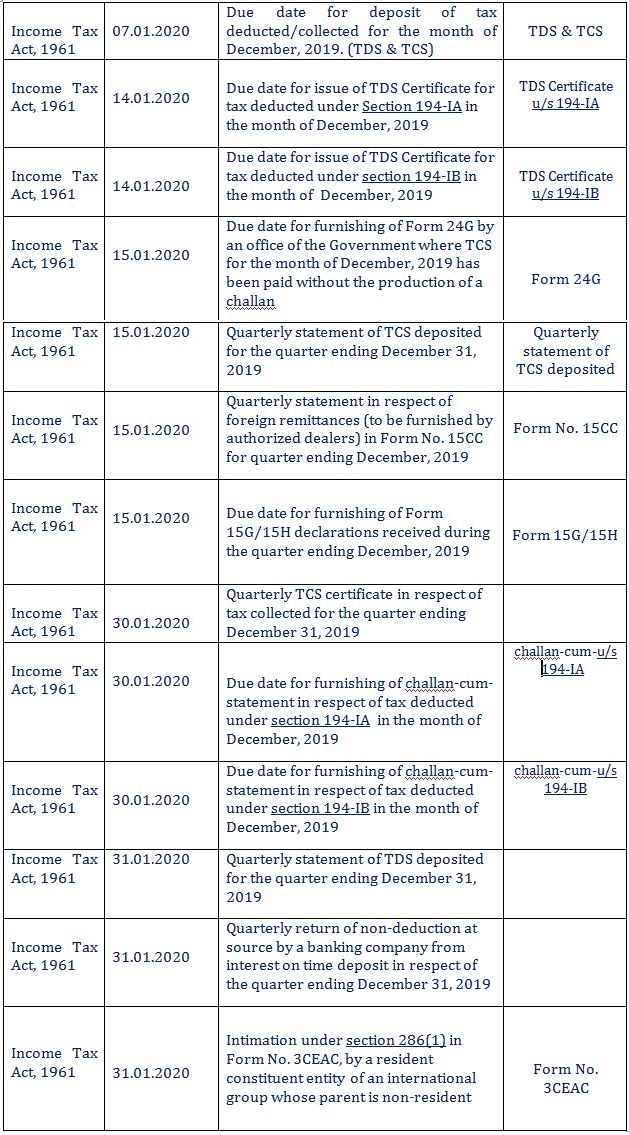

1. COMPLIANCE REQUIREMENT UNDER INCOME TAX ACT, 1961

• NOTE :

1. PAN-AADHAAR LINKING DEADLINE EXTENDED TO MARCH, 2020

• NOTE :

1. PAN-AADHAAR LINKING DEADLINE EXTENDED TO MARCH, 2020

The due date for linking of PAN with Aadhaar as specified under sub-section 2 of Section 139AA of the Income-tax Act,1961 has been extended from 31st December, 2019 to 31st March, 2020. (Notification no.107 of 2019 dated 30/12/2019 issued by CBDT.)

Source : https://www.incometaxindia.gov.in/communications/notification/notification_107_2019.pdf

2. PERSONS WHO HAVE MADE A DECLARATION UNDER SUB-SECTION (1) OF SECTION 183, BUT HAVE NOT MADE PAYMENT OF THE TAX AND SURCHARGE PAYABLE UNDER SECTION 184

In exercise of the powers conferred by the proviso to sub-section (1) of section 187 of the Finance Act, 2016 (28 of 2016), the Central Government hereby specifies that the persons who have made a declaration under sub-section (1) of section 183, but have not made payment of the tax and surcharge payable under section 184 and penalty payable under section 185 of the said Act, in respect of the undisclosed income, on or before the due date notified by the Central Government vide notification number S.O. 1830 (E), dated the 19th May, 2016, (as subsequently amended vide notification number S.O. 2476 (E), dated the 20th July, 2016), may make the payment of such amount on or before the 31st day of January, 2020, along with interest on such amount, at the rate of one per cent. for every month or part of a month comprised in the period commencing on the date immediately following the said due date as so notified and ending on the date of such payment.

Source : https://www.incometaxindia.gov.in/communications/notification/notification_103_2019.pdf

3. INCOME TAX (15TH AMENDMENT) RULES, 2019

Source : https://www.incometaxindia.gov.in/communications/notification/notification_104_2019.pdf

4. CLARIFICATIONS IN RESPECT OF PRESCRIBED ELECTRONIC MODES UNDER SECTION 269SU OF THE INCOME-TAX ACT, 1961

SOURCE : https://www.incometaxindia.gov.in/communications/circular/circular_32_2019.pdf

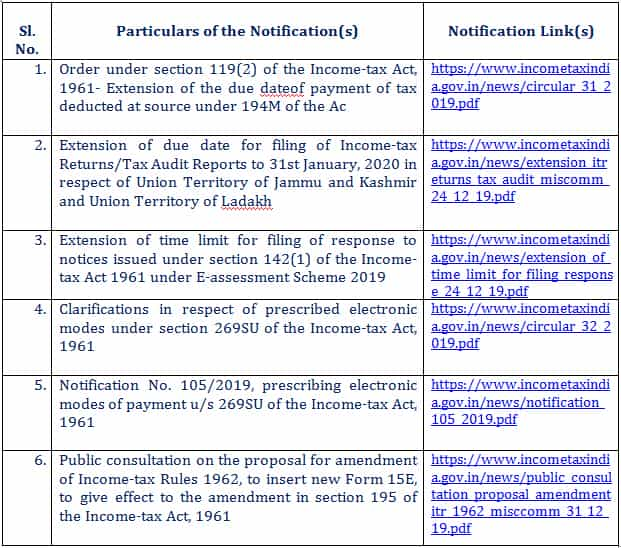

• IMPORTANT NOTIFICATIONS :

*Order under section 119(2) of the Income-tax Act, 1961- Extension of the due date of payment of tax deducted at source under 194M of the Act

*Order under section 119(2) of the Income-tax Act, 1961- Extension of the due date of payment of tax deducted at source under 194M of the Act

https://www.incometaxindia.gov.in/communications/circular/circular_31_2019.pdf

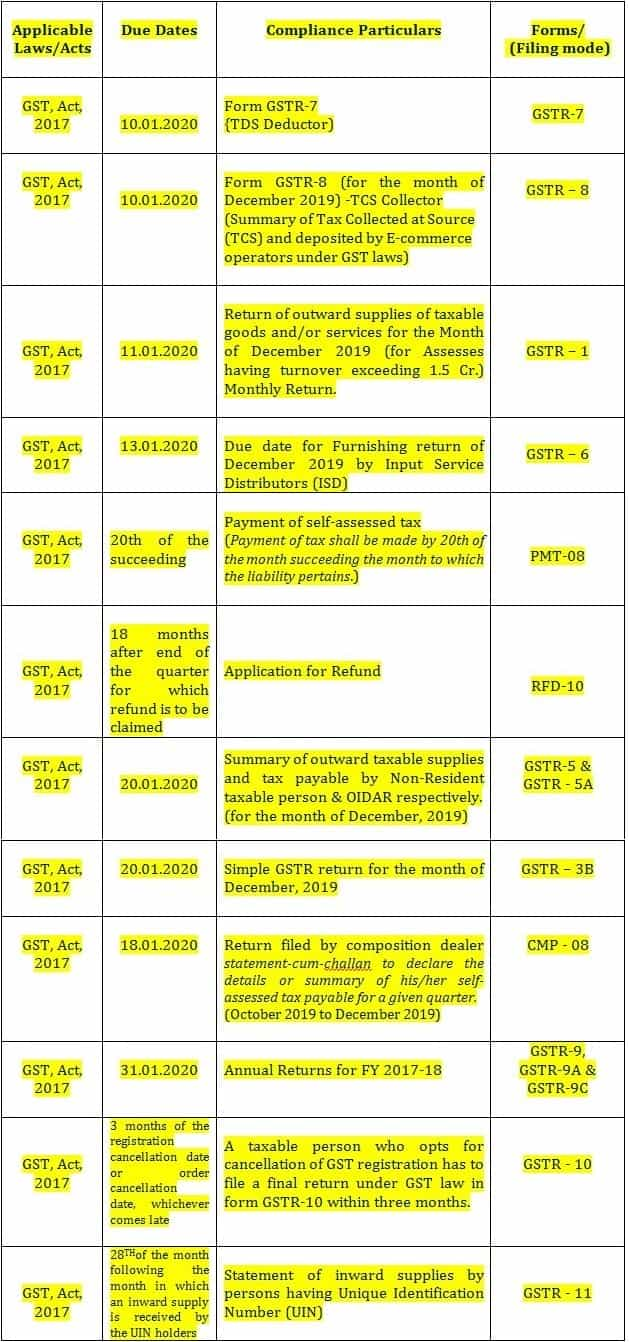

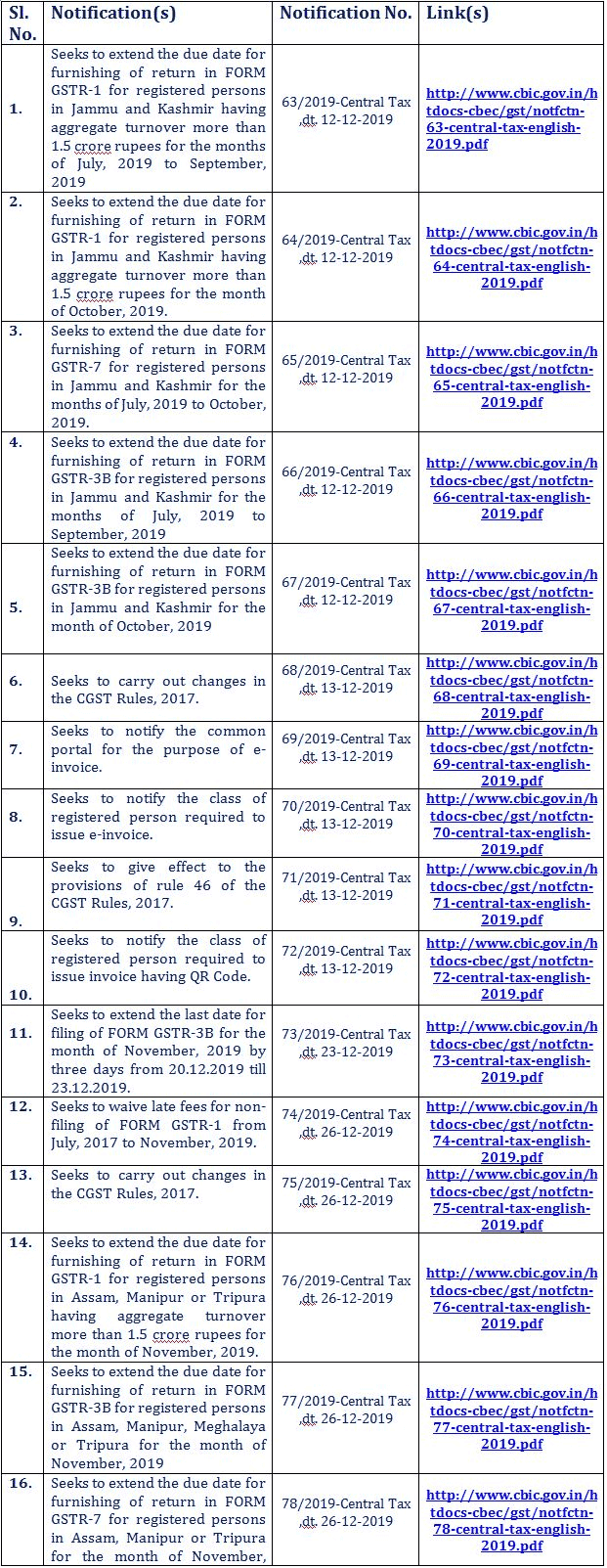

2. COMPLIANCE REQUIREMENT UNDER GOODS & SERVICES TAX ACT, (GST) 2017

• KEY UPDATE(s) :

1. Annual Return 2017-18

• KEY UPDATE(s) :

1. Annual Return 2017-18

Updated version of the Offline tool of GSTR-9C (Version 1.5) was made available on the portal on 24-12-2019. A minor issue has come to notice in auditor`s certificate issued in Part-B(ii) . The issue will be fixed shortly. In the meantime, where Part-B(ii) of the certificate is not applicable i.e. auditor preparing GSTR-9C has also conducted audit of the business and same number is applicable, they may continue with statement preparation and filing.

(https://www.gst.gov.in/newsandupdates/read/343)

2. Forms available on GST Portal for Taxpayers and Tax Officials

Government has issued various forms for GST related compliances to be made by taxpayers and for taking actions on them by tax officials. Various forms issued for registration, filing returns or refunds etc. have been made available on the GST Portal.. (https://www.gst.gov.in/newsandupdates/read/340)

3. List of CGST nodal officers for IT Grievance Redressal

http://cbic.gov.in/htdocs-cbec/gst/IT-Grievance-Nodal-Officers.xlsx

4. Blocking and Unblocking of EWB generation facility at E-way Bill Portal

https://www.gst.gov.in/newsandupdates/read/336

5. EXPLANATORY NOTES TO THE SCHEME OF CLASSIFICATION OF SERVICES

http://www.cbic.gov.in/resources//htdocs-cbec/gst/explanatory_notes_01oct19.pdf

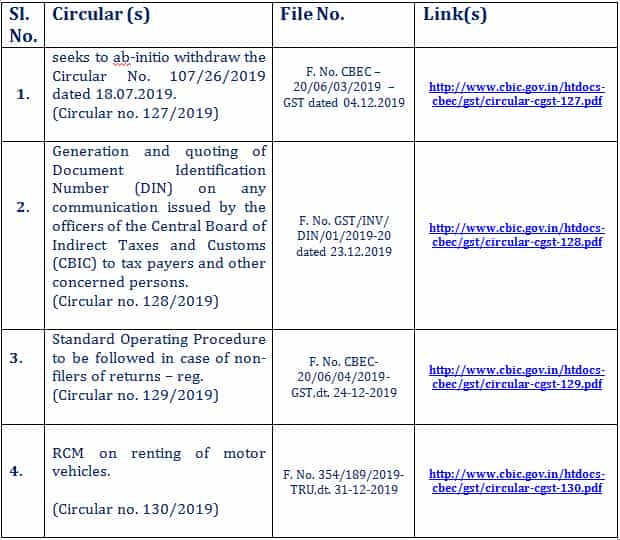

• GST UPDATES AS ON 29.11.2019 :

• Important Circulars :

• Important Circulars :

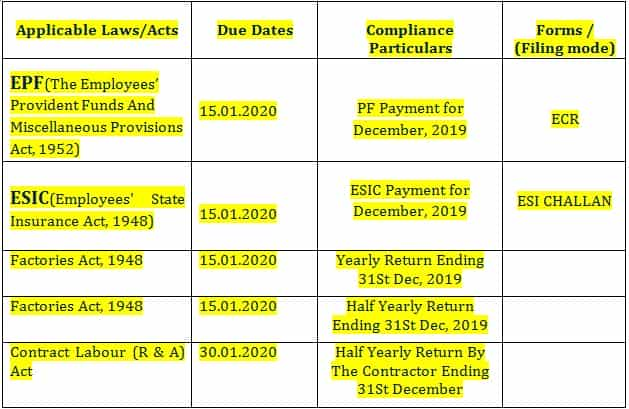

3. COMPLIANCE UNDER OTHER STATUTORY LAWS

3. COMPLIANCE UNDER OTHER STATUTORY LAWS

• QUICK REVIEW ON COMPLIANCE PARTICULARS :

• QUICK REVIEW ON COMPLIANCE PARTICULARS :

| Sl. No. |

Name of the Act(s) |

Compliance Particulars |

| 1 |

Factories Act 1948 |

• Annual returns and half year returns submitted on time with correct details

• All story statutory registers are maintained

• Appointment of Safety Officer, Welfare Officer, if applicable, and its qualification matching as per the act

• Canteen, Creche, rest room facilities are available |

| 2 |

Contact Labor Act 1970 |

• First check if this act is applicable to factory and to contractor. General rule say it is applicable for more than 20 contract workers. But it differs differs from state to state

• Principal Employer Registration, all contractor are listed on RC

• Contractor have valid License

• Contractor have submitted all dues like PF, ESIC, PT, LWF on time. |

| 3 |

Payment of Gratuity Act 1972: |

• Gratuity are paid to left employees who have completed 5 years

• Company have authorised one managerial personnel in organisation to receive all notice, letter, communication, etc |

| 4 |

Payment of Bonus Act 1965 |

• Bonus are paid on time. Returns submitted, register are maintained |

| 5 |

Payment of Wages 1936

and Minimum Wages Act 1948: |

• All registers are maintained

• Payment of Wages are done on time.

• Wages are paid above minimum wages. |

4. COMPLIANCES UNDER FEMA / RBI

| Applicable Laws/Acts |

Due Dates |

Compliance Particulars |

Forms / (Filing mode) |

| FEMA ACT 1999 |

Monthly Basis |

External Commercial Borrowings

Borrowers are required to report all ECB transactions to the RBI on a monthly basis through an AD Category – I Bank in the form of ‘ECB 2 Return’. |

ECB 2 Return |

| FEMA ACT 1999 |

Not later than 30 days from the date of issue of shares |

After issue of shares or other eligible securities, the Indian company has to file |

Form FC-GPR |

| FEMA ACT 1999 |

With in 60 days from the date of receipt of the amount of consideration. |

Reporting of transfer of shares and other eligible securities between residents and non-residents and vice- versa is to be made in Form FC-TRS. |

Form FC-TRS. |

| FEMA ACT 1999 |

With in Six (6) months {receive share certificates or any other documentary evidence of investment in the foreign JV / WOS as an evidence of investment and submit the same to the designated AD within 6 months;} |

An Indian Party and a Resident Individual making an overseas investment is required to submit form ODI

(Overseas investments (or financial commitment) in Joint Ventures (JV) and Wholly Owned Subsidiaries (WOS)) |

Form ODI |

5. COMPLIANCE REQUIREMENT UNDER SEBI (LISTING OBLIGATIONS AND DISCLOSURE REQUIREMENTS) (LODR) REGULATIONS, 2015

| FILING MODE(s) :

• For BSE : BSE LISTING CENTRE

• For NSE : NEAPS Portal |

•

Quarterly Compliances

| Sl. No. |

Regulation No. |

Compliance Particular |

Compliance Period

(Due Date) |

| 1 |

Regulation 13 (3) |

Statement of Investor complaints |

Within 21 days from the quarter end. |

| 2 |

Regulation 27 (2) |

Corporate Governance Report |

Within 15 days from quarter end. |

| 3 |

Regulation 31 |

Shareholding Pattern |

Within 21 days from quarter end. |

| 4 |

Regulation 32(1) |

Statement of deviation(s) or variation(s).

( *for public issue, rights issue, preferential issue etc.) |

Quarterly Basis |

| 5 |

Regulation 69 |

Indian Depository Receipt holding pattern & Shareholding details |

within 15 days of end of the quarter. |

•

Half Yearly Compliances

| Sl. No. |

Regulation No. |

Compliance Particular |

Compliance Period

(Due Date) |

| 1 |

Regulation 7(3) |

Compliance Certificate certifying maintaining physical and electronic transfer facility |

Within one month of end of each half of the financial year |

| 2 |

Regulation 40(9) |

Certificate from Practicing Company Secretary (PCS) |

Within one month of end of each half of the financial year |

| 3 |

Regulation 40(10) |

Transfer or transmission or transposition of securities |

Within one month of end of each half of the financial year |

| 4 |

Regulation 33 )

(SME) |

Un audited Financial Results within 45 days & Audited finance within 60 days |

April to Sep :14th day of November

Oct to March: & Full year Audited:

30th May |

•

Annual Compliances

| Sl. No. |

Regulation No. |

Compliance Particular |

Compliance Period

(Due Date) |

| 1 |

Regulation 14 |

Listing fees & other Charges |

Payment manner as specified by the Board of by Recognised Stock Exchange. |

| 2 |

Regulation 34*

(shall be amended w.e.f. April 2019) |

Annual Report |

Within 21 working days from the AGM Date |

| 3 |

Regulation 34(1)(a) |

a copy of the annual report sent to the shareholders along with the notice of the annual general meeting not later than the day of commencement of dispatch to its shareholders; |

Within one days from Dispatch to shareholder |

| 4 |

Annual report in XBRL mode

16 may 2019

BSE CIRCULAR'

Link |

Filings in respect of Annual Report has to be done by all listed entities in XBRL mode in addition to the currently used PDF mode mandatorily, for periods ending March 31, 2019. |

Same time limit of Regulation 34 |

| 5 |

Regulation 34(1)(b) |

in the event of any changes to the annual report, the revised copy along with the details of and explanation for the changes shall be sent not later than 48 hours after the annual general meeting. |

Within 48 hours after AGM |

| 6 |

Regulation 36 |

The listed entity shall send annual report referred to in to the holders of securities, not less than twenty-one days before the annual general meeting. |

21 days Before AGM (in soft or hard copy) |

•

Event based Compliances

| Sl. No. |

Regulation No. |

Compliance Particular |

Compliance Period

(Due Date) |

| 1 |

Regulation 7 (5) |

Intimation of

appointment / Change of Share Transfer Agent. |

Within 7 days of Agreement with

RTA. |

| 2 |

Regulation 17(2) |

Meeting of Board of Directors |

The board of directors shall meet at least 4 times a year, with a maximum time gap of 120 days between any two meetings. |

| 3 |

Regulation 18(2) |

Meeting of the audit committee |

The audit committee shall meet at least 4 times in a year and not more than 120 days shall elapse between two meetings. |

| 4 |

Regulation 29 |

Notice for Board Meeting to consider the prescribed matters. |

The Company shall give an advance notice of:

a) at least 5 days for Financial Result as per Regulation 29 1 (a)

b) in case matters as stated in regulation 29 1 (b) to (f) –

2 Working days in advance(Excluding the date of the intimation and date of the meeting) to Stock Exchange.

c) 11 working days in case matter related to alteration in i) Securities ;ii) date of interest or redemption of Debenture / bond as per regulation 29(3) (a) ,(b). |

| 5 |

Regulation 30 |

Outcome of Board Meeting (Schedule III Part A- (4) |

within 30 minutes of the closure of the meeting |

| 6 |

Regulation 31 |

Holding of specified securities and shareholding pattern |

Reg. 31(1)(a):1 day prior to listing of its securities on the stock exchange(s);

Reg. 31(1)(c):within 10 days of any capital restructuring of the listed entity resulting in a change exceeding 2 % of the total paid-up share capital. |

| 7 |

Regulation 39 |

Issuance of Certificates or Receipts / Letters / Advices for securities and dealing with unclaimed securities. |

Reg. 39(2): The listed entity shall

issue certificates or receipts or advices, as applicable, of subdivision, split, consolidation, renewal, exchanges, endorsements, issuance of duplicates thereof or issuance of new certificates or receipts or advices, as applicable, in cases of loss or old decrepit or worn out certificates or receipts or advices, as applicable within 30 days from the date of such lodgement.Reg. 39(2): The listed entity shall submit information regarding loss of share certificates and issue of the duplicate certificates, to the stock exchange within 2 days of its getting information. |

| 8 |

Regulation 40 |

Transfer or transmission or transposition of securities |

After due verification of the documents, the Listed Company shall register transfers of its securities in the name of the transferee(s) and issue certificates or receipts or advices, as applicable, of transfers; or issue any valid objection or intimation to the transferee or transferor, as the case may be, within a period of 15 days from the date of such receipt of request for transfer:

Transmission requests are processed for securities held in dematerialized mode and physical mode within 7 days and 21 days respectively, after receipt of the specified documents |

| 9 |

Regulation 43 |

Declaration of Dividend |

The company has to declare and disclose the dividend on per share basis only. |

| 10 |

Regulation 46 |

Company Website:.

Listed entity shall disseminate the information as stated in Regulation 46 (2) |

Shall update any change in the content of its website within

2 working days from the date of such change in content. |

| 11 |

Regulation 50 |

Intimation to stock exchange(s). |

Listed Company shall give prior intimation at least 11 working days before the date on and from which the interest on debentures and bonds, and redemption amount of redeemable shares or of debentures and bonds shall be payable. |

| 12 |

Regulation 57 |

Other submissions to stock exchange(s). |

Listed Company shall submit a certificate to the stock exchange within 2 days of the interest or principal or both becoming due that it has made timely payment of interests or principal obligations or both in respect of the non convertible debt securities. |

| 13 |

Regulation 82 |

Intimation and filings with stock exchange(s). |

Intention to issue new securitized debt instruments either through a public issue or on private placement basis :

Reg. 82(2) : Intimation of Meeting

at least 2 working days in advance, excluding the date of the intimation and date of the meeting, regarding the meeting of its board of trustees, at which the recommendation or declaration of issue of securitized debt instruments or any other matter affecting the rights or interests of holders of securitized debt instruments is proposed to be considered |

| 14 |

SCHEDULE III

PART A: DISCLOSURES OF EVENTS OR INFORMATION: SPECIFIED SECURITIES |

Events which shall be disclosed without any application of the guidelines for materiality as specified in sub-regulation (4) of regulation (30) |

(7B) In case of resignation of an independent director of the listed entity, within 7 days from the date of resignation, the following disclosures shall be made to the stock exchanges by the listed entities as mentioned in 7B (i), 7B(ii) & 7B(iii). |

| 15 |

Regulation 106J |

Period of subscription and issue of allotment letter. |

A rights issue shall be open for subscription in India for a period as applicable under the laws of its home country but in no case less than 10 days. |

| 16 |

Regulation 108 |

Application for Listing. |

The issuer / the issuing company, shall, make an application for listing, within 20 days from the date of allotment, to one or more recognized stock exchange(s) along with the documents specified by stock exchange(s) from time to time. |

| 17 |

Regulation 23 |

Corporate governance requirements with respect to subsidiary of listed entity |

The listed entity shall submit within 30 days from the date of publication of its stand alone and consolidated financial results for the half year, disclosures of related party transactions on a consolidated basis, in the format specified in the relevant accounting standards for annual results to the stock exchanges and publish the same on its website. |

| 18 |

Regulation 24A |

Secretarial Audit |

Every listed entity and its material unlisted subsidiaries incorporated in India shall undertake secretarial audit and shall annex with its annual report, a secretarial audit report,given by a company secretary in practice, in such form as may be specified with effect from the year ended March 31, 2019.

On or before: 30th day of May

(within 60 days from the Closure of FY) |

| 19 |

Regulation 23(9) |

The listed entity shall submit within 30 days from the date of publication of its standalone and consolidated financial results for the half year, disclosures of related party transactions on a consolidated basis, in the format specified in the relevant accounting standards for annual results to the stock exchanges and publish the same on its website. |

Disclosure Of Related Party Transactions Pursuant To Regulation 23(9) Of The SEBI (Listing Obligations And Disclosure Requirements) Regulations, 2015 WITHIN 30 days from the date of publication of Financial Results (for half year ) |

| 20 |

SEBI CIRCULAR NOV 26, 2018

LINK |

Initial Disclosure to be made by an entity identified as a Large Corporate.

Within 30 days from the beginning of the FYAnnual Disclosure to be made by an entity identified as a LCTo be submitted to the Stock Exchange(s) within 45 days of the end of the FY) |

APRIL 30

Annexure AMAY 15

Applicable for FY 2020 and 2021

Annexure B1MAY 15

Applicable from FY 2022 onwards

Annexure B2 |

| 21 |

Regulation 30 (6) read with Para A of Part A of Schedule III (except sub para 4 of with Para A of Part A of Schedule III |

The listed entity shall first disclose to stock exchange(s) of all events, as specified in Part A of Schedule III, or information as soon as reasonably possible and not later than twenty four hours from the occurrence of event or information:

Provided that in case the disclosure is made after twenty four hours of occurrence of the event or information, the listed entity shall, along with such disclosures provide explanation for delay

Example :

Proceedings of Annual and extraordinary general meetings of the listed entity. |

24 hours of Occurrence of event |

| 22 |

SCHEDULE III

PART A A

(SUB CLAUSE 7A) |

In case of resignation of the auditor of the listed entity, detailed reasons for resignation of auditor, as given by the said auditor, shall be disclosed by the listed entities to the stock exchanges as soon as possible but not later than twenty four hours of receipt of such reasons from the auditor |

24 hours of Occurrence of event |

| 23 |

SCHEDULE III

PARTA A

(SUB CLAUSE 7B) |

In case of resignation of an independent director of the listed entity, within seven days from the date of resignation, the following disclosures shall be made to the stock exchanges by the listed entities |

within 7 days from the date of resignation |

| 24 |

Regulation 37(1) |

Draft Scheme of Arrangement & Scheme of Arrangement before for obtaining Observation Letter or No-objection letter, before filing such scheme with any Court or Tribunal, in terms of requirements specified by the Board or stock exchange(s) from time to time. |

Before filling the same with any court or tribunal |

| 25 |

Regulation 37(1) read with Section 31 of the Insolvency Code, |

No need to follow Regulation 37 & 94 if restructuring proposal approved as part of a resolution plan by the Tribunal under section 31 of the Insolvency Code, subject to the details being disclosed to the recognized stock exchanges within one day of the resolution plan being approved |

within one day of the resolution plan being approved |

| 26 |

Regulation 42(2) |

The listed entity shall give notice in advance of atleast seven working days (excluding the date of intimation and the record date) to stock exchange(s) of record date specifying the purpose of the record date. (Refer 42(1) Record date) |

7 working days (excluding the date of intimation and the record date) |

| 27 |

Regulation 44(3) |

The listed entity shall submit to the stock exchange, within forty eight hours of conclusion of its General Meeting, details regarding the voting results in the format specified by the Board. |

within 48 hours of conclusion of its General Meeting |

| 28 |

Regulation 31A |

Re-classification of status of a promoter/ person belonging to promoter group to public

an application for re-classification to the stock exchanges has been made by the listed entity consequent to the following procedures and not later than thirty days from the date of approval by shareholders in general meeting: |

Not later than 30 days of general Meeting |

| 29 |

Regulation 50(1)

(Debt OR Non-Convertible Redeemable Preference Shares Or Both) |

Intimation to stock exchange(s).

Listed Company shall give prior intimation at least 11 working days before the date on and from which the interest on debentures and bonds, and redemption amount of redeemable shares or of debentures and bonds shall be payable. |

at least 11 working days |

| 30 |

Regulation 50(3)

(Debt OR Non-Convertible Redeemable Preference Shares Or Both) |

The listed entity shall intimate to the stock exchange(s), at least two working days in advance, excluding the date of the intimation and date of the meeting, regarding the meeting of its board of directors, at which the recommendation or declaration of issue of non convertible debt securities or any other matter affecting the rights or interests of holders of non convertible debt securities or non convertible redeemable preference shares is proposed to be considered. |

at least 2 working days in advance, excluding the date of the intimation and date of the meeting |

| 31 |

Regulation 52 (1) and (2)

(Debt OR Non-Convertible Redeemable Preference Shares Or Both) |

Financial Result

The listed entity shall prepare and submit un-audited or audited financial results on a half yearly basis in the format as specified by the Board within forty five days from the end of the half year to the recognised stock exchange(s) |

Unaudited: 45 days from half end

Audited: 60 days of half end

Sumbit The Copy Of Fr To Debenture Trustees On Same Day After Submission To Stock Exchange |

| 32 |

Regulation 52(5)

(Debt OR Non-Convertible Redeemable Preference Shares Or Both) |

The listed entity shall, within seven working days from the date of submission of the information required under sub- regulation (4),ie information submitted with Financial Results submit to stock exchange(s), a certificate signed by debenture trustee that it has taken note of the contents. |

7 working days of FR |

| 33 |

Regulation 57

(Debt OR Non-Convertible Redeemable Preference Shares Or Both) |

Other submissions to stock exchange(s).

Listed Company shall submit a certificate to the stock exchange within 2 days of the interest or principal or both becoming due that it has made timely payment of interests or principal obligations or both in respect of the non convertible debt securities. |

within 2 days |

| 34 |

Regulation 60(2)

(Debt OR Non-Convertible Redeemable Preference Shares Or Both) |

The listed entity shall give notice in advance of atleast seven working days (excluding the date of intimation and the record date) to stock exchange(s) of record date specifying the purpose of the record date.

(Refer 60(1) Record date) |

7 working days (excluding the date of intimation and the record date) |

| 35 |

Regulation 78(2)

(Obligations of listed entity which has listed its indian depository receipts) |

Record date

The listed entity shall give notice in advance of at least four working days to the recognised stock exchange(s) of record date specifying the purpose of the record date. |

at least 4 working days |

| 36 |

Regulation 82

(Obligations Of Listed Entity Which Has Listed Its Securitised Debt Instruments) |

Intimation and filings with stock exchange(s).

Intention to issue new securitized debt instruments either through a public issue or on private placement basis :

Reg. 82(2) : Intimation of Meeting

at least 2 working days in advance, excluding the date of the intimation and date of the meeting, regarding the meeting of its board of trustees, at which the recommendation or declaration of issue of securitized debt instruments or any other matter affecting the rights or interests of holders of securitized debt instruments is proposed to be considered |

At least 2 working days in advance |

| 37 |

Regulation 87(2)

(Obligations of listed entity which has listed its indian depository receipts) |

Record date

The listed entity shall give notice in advance of atleast seven working days (excluding the date of intimation and the record date) to the recognised stock exchange(s) of the record date or of as many days as the Stock Exchange may agree to or require specifying the purpose of the record date. |

at least 7 working days(excluding the date of intimation and the record date) |

| 38 |

Regulation 87B

(Obligations Of Listed Entity Which Has Listed Its Security Receipts) |

The listed entity shall first disclose to stock exchange(s) of all events or information, as specified in Part E of Schedule III, as soon as reasonably possible but not later than twenty four hours from occurrence of the event or information:

Provided that in case the disclosure is made after twenty four hours of occurrence of the event or information, the listed entity shall, along with such disclosures provide explanation for the delay. |

24 hours of Occurrence of event |

| 39 |

Regulation 87E

(Obligations Of Listed Entity Which Has Listed Its Security Receipts) |

Record date

The listed entity shall give notice in advance of atleast seven working days (excluding the date of intimation and the record date) to the recognised stock exchange(s) of the record date or of as many days as the Stock Exchange may agree to or require specifying the purpose of the record date. |

at least 7 working days (excluding the date of intimation and the record date) |

6. SEBI Takeover Regulations 2011

| Sl. No. |

Regulation No. |

Compliance Particular |

Compliance Period

(Due Date) |

| 1 |

Regulation 30(1) |

Every person, who together with persons acting in concert with him, holds shares or voting rights entitling him to exercise 25% or more of the voting rights in a target company, shall disclose their aggregate shareholding and voting rights as of the 31st day of March, in such target company in such form as may be specified. |

Disclosures shall be made within seven (7) working days from the end of each financial year to;

1) every stock exchange where the shares of the target company are listed; and

2) the target company at its registered office. |

| 2 |

Regulation 30(2) |

The promoter of every target company shall together with persons acting in concert with him, disclose their aggregate shareholding and voting rights as of the thirty-first day of March, in such target company in such form as may |

Disclosures shall be made within seven (7) working days from the end of each financial year to;

1) every stock exchange where the shares of the target company are listed; and

2) the target company at its registered office. |

| 3 |

Regulation 31(1) read with Regulation 28(3) of Takeover Regulations

AUGUST 7, 2019 CIRCULARLINK |

The promoter of every listed company shall specifically disclose detailed reasons for encumbrance if the combined encumbrance by the promoter along with PACs with him equals or exceeds: a) 50% of their shareholding in the company; or b) 20% of the total share capital of the company, |

within 2 (two) working days |

7. SEBI (Prohibition of Insider Trading) Regulations, 2015

| Sl. No. |

Regulation No. |

Compliance Particular |

Compliance Period

(Due Date) |

| 1 |

Regulation 7(2)

“Continual Disclosures” |

Every promoter, employee and director of every company shall disclose to the company the number of such securities acquired or disposed of within two trading days of such transaction if the value of the securities traded, whether in one transaction or a series of transactions over any calendar quarter, aggregates to a traded value in excess of ten lakh rupees (10,00,000/-) or such other value as may be specified; |

Every company shall notify;within two trading days of receipt of the disclosure or from becoming aware of such information |

8. SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018

| Sl. No. |

Regulation No. |

Compliance Particular |

Compliance Period

(Due Date) |

| 1 |

Schedule XIX - Para (2) of ICDR

Read with Reg 108 of SEBI LODR |

“The issuer shall make an application for listing from the date of allotment, within such period as may

be specified by the Board from time to time, to

one or more recognized stock exchange(s)”.

In regard to above, it is specified that Issuer shall

make an application to the exchange/s for listing

in case of further issue of equity shares from the

date of allotment within 20 days (unless

otherwise specified). |

Within 20 days from the date of allotment |

| 2 |

Regulation 162 |

The tenure of the convertible securities of the issuer shall not exceed eighteen months from

the date of their allotment. |

Within 18 monts from date of allotment |

| 3 |

SEBI CIRCULAR

Aug 19, 2019Link |

Application for trading approval to the stock exchange

Listed entities shall make an application for trading approval to the stock exchange/s within 7 working days from the date of grant of listing approval by the stock exchange/s. |

Within 7 working days from grant of date of listing approval |

| 4 |

Regulation 295(1) |

Completion of Bonus Issue:

Within 15 days from the date of approval of the issue by its board of directors – in

cases where shareholders’ approval for capitalization of profits or reserves for

making the bonus issue is not required

Within 2 months from the date of the meeting of its board of directors wherein

the decision to announce bonus issue was taken subject to shareholders’

approval – in cases where issuer is required to seek shareholders’ approval for capitalization of profits or reserves for making the bonus issue. |

Within 15 days from Board Approval ( where shareholder approval is not required)

Within 2 months from Board Approval ( where shareholder approval is required) |

9. SEBI (Buyback of Securities) Regulations, 2018 (Buyback Regulations)

| Sl. No. |

Regulation No. |

Compliance Particular |

Compliance Period

(Due Date) |

| 1 |

Regulation 11 and 24(iv) |

Extinguishment of equity shares in connection with Buyback

The particulars of the security certificates extinguished and destroyed shall be furnished by the company to the stock exchanges where the shares or other specified securities of the company are listed within seven days of extinguishment and destruction of the certificates |

7 days of extinguishment and destruction of the certificates |

• SEBI Circulars – December, 2019

| Sl. No. |

Date& Circular No. |

Particulars of the Circulars |

Link |

| 1 |

Dec 10, 2019

Circular No.: SEBI/HO/IMD/DF2/CIR/P/2019/152 |

Review of investment norms for mutual funds for investment in Debt and Money Market Instruments |

All circulars are available at

https://www.sebi.gov.in/sebiweb/home/HomeAction.dodoListing=yes&sid=1&ssid=7&smid=0 |

| 2 |

Dec 11, 2019

Circular No.: CFD/DIL1/CIR/P/2019/0000000154 |

Filing of Offer Documents under Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018. |

| 3 |

Dec 16, 2019

Circular No.: SEBI/HO/IMD/DF2/CIR/P/2019/155 |

Management and advisory services by AMCs to Foreign Portfolio Investors |

| 4 |

Dec 24, 2019

Circular No.: SEBI/HO/DDHS/DDHS/CIR/P/2019/161 |

Guidelines for filing of placement memorandum - InvITs proposed to be listed |

| 5 |

Dec 24, 2019

Circular No.: CIR/CFD/CMD1/162/2019 |

Format on Statement of Deviation or Variation for proceeds of public issue, rights issue, preferential issue, Qualified Institutions Placement (QIP) etc. |

| 6 |

Dec 24, 2019

Circular No.: SEBI/HO/DDHS/DDHS/CIR/P/2019/167 |

Framework for listing of Commercial Paper-Amendments |

| 7 |

Dec 24, 2019

Circular No.: SEBI/HO/IMD/DF3/CIR/P/2019/166 |

Circular on Investment in units of Mutual Funds in the name of minor through guardian and ease of process for transmission of units |

| 8 |

Dec 27, 2019

Circular No.: SEBI/HO/IMD/DF1/CIR/P/2019/169 |

Measures to strengthen the conduct of Investment Advisers (IA). |

• CIRCULARS TO LISTED COMPANIES – DECEMBER, 2019

| Sl. No. |

Date |

Particulars of the Circulars |

Link |

| 1 |

03.12.2010 |

Guidelines for preferential issue of units and institutional placement of units by a listed Real Estate Investment Trust (REIT) |

LINK |

| 2 |

04.12.2010 |

Guidelines for preferential issue of units and institutional placement of units by a listed Infrastructure Investment Trust (InvIT) |

LINK |

| 3 |

10.12.2010 |

Securities And Exchange Board Of India (Issue Of Capital And Disclosure Requirements) (Fifth Amendment) Regulations, 2019 |

LINK |

| 4 |

12.12.2010 |

Filing of Offer Documents under Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018 |

LINK |

| 5 |

24.12.2010 |

Format on Statement of Deviation or Variation for proceeds of public issue, rights issue, preferential issue, Qualified Institutions Placement (QIP) etc. |

LINK |

| 6 |

24.12.2010 |

Guidelines for filing of placement memorandum - InvITs proposed to be listed |

LINK |

| 7 |

26.12.2010 |

Framework for listing of Commercial Paper-Amendments |

LINK |

| 8 |

27.12.2010 |

Guidelines on Framework for listing of Commercial Paper |

LINK |

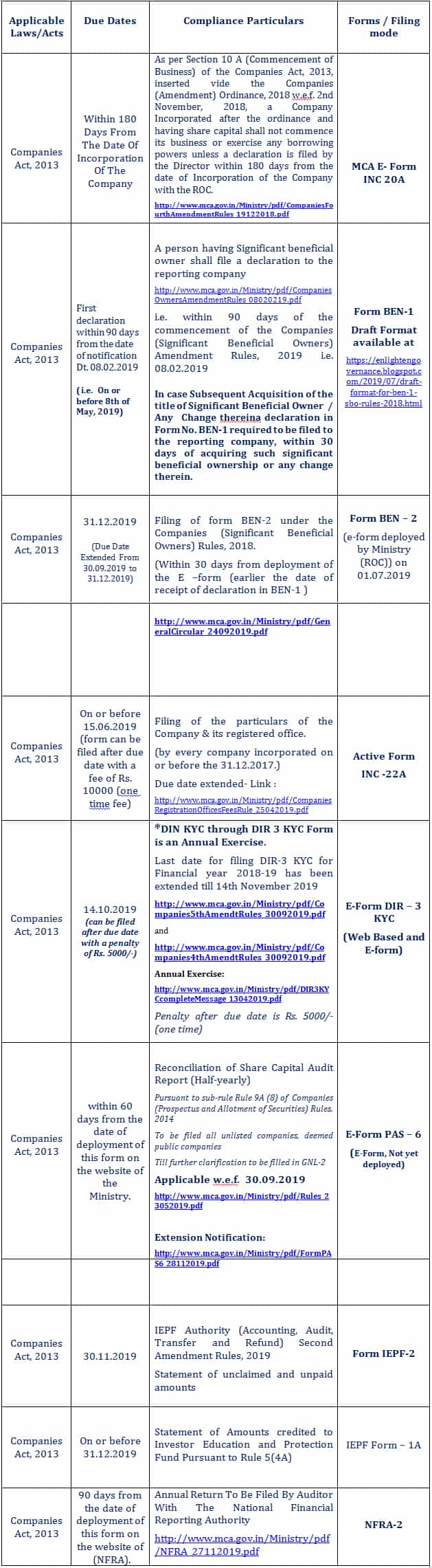

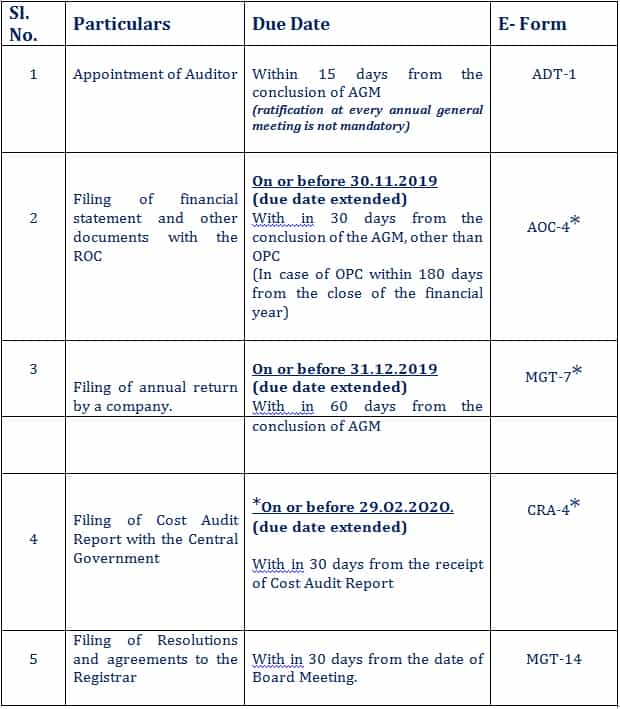

10. COMPLIANCE REQUIREMENT UNDER COMPANIES ACT, 2013 AND RULES MADE THERE UNDER;

• Due dates of ROC Return Filings;

• Due dates of ROC Return Filings;

*Relaxation of additional fees and extension of last date in filing of forms MGT-7 (Annual Return) and AOC-4 (Financial Statement) under the Companies Act, 2013- UT of J&K and UT of Ladakh –

*Relaxation of additional fees and extension of last date in filing of forms MGT-7 (Annual Return) and AOC-4 (Financial Statement) under the Companies Act, 2013- UT of J&K and UT of Ladakh –

extension of time for filing of financial statements for the financial year ended 31.03.2019. Therefore, it has been decided to extend the due date for filing of e-forms AOC-4, AOC-4 (CFS) AOC-4 XBRL and e-form MGT-7 upto 31.01.2020, for companies having jurisdiction in the UT of J&K and UT of Ladakh without levy of additional fee.’

*Relaxation of additional fees and extension of last date of filing of CRA-4 (cost audit report for FY 2018-19 under the Companies Act, 2O13

http://www.mca.gov.in/Ministry/pdf/Circular17_30122019.pdf

• Due dates of LLP Return Filing :

LLP Form 8 (Statement of Account & Solvency) on or before 30.10.2019

The charge details i.e. creation, modification or satisfaction of charge, can be filed through Appendix to e-Form 8 (Interim)

Form LLP -8 can be filed after due date i.e. 30.10.2019 with a penalty of Rs. 100/- per day till the filing is completed.

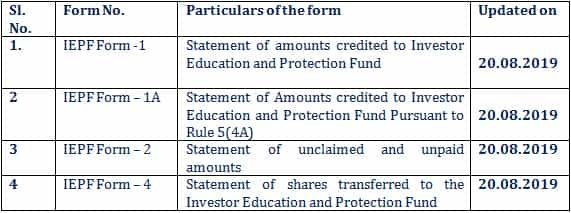

11. Investor Education and Protection Fund

1. MINISTRY OF CORPORATE AFFAIRS on 14.08.2019 has came up with Investor Education and Protection Fund Authority (Accounting, Audit, Transfer and Refund)Second Amendment Rules, 2019.

Applicability :

• The provisions of these rules, Other than rule 6 (i), 6 (iv), 6 (v), 6(vi), 6(vii) and 6 (viii), shall come into force with effect from the 20th day of August, 2019.

• The provisions of rule 6 (i), 6 (iv), 6 (v), 6(vi), 6(vii) and 6 (viii), shall come into force with effect from the 20th day of September, 2019.

Following E-forms revised after these rules :

Source :

Source : http://www.mca.gov.in/Ministry/pdf/IEPFRules_19082019.pdf

2. As part of the revised Investor Education and Protection Fund Authority (Accounting, Audit, Transfer and Refund)Second Amendment Rules, 2019 dated 14th August 2019, Form IEPF-5 is introduced as a web form instead of the existing e- Form w.e.f 20th September 2019.

Form IEPF -5: Application to the Authority for claiming unpaid amounts and shares out of Investor Education and Protection Fund (IEPF)

3. Web form IEPF-5 Pending E- verification report as on 25-Dec-2019

http://www.iepf.gov.in/IEPF/pdf/IEPF5WEBFORM_26122019.xls

4. General Circular 17(Relaxation of additional fee on filling of e-verification report)

http://www.iepf.gov.in/IEPF/pdf/circularNo17_12122019.pdf

• Kindly note that :

Relaxation of additional fees and extension of last date of filing of form IEPF – 1A and Form IEPF -2:Ministry has decided to relax the additional fee payable by Companies on filing of Form IEPF-1A upto 31.12.2019 and Form IEPF -2 (for the purpose of filing statement of unclaimed and unpaid amounts) upto 30.11.2019.

Source : http://www.iepf.gov.in/IEPF/pdf/GeneralCircular1_25102019.pdf

• The Institute of Company Secretaries of India (ICSI) Updates :

ICSI has extended the last date for generation of eCSIN from 31st December, 2019 to 15th January, 2020.

https://www.icsi.edu/media/webmodules/Extension_of_ECSIN.pdf

1. ICSI (Employee Company Secretaries Identification Number (eCSIN)Guidelines), 2019

https://ecsin.icsi.edu/PDF/eCSIN-Guidlines.pdf

2. FAQ’s on eCSIN

https://ecsin.icsi.edu/PDF/UserManual_eCSIN_FAQ.pdf

---------------------------------------------------------------------------------------------------------------------------------

This article is updated till 31st December, 2019 with all Laws / Regulations and their respective amendments.

--------------------------------------------------------THE END-------------------------------------------------------------

For Regular Updates Join : https://t.me/Studycafe

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072