Critical Analysis of CBIC notifications and Circulars issued subsequent to 35th GST Council meeting

Subsequent to 35 th GST Council meeting, the CBIC has issued the order and notifications giving effect to the recommendations of GST council

Subsequent to 35th GST Council meeting, the CBIC has issued the order and notifications giving effect to the recommendations of GST council. Analysis of relevant ones are discussed below and notification and orders are attached for your ready reference:

A. Order for extension of GSTR 9, 9A & 9C date:

| Order No. | Date of issue | Subject |

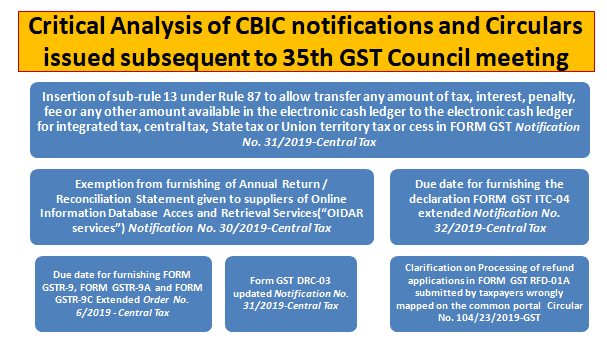

| Order No. 6/2019 - Central Tax | 28-06-2019 | Seeks to extend the due date for furnishing FORM GSTR-9, FORM GSTR-9A and FORM GSTR-9C under section 44 of the Central Goods an Services Tax Act, 2017. |

B. CGST Notifications:

| Notification No. | Description |

| 32/2019-Central Tax dt. 28-06-2019 | Seeks to extend the due date for furnishing the declaration FORM GST ITC-04 |

| 31/2019-Central Tax dt. 28-06-2019 | Amendment in CGST Rules, 2017 which includes: Insertion of Rule 10A to make furnishing of bank account details mandatory (except for those registered persons required to deduct TDS/TCS, granted suo moto registration by proper officer) within 45 days from the date of grant of registration or the date on which the return required under section 39 is due to be furnished, whichever is earlier, Insertion of new Rule 32A to clarify that value of supply for Kerala Flood Cess (KFC) and GST would be same. No GST to be levied on KFC Insertion of new proviso under Rule 46 & 49 providing that the Government can specify the requirement of Quick Response (QR) code on tax invoice / bill of supply Amendment in Rule 66 (TDS) and Rule 67 (TCS) whereby requirement of TDS / TCS deductor to furnish details under Part C of Form GSTR 2A and Form GSTR 4A omitted Insertion of sub-rule 13 under Rule 87 to allow transfer any amount of tax, interest, penalty, fee or any other amount available in the electronic cash ledger to the electronic cash ledger for integrated tax, central tax, State tax or Union territory tax or cess in FORM GST PMT-09 (format attached at the end of the notification) Insertion of Rule 95A for refund of taxes to the retail outlets established in departure area of an international Airport beyond immigration counters making tax free supply to an outgoing international tourist Amendment in Rule 128 to allow extension of 1 month (as may be allowed by the Authority) to standing committee for examining the accuracy and adequacy of anti-profiteering application; and fixation of time limit of 2 months which is extendable by 1 month (as may be allowed by the Authority) for State level screening committee to examine the application on issues of local nature Amendment in Rule 129(6) to extend normal time period from 3 to 6 months for Director General of Anti-profiteering to complete the investigation on receipt of the reference from the Standing Committee Amendment in Rule 133(3)(c) to prescribe deposit of interest @ 18% in the Fund Constituted under Section 57 of State GST Act where the eligible person does not claim return of the amount or is not identifiable Insertion of new proviso after Rule 138(10) to extend validity of e-way bill within 8 hours from the time of its expiry Amendment in Form GSTR 9, to change the time period for disclosing of FY 17-18 details in subsequent year from September 2018 to March 2019. Clarificatory changes in the instructions part of annual return Updation of Form GST DRC-03 |

| 30/2019-Central Tax dt. 28-06-2019 | Seeks to provide exemption from furnishing of Annual Return / Reconciliation Statement for suppliers of Online Information Database Acces and Retrieval Services(OIDAR services) |

| 29/2019-Central Tax dt. 28-06-2019 | Prescribed due date for furnishing FORM GSTR-3B for the months of July, 2019 to September, 2019 which is on or before the 20th day of the month succeeding such month |

| 28/2019-Central Tax dt. 28-06-2019 | Prescribed due date for furnishing FORM GSTR-1 for registered persons having aggregate turnover of more than 1.5 crore rupees for the months of July, 2019 to September, 2019 till the 11th day of the month succeeding such month |

| 27/2019-Central Tax dt. 28-06-2019 | Seeks to prescribe the due date for furnishing FORM GSTR-1 for registered persons having aggregate turnover of up to 1.5 crore rupees for the months of July, 2019 to September, 2019. |

| 26/2019-Central Tax dt. 28-06-2019 | Seeks to extend the due date of filing returns in FORM GSTR-7 |

C. CGST Circulars:

| Circular No. 105/24/2019-GST | Clarification on various doubts related to treatment of secondary or post-sales discounts under GST - reg It is clarified that if the post-sale discount is given by the supplier of goods to the dealer without any further obligation or action required at the dealers end, then the post sales discount given by the said supplier will be related to the original supply of goods and it would not be included in the value of supply, in the hands of supplier of goods, subject to the fulfilment of provisions of sub-section (3) of section 15 of the CGST Act. However, if the additional discount given by the supplier of goods to the dealer is the post-sale incentive requiring the dealer to do some act like undertaking special sales drive, advertisement campaign, exhibition etc., then such transaction would be a separate transaction and the additional discount will be the consideration for undertaking such activity and therefore would be in relation to supply of service by dealer to the supplier of goods. The dealer, being supplier of services, would be required to charge applicable GST on the value of such additional discount and the supplier of goods, being recipient of services, will be eligible to claim input tax credit (hereinafter referred to as the ITC) of the GST so charged by the dealer. |

| Circular No. 104/23/2019-GST | Processing of refund applications in FORM GST RFD-01A submitted by taxpayers wrongly mapped on the common portal Where reassignment of refund applications to the correct jurisdictional tax authority is not possible on the common portal, the processing of the refund claim should not be held up and it should be processed by the tax authority to whom the refund application has been electronically transferred by the common portal. After the processing of the refund application is complete, the refund processing authority may inform the common portal about the incorrect mapping with a request to update it suitably on the common portal so that all subsequent refund applications are transferred to the correct jurisdictional tax authority. |

| Circular No. 103/22/2019-GST | Clarification regarding determination of place of supply in certain cases (I) Services provided by Ports - It is hereby clarified that such services are ancillary to or related to cargo handling services and are not related to immovable property. Accordingly, the place of supply of such services will be determined as per the provisions contained in sub-section (2) of Section 12 or sub-section (2) of Section 13 of the IGST Act, as the case may be, depending upon the terms of the contract between the supplier and recipient of such services. (II) Services rendered on goods temporarily imported in India - Place of supply in case of performance based services is to be determined as per the provisions contained in clause (a) of sub-section (3) of Section 13 of the IGST Act and generally the place of services is where the services are actually performed. But an exception has been carved out in case of services supplied in respect of goods which are temporarily imported into India for repairs or for any other treatment or process and are exported after such repairs or treatment or process without being put to any use in India, other than that which is required for such repairs or treatment or process. In case of cutting and polishing activity on unpolished diamonds which are temporarily imported into India are not put to any use in India, the place of supply would be determined as per the provisions contained in sub-section (2) of Section 13 of the IGST Act. |

| Circular No. 102/21/2019-GST | Clarification regarding applicability of GST on additional / penal interest Generally, following two transaction options involving EMI are prevalent in the trade:- Case 1: X sells a mobile phone to Y. The cost of mobile phone is Rs 40,000/-. However, X gives Y an option to pay in installments, Rs 11,000/- every month before 10th day of the following month, over next four months (Rs 11,000/- *4 = Rs. 44,000/- ). Further, as per the contract, if there is any delay in payment by Y beyond the scheduled date, Y would be liable to pay additional / penal interest amounting to Rs. 500/- per month for the delay. In some instances, X is charging Y Rs. 40,000/- for the mobile and is separately issuing another invoice for providing the services of extending loans to Y, the consideration for which is the interest of 2.5% per month and an additional / penal interest amounting to Rs. 500/- per month for each delay in payment. As per the provisions of sub-clause (d) of sub-section (2) of section 15 of the CGST Act, the amount of penal interest is to be included in the value of supply. The transaction between X and Y is for supply of taxable goods i.e. mobile phone. Accordingly, the penal interest would be taxable as it would be included in the value of the mobile, irrespective of the manner of invoicing. Case 2: X sells a mobile phone to Y. The cost of mobile phone is Rs 40,000/-. Y has the option to avail a loan at interest of 2.5% per month for purchasing the mobile from M/s ABC Ltd. The terms of the loan from M/s ABC Ltd. allows Y a period of four months to repay the loan and an additional / penal interest @ 1.25% per month for any delay in payment. The additional / penal interest is charged for a transaction between Y and M/s ABC Ltd., and the same is getting covered under Sl. No. 27 of notification No. 12/2017- Central Tax (Rate) dated 28.06.2017. Accordingly, in this case the 'penal interest' charged thereon on a transaction between Y and M/s ABC Ltd. would not be subject to GST, as the same would not be covered under notification No. 12/2017-Central Tax (Rate) dated 28.06.2017. The value of supply of mobile by X to Y would be Rs. 40,000/- for the purpose of levy of GST. |

Click Here to Buy CA INTER/IPCC Pendrive Classes at Discounted Rate

About Author

Pratibha Goyal

Admin

This Account belongs to Admistrator of Studycafe.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.