ITR Refund Delay Despite Timely Filing: Refunds May Take Till December 2026:

Grievance closure does not guarantee refund as statutory timelines allow processing till December 2026

Income Tax Refund Delays Continue Despite Timely ITR Filing

ITR Refund Delay Despite Timely Filing: Refunds May Take Till December 2026

Filing an income tax return (ITR) within the due date does not necessarily guarantee timely processing or a refund, as reflected in a grievance response recently issued by the Income Tax Department.

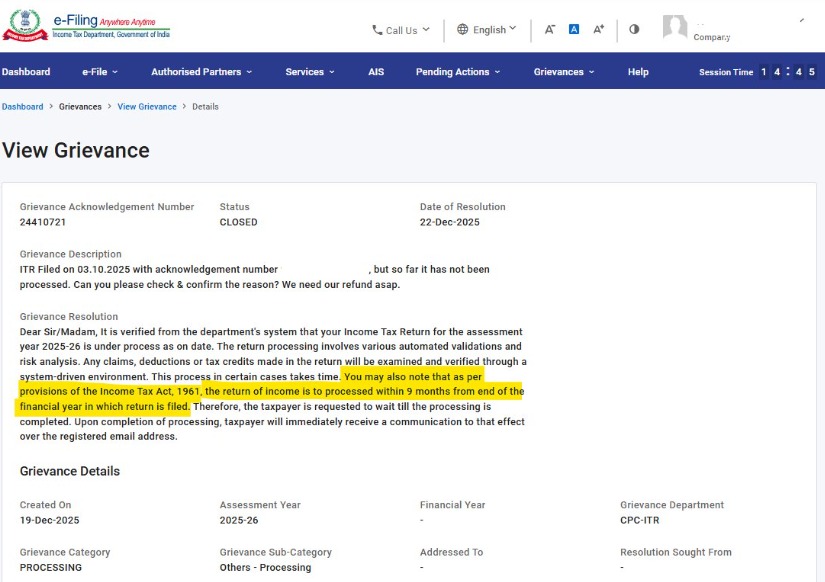

In a recent case, the taxpayer had filed the return for FY 2024–25 (AY 2025–26) on time. With no update on processing, a grievance was raised on the income tax portal. While the grievance has since been marked as closed, the return itself continues to remain under processing.

The Department’s reply states that the return “may be processed within nine months from the end of the financial year.” Since the financial year ends on 31 March 2025, this effectively allows processing to continue until December 2026.

Tax professionals point out that closure of a grievance often only confirms that the case falls within statutory timelines and does not imply any acceleration of refund issuance.

The episode has also drawn attention to the unequal treatment of delays. While delayed refunds carry interest at 0.5% per month, taxpayers are charged interest at 1% per month for delays in advance or self-assessment tax payments.

In tax administration, compliance deadlines for taxpayers are rigid, while refund timelines for the department remain significantly more flexible.

Tax professionals point out that closure of a grievance often only confirms that the case falls within statutory timelines and does not imply any acceleration of refund issuance.

The episode has also drawn attention to the unequal treatment of delays. While delayed refunds carry interest at 0.5% per month, taxpayers are charged interest at 1% per month for delays in advance or self-assessment tax payments.

In tax administration, compliance deadlines for taxpayers are rigid, while refund timelines for the department remain significantly more flexible.

Tax professionals point out that closure of a grievance often only confirms that the case falls within statutory timelines and does not imply any acceleration of refund issuance.

The episode has also drawn attention to the unequal treatment of delays. While delayed refunds carry interest at 0.5% per month, taxpayers are charged interest at 1% per month for delays in advance or self-assessment tax payments.

In tax administration, compliance deadlines for taxpayers are rigid, while refund timelines for the department remain significantly more flexible.About Author

Meetu Kumari

Content Manager

Meetu Kumari is an Experienced Advocate and Content Writer with 4+ years of demonstrated history of working in the law practice industry. Skilled in Developing Content, Researching, and Drafting. Strong professional with a Bachelor of Science (B.Sc.) focused on Law from Gujarat National Law University.

Meetu Kumari is an Experienced Advocate and Content Writer with 4+ years of demonstrated history of working in the law practice industry. Skilled in Developing Content, Researching, and Drafting. Strong professional with a Bachelor of Science (B.Sc.) focused on Law from Gujarat National Law University.

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2264

2264My Recent Articles

- ITAT Condones 302-Day Delay, Restores Salary Assessment for Fresh VerificationPremium

- ITAT Condones Delay After Tax Consultant's Death, Restores Appeals for Fresh HearingPremium

- ITAT Remands Salary Addition, Says Taxability Depends on Salary Becoming Due, Not Mere ReceiptPremium

- ITAT Deletes TP Royalty Adjustment, Orders Fresh Review of Commission BenchmarkingPremium

- ITAT Quashes Reassessment Over Unsigned Section 148 Notice Issued to AssesseePremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts