Reetu | Oct 3, 2023 |

GSTN introduced Form DRC-01C to handle ITC mismatches between GSTR-2B and GSTR-3B

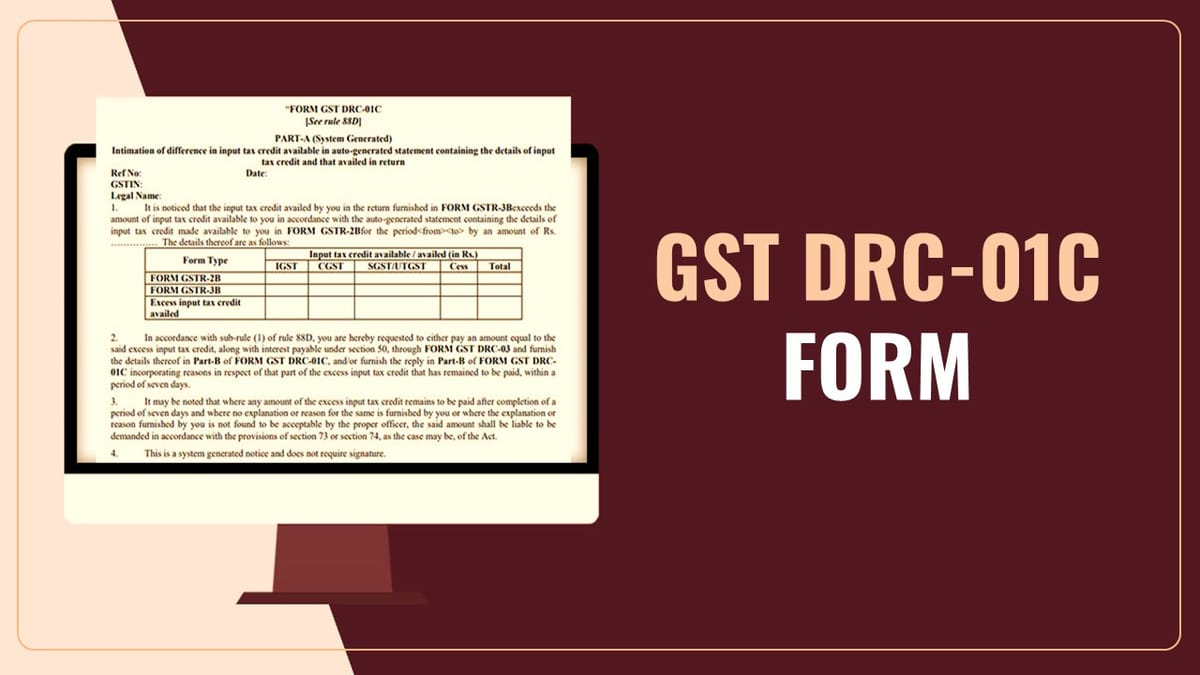

The Goods and Services Tax Network (GSTN) has enabled Form DRC-01C to handle Input Tax Credit mismatches between GSTR 2B and GSTR 3B, in accordance with newly inserted rule 88D of the Central Goods and Services Tax Rules, 2017.

This above-mentioned rule was notified via a Central Tax Notification released in August 2023.

Rule 88D of the CGST Rules

“88D. Manner of dealing with difference in input tax credit available in auto-generated statement containing the details of input tax credit and that availed in return-

(1) Where the amount of input tax credit availed by a registered person in the return for a tax period or periods furnished by him in FORM GSTR-3B exceeds the input tax credit available to such person in accordance with the auto-generated statement containing the details of input tax credit in FORM GSTR-2B in respect of the said tax period or periods, as the case may be, by such amount and such percentage, as may be recommended by the Council, the said registered person shall be intimated of such difference in Part A of FORM GST DRC- 01C, electronically on the common portal, and a copy of such intimation shall also be sent to his e-mail address provided at the time of registration or as amended from time to time, highlighting the said difference and directing him to—

(a) pay an amount equal to the excess input tax credit availed in the said FORM GSTR-3B, along with interest payable under section 50, through FORM GST DRC-03, or

(b) explain the reasons for the aforesaid difference in input tax credit on the common portal, within a period of seven days.

(2) The registered person referred to sub-rule (1) shall, upon receipt of the intimation referred to in the said sub-rule, either,

(a) pay an amount equal to the excess input tax credit, as specified in Part A of FORM GST DRC- 01C, fully or partially, along with interest payable under section 50, through FORM GST DRC-03 and furnish the details thereof in Part B of FORM GST DRC-01C, electronically on the common portal, or

(b) furnish a reply, electronically on the common portal, incorporating reasons in respect of the amount of excess input tax credit that has still remained to be paid, if any, in Part B of FORM GST DRC-01C, within the period specified in the said sub-rule.

(3) Where any amount specified in the intimation referred to in sub-rule (1) remains to be paid within the period specified in the said sub-rule and where no explanation or reason is furnished by the registered person in default or where the explanation or reason furnished by such person is not found to be acceptable by the proper officer, the said amount shall be liable to be demanded in accordance with the provisions of section 73 or section 74, as the case may be.”

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"