ITO’s Rejection of Books and 8% Profit Estimation Requires Fresh Appellate Examination; ITAT Remands Matter to CIT(A):

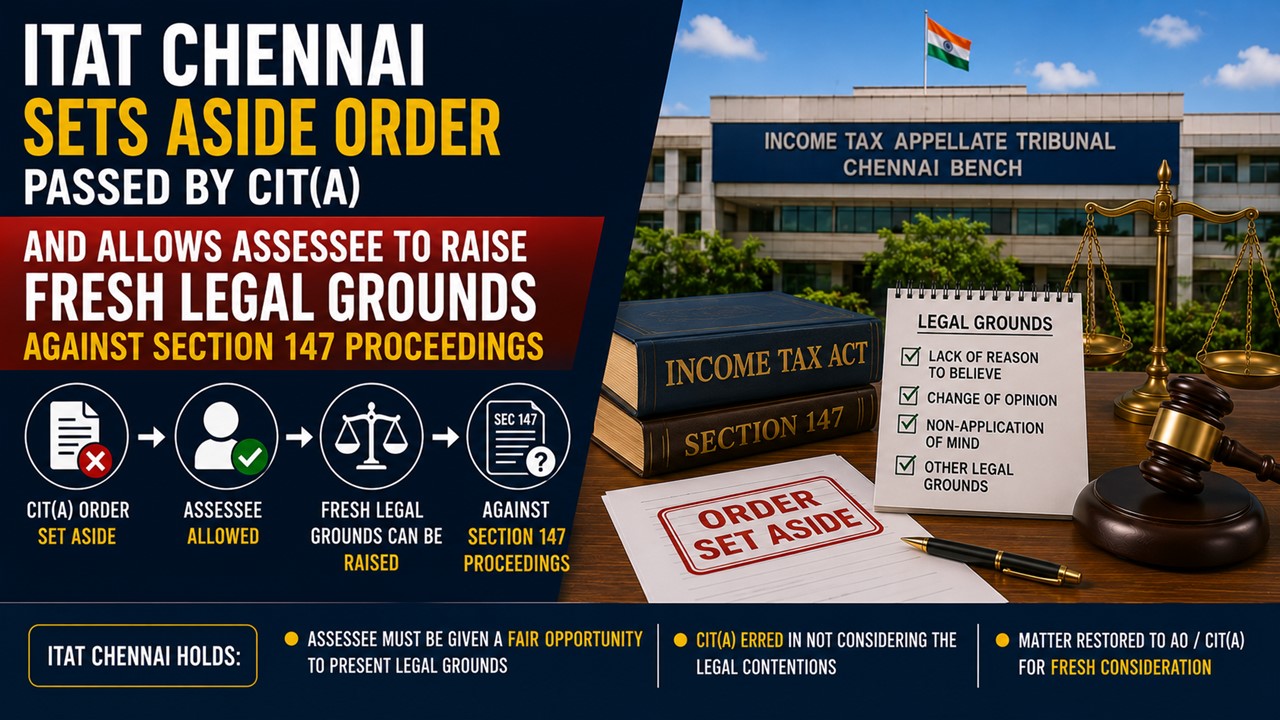

The Income Tax Appellate Tribunal (ITAT) Chennai has set aside the order passed by the CIT(A) and restored the matter for fresh adjudication.

ITAT Chennai Restores Reassessment Dispute to CIT(A)

ITO’s Rejection of Books and 8% Profit Estimation Requires Fresh Appellate Examination; ITAT Remands Matter to CIT(A)

The Income Tax Appellate Tribunal (ITAT) Chennai set aside the order passed by the CIT(A) to decide the appeal afresh in accordance with law after providing an adequate opportunity of hearing to the assessee.

The assessee is an individual engaged in the business of purchase and sale of paddy through the proprietary concern named V. Gowri Traders and had not filed her return of income for assessment year 2018-19 and according to the information available with the Department regarding cash deposits amounting to Rs.72.45 lakh and cash withdrawals aggregating to Rs.3.04 crore, the AO initiated proceedings under Sections 147 and 148 of the Income Tax Act, 1961.

In response to the notice issued under Section 148, the assessee filed a return declaring a total income of Rs 5.56 lakh and explained that the cash withdrawals were utilised for making payments to small farmers from whom paddy was procured. However, the assessee failed to furnish complete books of account and supporting documents.

The AO invoked Section 145 and estimated income by applying a net profit rate of 8% on the disclosed turnover of Rs 2.48 crore. Aggrieved by the assessment order, the assessee preferred an appeal before the CIT(A), which confirmed the additions made by the AO.

The Tribunal observed that although the assessee had failed to properly present the appeal before the CIT(A), ordinarily an assessee should be afforded an effective opportunity to substantiate the case. The Bench further noted that adjudication of issues on merits requires an examination of facts and records and the Tribunal considered it appropriate to restore the matter to the file of the CIT(A).

Accordingly, the impugned order was set aside and the appeal of the assessee was allowed for statistical purposes.

About Author

Saima

Content Writer

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 228

228My Recent Articles

- ITAT Grants Fresh Opportunity to Blind Retired Employee And Sets Aside Assessment Passed Without Considering DisabilityPremium

- SBI Cannot Be Treated as Assessee in Default for Non-Deduction of TDS on LTC Payments Made Under Court's Interim OrderPremium

- ITAT Allows 15% Concessional Tax Rate Under Section 115BAB Where Form 10-ID Was Filed Within Extended Due DatePremium

- ITAT Holds Delay in Appeal Is Justified Due to Non-Service of Order on Updated EmailPremium

- ITAT Holds Fresh Application for Registration Under Sections 12AB and 80G Must Be Examined IndependentlyPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts