Empanelment of CA Firm for Internal Audit of Assam Skill Development Mission

Empanelment of CA Firm for Internal Audit of Assam Skill Development Mission Scope of Work The primary objective of ' Internal Audit ' is “to ensure …

Table of Contents

Scope of Work

The primary objective of 'Internal Audit' is “to ensure that the financial statements i.e. the Balance Sheet, Income & Expenditure Account and Receipt & Payment Account, give a true & fair view and are free from any material misstatements”. In context of ASDM, Internal Audit also aims at ensuring that the respective program expenditures are eligible for financing under the relevant grant/ credit agreements (under programs supported by development partners) and that the funds have been utilized for the purpose for which they were provided.Internal Audit

Internal Audit is a systematic examination of financial transaction on a regular basis to ensure accuracy, authenticity, compliance with procedure and guidelines. The emphasis under internal audit is not on test checking but on substantial checking of transactions. It is an ongoing appraisal of the financial health of an entity to determine whether the financial management arrangements (including internal control mechanisms) are effectively working and to identify areas of improvement to enhance efficiency. Independent Chartered Accountant firm shall be appointed as Internal Auditor at Assam Skill Development Mission to undertake periodical audit and report on vital parameters which would depict the true picture of financial and accounting health of the project.Objective

The key objectives of the Internal Audit include: -- To ensure voucher/evidence based payments to improve transparency.

- The ensure accuracy and timelines in maintenance of books of accounts.

- To ensure timelines and accuracy of periodical financial statements.

- To improve accuracy and timelines of financial reporting especially at individual project levels and consolidated basis.

- To ensure compliance with laid down systems, procedures and policies.

- To regularly track, follow up and settle advances on a priority basis.

- To assess & improve overall internal control systems.

Scope of Audit

The responsibilities of the internal auditor shall include reporting on the adequacy of internal controls, the accuracy and propriety of transactions, the extent to which assets are accounted for and safeguarded and the level of compliance with financial norms and procedures of the operational guidelines. The internal audit shall be carried out both at State as well as District level as per requirement.Eligibility Criteria

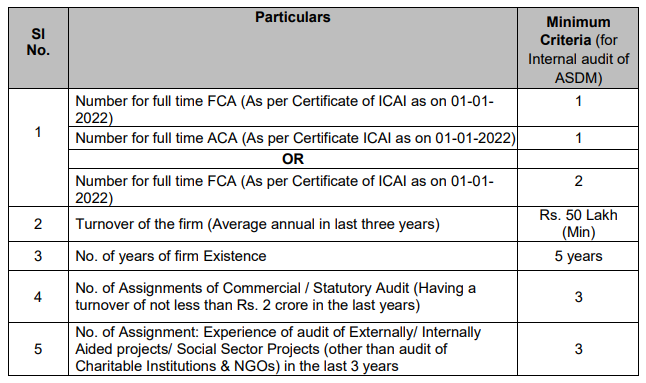

1. The firm must be empaneled with C & AG for the year 2021-22 and the particulars of the Firm H.O., B.O. and Partners and paid Chartered Accountants should match with the certificate issued by ICAI not before 1st January, 2022, without which the application of the firm would not be considered. Proof of empanelment with C&AG to be attached. 2. The firms having H.O. only within the state capital of the same State for which the proposal is given may be given preference. (Such head office should be existed within the state for not less than three years as per the ICAI Certificate). 3. Firms must qualify following minimum criteria: i. Any firm not qualifying on these minimum criteria need not apply as its proposal shall be summarily rejected.

ii. Supporting Documents for Eligibility Criterions:

Following supporting documents must be submitted by the firm along with the technical proposal:

i. Any firm not qualifying on these minimum criteria need not apply as its proposal shall be summarily rejected.

ii. Supporting Documents for Eligibility Criterions:

Following supporting documents must be submitted by the firm along with the technical proposal:

a. For Sl. No. 1 & 3 above, the firm must submit an attested copy of Certificate of ICAI as on 01.01.2022.

b. For Sl. No. 2, the firm must submit, a copy of the Audited Balance Sheet & Profit & Loss Account for the last three years otherwise a Certificate issued by any C.A. Firm may also be provided in this regard giving the break-up of Fees (Audit Fee, Taxation and Others).

c. For Sl. No. 4 & 5, the firm must submit a copy of the appointment letters from the auditee organizations. Branch Audit of any Bank shall not be considered while taking into account the total number of assignments.

About Author

Sushmita Goswami

Content Manager

Studycafe

Studycafe  New Delhi , Delhi, India

New Delhi , Delhi, India 886

886My Recent Articles

- What to Consider When Choosing an Online Trading Platform?

- Post Office Franchise Scheme: Take Post Office Franchise at Rs 5000 and Earn Commission upto 20%; Check Details Here

- IAN invests INR 4.5 crore in Fintech NBFC Indium Finance

- UPI a Digital Public Good, No Charges in Consideration: Finance Ministry

- ITR Filing Penalty: Check Taxpayers Exempt from Paying a Late Fee even Missing the Deadline

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts