GST Ready Reckoner on Recent Changes on Real Estate

GST on Real Estate A Ready Reckoner on Recent Changes The Article discusses all the decisions taken in the 33rd and 34th GST council meeting

GST on Real Estate A Ready Reckoner on Recent Changes

The Article discusses all the decisions taken in the 33rd and 34th GST council meetings held on 24th feb, 2019 and 19th march, 2019 government has bought out transformational changes in GST law and tax rates for real estate sector w.e.f. 1-4-2019

It covers salient features of new tax structure recommonded for real estate sector, i.e, construction service. It discusses the applicability of GST on various projects depending on nature of the project (REP, RREP). It also discusses the taxability based on the progress of construction (on going project, new project). Precisely, this book covers the applicable GST on residential, commercial constructions, affordable housing and the guidelines and requisite conditions as envisaged in Notifications Nos. 03/2019-CTR to 08/2019-CTR (all dated 29.03.2019). However, this book does not discuss the taxability of Works Contract Service.

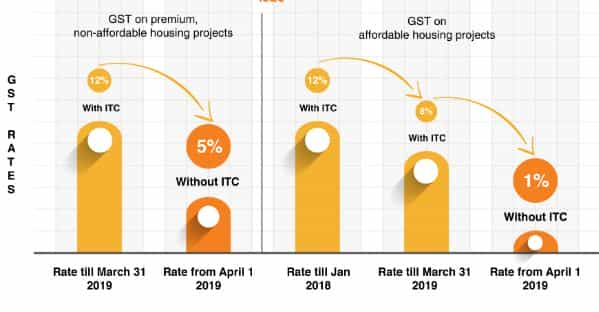

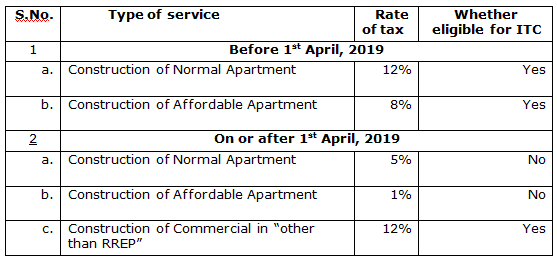

1.) TAX STRUCTURE BEFORE AND AFTER 1ST APRIL, 2019

Before going deep into the taxability or otherwise of the Real Estate Projects, lets try to understand certain concepts relating to Real Estate Sector.

From the above, it can be understood that the features that distinguish old tax structure from new tax structure are; change in the tax rates and fac ility to avail ITC. Each tax structure is having its own advantages. New tax structure, for instance, provides for reduced tax rates, old one, on the other hand, allows a builder to avail ITC. Based on the progress of the construction and ITC availed/to be availed, sometimes it may be beneficial for an ongoing project to continue with the old tax structure. Keeping this in view, the facility of choosing old tax structure is still provided to the builders of ongoing project, while such facility is not available to those projects which commence on or after 1st April, 2019 (new project, in short). It is, thus, pertinent to know the definition of ongoing project.

TO DOWNLOAD FULL BOOK CLICK HERE

About Author

Anjali Yadav

NA

Delhi, Delhi, India

Delhi, Delhi, India 104

104My Recent Articles

- GSTR-9 & GSTR -9C more simplified & last dates of submission extended

- Exemptions of GST on TDR and FSI for construction of residential apartments

- GST Features of Making Payment on Voluntary Basis (Form GST DRC-03)

- GST E-Invoice System concept note, Standard, Schema and Template

- GST Online processing of refund applications and single authority disbursement implemented

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.