GST Refund claim should not be rejected due to shortcoming of GSTN: High Court:

The High Court ordered for payment of GST Refund along with the interest, which could not be paid due to a technical glitch of the GST Network.

GST Refund

Table of Contents

GST Refund claim should not be rejected due to shortcoming of GSTN: High Court

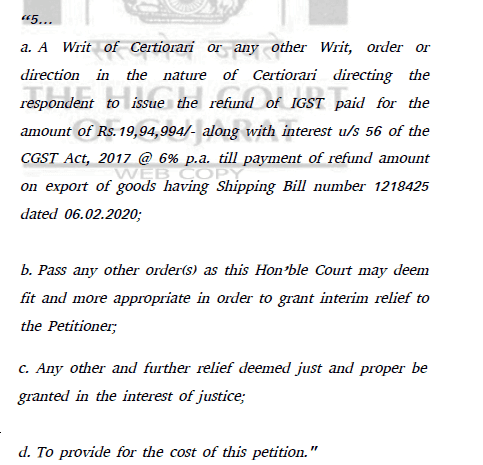

This petition is preferred seeking to question the action of the respondent authority in non-issuance of the refund of Integrated Goods and Services Tax (‘the IGST’ hereinafter) along with the interest.

The petitioner is a Limited Liability Partnership Firm having LLP No.AAM-1202 and is engaged in trading of Ceramics and Tiles. Assessee was formerly known as Azuvi International LLP and has changed its name to Aartos International LLP from 08.04.2019. The name updation was intimated to the Bank and all the relevant government departments including GST, Income Tax, ROC and Customs.

The petitioner exported the goods in the month of February and March 2020 and shipping bills along with GSTR-3B and GSTR-1 for substantiation of this averment are forming the part of the record. It is averred by the petitioner that out of three export invoices, the refund has been received of IGST paid at the time of export of Rs.20.45 Lakh (rounded of). On three invoices being invoice Nos. E54/2019-20, E67/2019-20 and E68/2019-20 dated 08.03.2020 and the duty drawback of all the three invoices also had been received on 27.02.2020 and 04.04.2020.

The petitioner since did not receive the refund of the IGST paid on export invoice No.E54/2019-20 dated 06.02.2020 of Rs.19,94,994/-, it had attempted to approach the department. As there is a portal of Department of Administrative Reforms and Public Grievance (‘the CPGRAMS’ hereinafter) on 14.02.2022, however for two months, there was no response.

It is the say of the petitioner that the provision of Sections 16 and 54 of the IGST Act and Rule 96 of the CGST Rules if are considered, then the amount claimed as refund would become due to the petitioner and an order need to be passed by the respondent sanctioning 90% of the amount claimed in Form RFD-04 within a period of not exceeding 07 days from the date of acknowledgment received. The refund applications as per Rule 96 of the CGST Rule, 2017 are the payment of tax and shipping bills once the goods are imported with payment of tax. However, the respondent had not issued the order and hence, this petition with the following prayers:

What did Court say?

8. It is quite clear from this that when Section 54(6) of the CGST read with Section 91(2) of the CGST Rules, the amount is required to be refunded and it is the respondent’s obligation to make an order sanctioning 90% of the amount claimed in Form RFD-04 within a period of seven days from the date of acknowledgment received. There are no separate applications for the refund. The shipping bills are deemed to be refund applications when the goods are exported with payment of tax. 9. Admittedly, in the present case, it appears to be the difficulty at the end of the GST network or some error in the software itself which would require a cure. When nothing is being disputed and for two of the tax invoices the refund has already been credited in the account of the petitioner, this appears to be a short coming of the software itself. Everything since is being done electronically and this automatically grant of refund after validating the shipping bill data available in ICS against the GST returns, data transmitted by GSTN, if there is any difficulty at the level of the mismatch or the processing of the claim of the refund, it becomes a duty of the GSTN to look into the same. Finding fault with the officer concerned also will not help as they are largely dependent on the network. It is good to be driven through the machines in this electronic age and this automatic grant of refund which is system driven rather then the officer driven at the same time unless there is a constant vigil on the part of the GSTN and also an endeavor to rectify the mismatch or the short comings of the software, the issues are bound to multiply. 10. We are constrained to observe this as in many of the matters we notice that on one hand there is laudable objectives of making it all system driven and on the other hand the limitations of the system which are otherwise required to be addressed to at the level of the GSTN. There is some kind of apathy. We, would, therefore, also recommend that if the authority concerned deems it appropriate, let there be a direct communication also with the GSTN in the portal itself which could be also response based. Therefore, instead of the individual department pleading through their senior through the GSTN, the Assessee of those consultants and others could communicate with the GSTN on portal if a feature like “MAY I HELP YOU” is created by the authority on due deliberation or through the “Grievance Reddressal Mechanism”. Essentially, this is for the purpose of lessening the Court work also as per such details the Assessees are not to be dragged to the Court when in fact there is nothing for the Court to adjudicate except pointing out to the limitation of the software of the respondent department. 11. With this direction, the petition is ALLOWED. Let the refund of IGST be paid for the amount of Rs.19,94,994/- with interest at the rate of 6% and with all consequential benefits within a period of two weeks from the date of receipt of a copy of this order. 12.Over and above the regular mode of service, direct service through e-mode on official email address is also permitted. Click on the link given below to download the orderAbout Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts