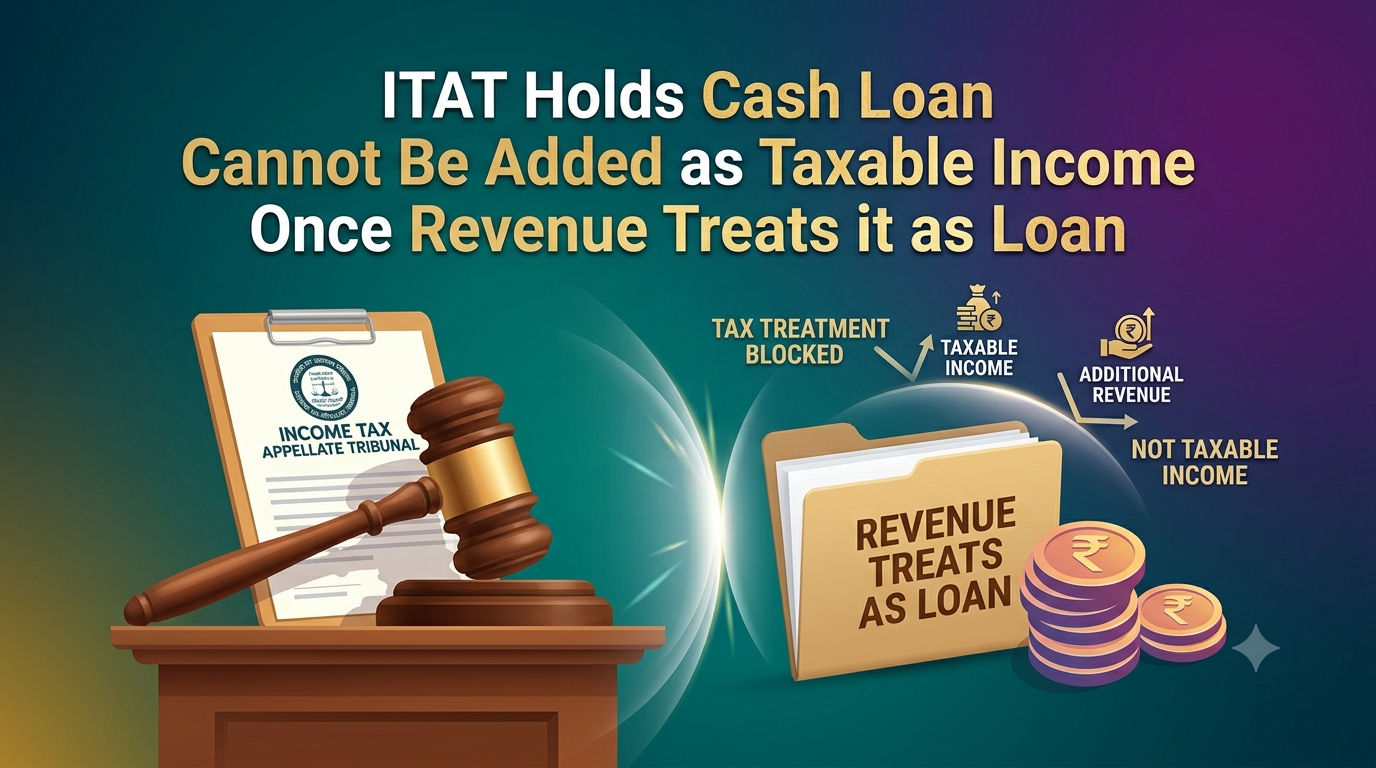

ITAT Holds Cash Loan Cannot Be Added as Taxable Income Once Revenue Treats it as Loan :

The ITAT Mumbai held that alleged violation of Section 269SS can attract only penalty under Section 271D and not income tax addition.

ITAT deletes Rs 10 lakh addition

The Income Tax Appellate Tribunal (ITAT) Mumbai has held that where the Revenue itself accepts a transaction as a cash loan, the amount cannot simultaneously be assessed as taxable income.

The assessee filed her return of income for Assessment Year 2012-13, declaring a total income of Rs 600,570. Later, the AO received information from the Investigation Wing alleging that the assessee had accepted a cash loan of Rs 10 lakh from M/s Evergreen Enterprises during the financial year. Based on this information, reassessment proceedings were initiated under Sections 147 and 148 of the Income Tax Act.

During reassessment, the AO treated the cash loan as violating Section 269SS and initiated penalty proceedings under Section 271D and also added the same amount to the assessee's income.

The CIT(A) upheld the addition, making the assessee file an appeal before the tribunal.

The Tribunal observed that the Income Tax Act particularly provides for a penalty under Section 271D where a cash loan is accepted in violation of Section 269SS. Therefore, the legal consequence is the penalty provisions, which do not extend to treating the loan amount itself as taxable income.

The Tribunal further noted that the AO had already initiated penalty proceedings under Section 271D after acknowledging the transaction as a loan. Having adopted that position, the revenue could not legally assess the same amount as income.

The Tribunal held that once the revenue itself accepts that the receipt is a loan transaction, the same amount cannot be simultaneously treated as unexplained income. Accordingly, it allowed the appeal of the assessee while deleting the addition of Rs 10 lakh.

Citation Details

Appeal Number

ITA No. 902/MUM/2026

Assessment Year

2012-13

Case Citation

Ulka Chandrashekhar Nair Vs Income Tax Officer (ITAT Mumbai); ITA No. 902/MUM/2026; 29/06/2026; 2012-13

Case Name

Ulka Chandrashekhar Nair Vs Income Tax Officer

Court

ITAT Mumbai

Judgement Date

29/06/2026

About Author

Saima

Content Writer

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 146

146My Recent Articles

- ITAT Denies Deduction on Donation to Kisan Party of India As Claim Lacked CredibilityPremium

- ITAT Denies Section 80GGC Deduction on Political Donation Found to be Accommodation EntryPremium

- ITAT Holds Business Loss from Genuine Share Transactions Cannot Be Taxed as Unexplained Cash Credit Under Section 68Premium

- ITAT Upholds Deletion of Rs 5.61 Crore Addition as AO Failed to Independently Verify Alleged Accommodation EntriesPremium

- AAAR Rules 5% GST on E-Rickshaw CKD Kits Applicable Only When Complete Unassembled Vehicle is Supplied Premium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts