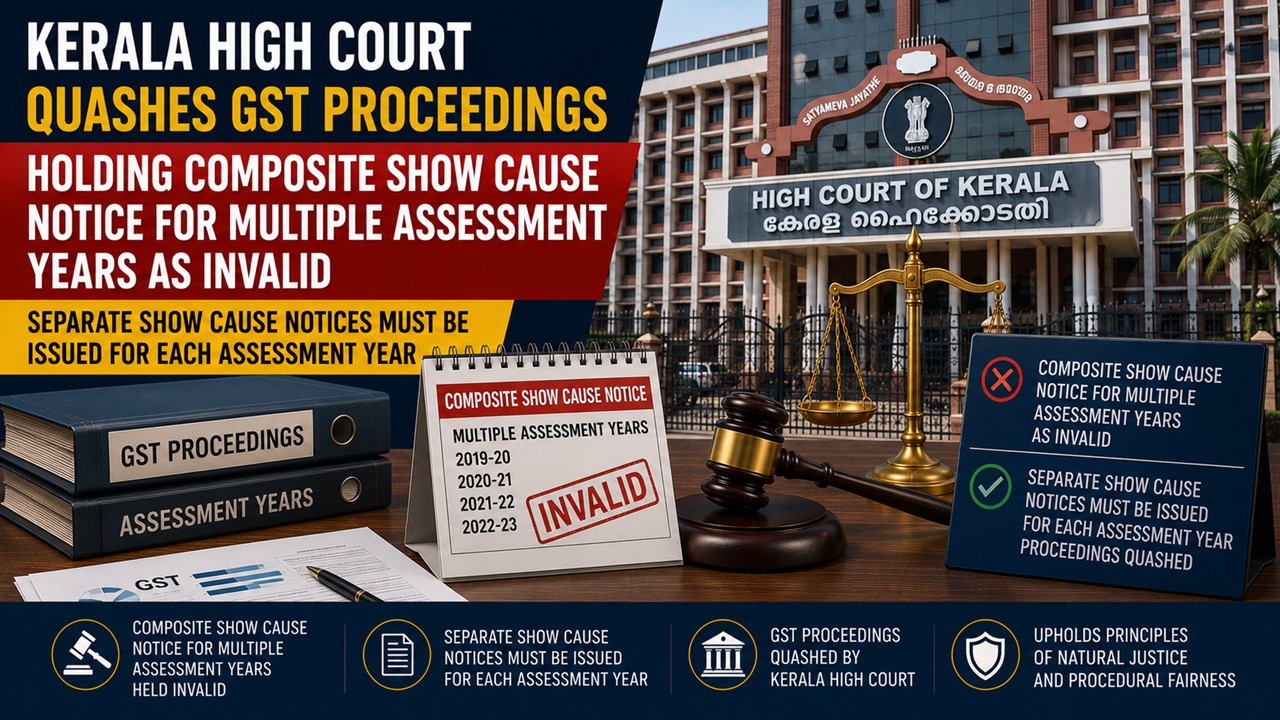

Kerala High Court Quashes GST Proceedings Holding Composite Show Cause Notice for Multiple Assessment Years As Invalid:

The Kerala High Court has set aside a composite Show Cause Notice holding that a common notice covering multiple assessment years is legally unsustainable.

Separate Show Cause Notices Must Be Issued for Each Assessment Year

Kerala High Court Quashes GST Proceedings Holding Composite Show Cause Notice for Multiple Assessment Years As Invalid

The Kerala High Court held that a composite Show Cause Notice issued under the GST laws for multiple assessment years is legally unsustainable and there should be separate proceedings initiated for each assessment year.

The petitioner is M/s. Malabar Trade Links and challenged a composite Show Cause Notice dated 22.09.2025 and the subsequent Order-in-Original dated 03.03.2026 issued by the GST authorities. The petitioner contended that issuance of a common notice for more than one assessment year was contrary to law.

The Petitioner relied on Kerala High Court decisions in Joint Commissioner (Intelligence & Enforcement) Vs. M/s. Lakshmi Mobiles Accessories and Tharayil Medicals (M/s.), Thrissur Vs. Deputy Commissioner, Thrissur to contend that issuance of a common notice for more than one assessment year was contrary to law.

The Court observed that a single Show Cause Notice covering multiple assessment years is not legally sustainable. In view of the principles observed by the court in the earlier judgments, the Court found merit in the challenge raised by the petitioner. Accordingly, the Court quashed both the Show Cause Notice and the Order-in-Original. However, liberty was granted to the respondent department to issue separate notices for the relevant assessment years and proceed in accordance with law.

The Court further directed that, while computing the period of limitation for initiating fresh proceedings, the period commencing from the date of issuance of the impugned Show Cause Notice until the receipt of the certified copy of the judgment shall stand excluded. All other contentions of the parties were left open.

About Author

Saima

Content Writer

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 219

219My Recent Articles

- ITAT Rules That Reassessment Proceedings Invalid Without Mandatory Notice under Section 143(2)Premium

- ITAT Rules that Section 153C Cannot Be Invoked Where the Date of Search for 'Other Person' Falls After 1 April 2021Premium

- ITAT Rules Reassessment Notices Where Escaped Income Ultimately Fell Below Rs 50 Lakh Threshold as UnsustainablePremium

- CBIC Constitutes Working Group to Examine Centralised Administration of Taxpayers with Multiple GST Registrations

- CBIC Issues Guidelines for Departmental Appeals to GSTAT in Common Adjudicating Authority Cases

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts