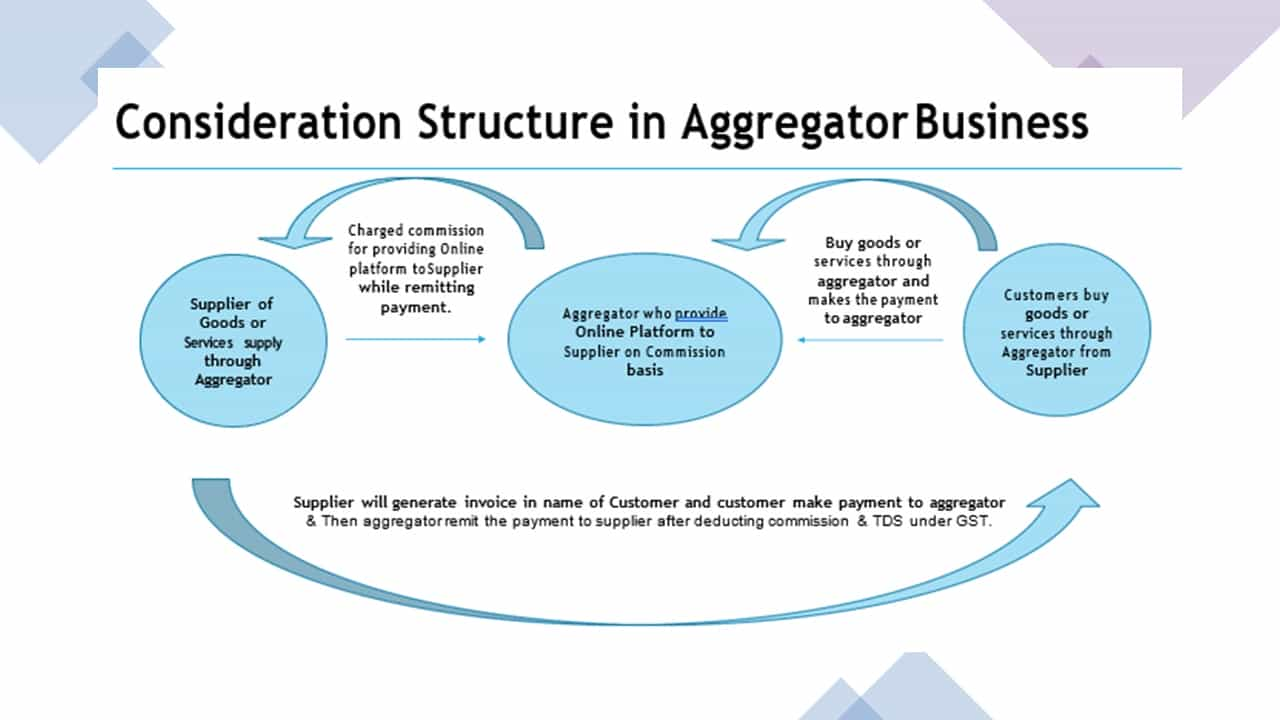

GST on Ecommerce industry

Place of Supply and Type of GST charged under GST under different scenario 1. Place of Supply of Services: In Case of Supply of service made through …

Table of Contents

Place of Supply and Type of GST charged under GST under different scenario

As discussed above place of Supply will be as follow in different scenario & type of GST:

1. Buyer, Seller & E-commerce in same state:

Place of Supply will be that State & CGST & SGST to be charged

2. Buyer, Seller & E-Commerce in different states:

Service from E-commerce to Supplier of Service – Place of supply will be place of supplier if registered or address of supplier available with E-Commerce otherwise place of E-commerce & IGST to be charged.

Service from Supplier to Consumer through E-comm. – Place of supply will be place of consumer if registered or address of consumer available with supplier otherwise place of Service Provider & IGST to be charged.

3. E-Commerce & Buyer in same state & supplier in other state:

1. Place of Supply of Services:

In Case of Supply of service made through E-Commerce operator following two Transaction take place: 1. Service by E-Commerce operator to Supplier of service through E-Commerce. 2. Supplier of service provide service to final consumer through E-Commerce operator. In such case Place of supply will be as follow:| S. No | Service Provide | Registered / Unregistered under GST | Place of Supply |

| 1 | E-Commerce to Supplier of Service through E-Commerce | Registered | Place of such Registered Recipient |

| Unregistered | If address available then place of such recipient otherwise place of E- Commerce operator | ||

| 2 | Supplier of Service to Consumer through E-Commerce | Registered | Place of such Registered Recipient |

| Unregistered | If address available then place of such recipient otherwise place of E- Commerce operator |

- E-Commerce to Supplier of service - Place of supply will be place of supplier if registered or address of supplier available with E- Commerce otherwise place of E-commerce. IGST to be charged if supplier registered or address available otherwise CGST & SGST to be charged.

- Supplier to Consumer – Place of supply will be place of consumer if registered or address of consumer available with supplier otherwise place of supply of Service Provider. IGST to be charged if supplier registered or address available otherwise CGST & SGST to be charged.

- E-Commerce to Supplier of service –

- Supplier to Consumer –

- E-Commerce to Supplier of service – Same as per point 3.

- Supplier to Consumer - Same as per point 1

- E-Commerce to Supplier of service – Same as per point 3.

- Supplier to Consumer - Same as per point 3

TCS under GST by E-Commerce Operator:

1. E-Commerce operator require to collect TCS under GST from Net Value of Taxable Supply made through it by the other supplier & E- Commerce operator collect the consideration on behalf of the supplier. 2. TCS rate is 1% when Inter-State Supply & 0.5% of CGST & 0.5% of SGST in case of Intra-State supply. 3. E-Commerce operator need to an obtain State-wise registration for TCS purpose in which it has obligation to collect tax. 4. TCS should be CGST & SGST or IGST is based on GST charged by supplier. i.e. if supplier charged CGST & SGST on its supply TCS will be CGST & SGST or supplier charged IGST then TCS will be IGST.TDS under Income Tax Law:

1. E-Commerce operator shall deduct TDS also under section 194O under Income Tax Act, 1961 from the payment made to supplier (Individual or HUF) at the Rate 1% in case of supplies exceed Rs. 50,00,000/- with effect from 01st October, 2020. Please refer all the relevant sections, rules, amendments and consider all the necessary requirements as applicable. The author is not responsible for any losses caused or incurred. The content is merely for sharing knowledge. The author can be reached at [email protected] or 9819244185. A Practicing Chartered Accountant with over 4 years of rich experience in Company Law, Audits, Accounts & taxation. She is a writer at her own blog https://insights.buddingbusiness.com/. She is keen in streamlining business accounts of the Company and provide Startup consultancy.About Author

SWETA MAKWANA

Founder

Makwana Sweta & Associates

Makwana Sweta & Associates Mumbai, Maharashtra, India

Mumbai, Maharashtra, India 2

2Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts