GST on Goods and Transport Agency Services: Know the New GST Rates and ITC Conditions for GTA

GST on Goods and Transport Agency Services: Know the New GST Rates and ITC Conditions for GTA This article discusses new GST Rates and Input Tax Cred…

Table of Contents

GST on Goods and Transport Agency Services: Know the New GST Rates and ITC Conditions for GTA

This article discusses new GST Rates and Input Tax Credit (ITC) Conditions Applicable in the case of Services provided by the Goods and Transport Agency (GTA).

GTA has been considered the backbone of the Indian Economy. That is the reason, this sector has always got special attention and benefits in the Goods and Service Tax (GST) Regime as well. One of the benefits given to this sector was the applicability of the Reverse Charge Mechanism (RCM) where the responsibility of GST Payment comes to the Service Receiver.

Prior to 18th July 2022, GTA had two Options:

- Payment of 12% GST on Forward Charge Mechanism and Availment of Input Tax Credit.

- Applicability of 5% GST on RCM, where the responsibility of GST Payment comes to the Service Receiver.

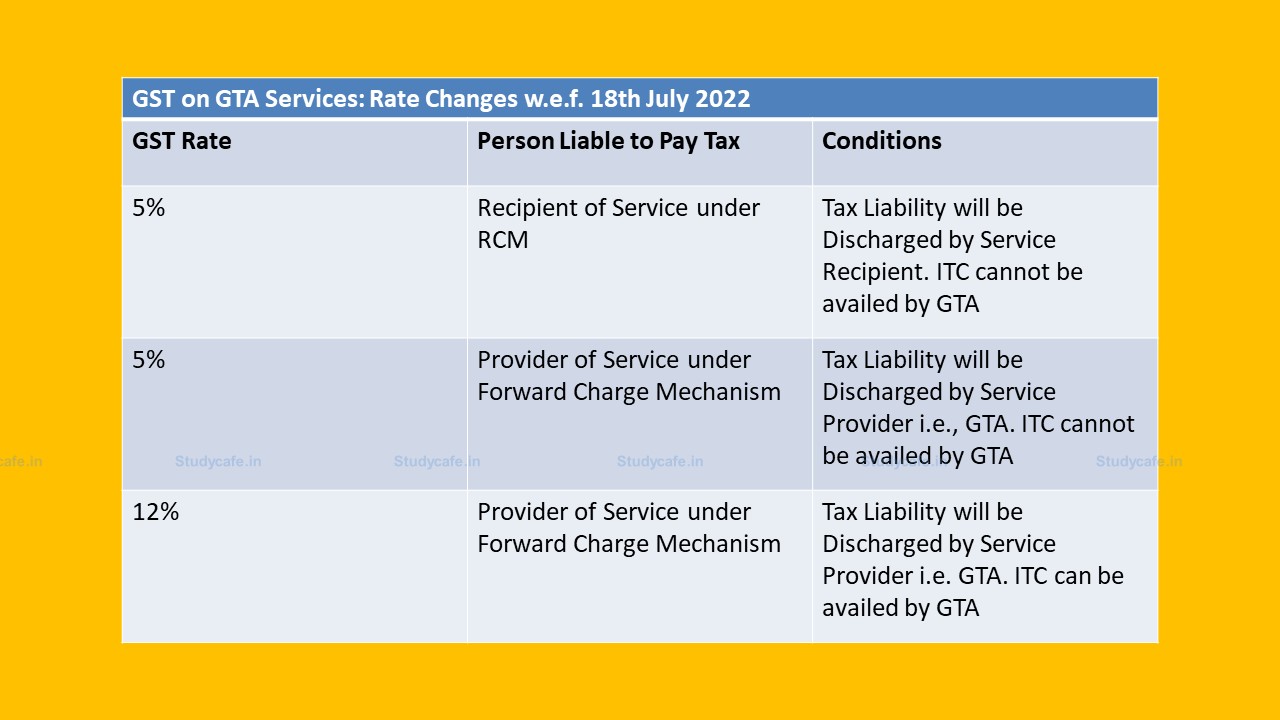

Rate Changes w.e.f. 18th July 2022

Vide Notification No. 03/2022-Central Tax (Rate) dated 13th July 2022 the GTA is being given the option to pay GST at the rate of 5% on Forward Charge Mechanism without the Availment of Input Tax Credit. Options with GTA w.e.f. 18th July 2022:- GTA can Opt for Payment of 12% GST on Forward Charge Mechanism and Availment of Input Tax Credit.

- GTA can Opt for Payment of 5% GST on Forward Charge Mechanism without Availment of Input Tax Credit.

- Applicability of 5% GST on RCM, where the responsibility of GST Payment comes to the Service Receiver.

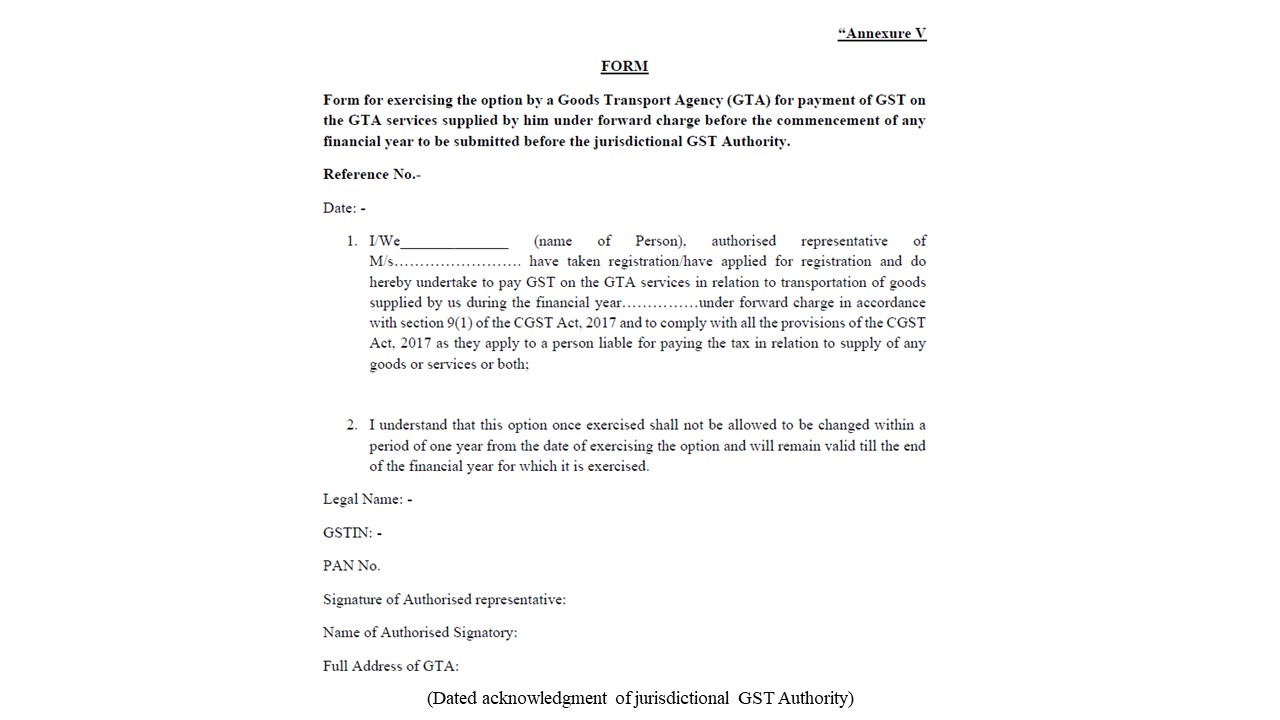

How to Opt for New GST Rate?

Form for exercising the option by a Goods Transport Agency (GTA) for payment of GST on the GTA services supplied by him under forward charge before the commencement of any financial year to be submitted before the jurisdictional GST Authority.

Due Date for Exercising the Option

The last date for exercising the above option for any financial year is the 15th of March of the preceding financial year. The option for the financial year 2022-2023 can be exercised by 16th August 2022. Provided further that invoice for supply of the service charging GST at the rate of 5% may be issued during the period from the 18th July 2022 to 16th August 2022 before exercising the option for the financial year 2022-2023 but in such a case the supplier shall exercise the option to pay GST on its supplies on or before the 16th August 2022.Declaration to be made on Tax Invoice

Declaration I/we have taken registration under the CGST Act, 2017 and have exercised the option to pay tax on services of GTA in relation to transport of goods supplied by us during the Financial Year _____ under forward charge.Exemption Withdrawn

Earlier there was exemption on services provided by GTA where (a) Goods, where consideration charged for the transportation of goods on a consignment transported in a single carriage does not exceed one thousand five hundred rupees; (b) goods, where consideration charged for transportation of all such goods for a single consignee does not exceed rupees seven hundred and fifty; Same is now withdrawnAbout Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts