Late Payment to MSME: Decoding Section 43B(h) of Income Tax:

The Ministry of Finance has introduced the Section 43B(h) of Income Tax to ensure timely payment to MSMEs.

Decoding Section 43B(h) of Income Tax

Table of Contents

New Clause (h) of Section 43B

Certain deductions to be only on actual payment43B. Notwithstanding anything contained in any other provision of this Act, a deduction otherwise allowable under this Act in respect of….

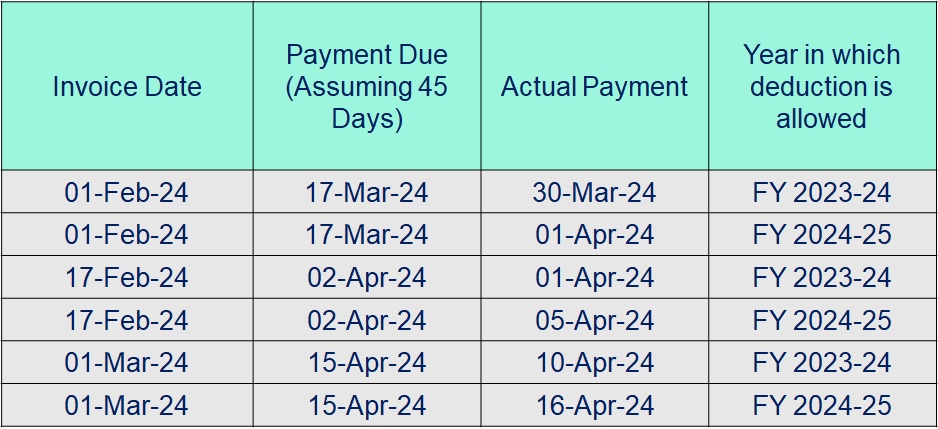

.. (h) any sum payable by the assessee to a micro or small enterprise beyond the time limit specified in section 15 of the Micro, Small and Medium Enterprises Development Act, 2006 (27 of 2006) [inserted by the Finance Act, 2023, w.e.f. 1-4-2024]

shall be allowed (irrespective of the previous year in which the liability to pay such sum was incurred by the assessee according to the method of accounting regularly employed by him) only in computing the income referred to in section 28 of that previous year in which such sum is actually paid by him:

Provided that nothing contained in this section [except the provisions of clause (h)] shall apply in relation to any sum which is actually paid by the assessee on or before the due date applicable in his case for furnishing the return of income under sub-section (1) of section 139 in respect of the previous year in which the liability to pay such sum was incurred as aforesaid and the evidence of such payment is furnished by the assessee along with such return.

Time limit specified in MSME Act

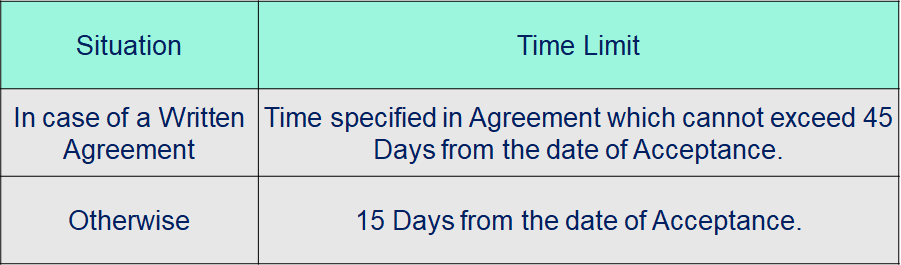

Liability of buyer to make payment15. Where any supplier, supplies any goods or renders any services to any buyer, the buyer shall make payment therefor on or before the date agreed upon between him and the supplier in writing or, where there is no agreement in this behalf, before the appointed day:

Provided that in no case the period agreed upon between the supplier and the buyer in writing shall exceed forty-five days from the day of acceptance or the day of deemed acceptance. Definitions.

2(b) "appointed day" means the day following immediately after the expiry of the period of fifteen days from the day of acceptance or the day of deemed acceptance of any goods or any services by a buyer from a supplier.

Explanation.—For the purposes of this clause,—

(i) "the day of acceptance" means,—

(a) the day of the actual delivery of goods or the rendering of services; or

(b) where any objection is made in writing by the buyer regarding the acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day on which such objection is removed by the supplier;

(ii) "the day of deemed acceptance" means, where no objection is made in writing by the buyer regarding acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day of the actual delivery of goods or the rendering of services;

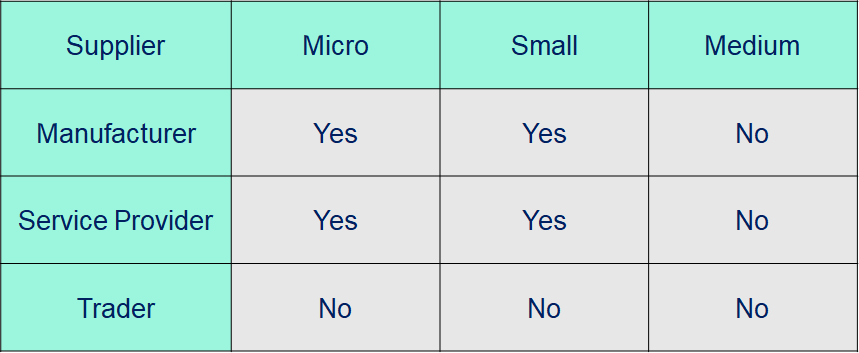

Condition for Applicability of Section 43B(h)

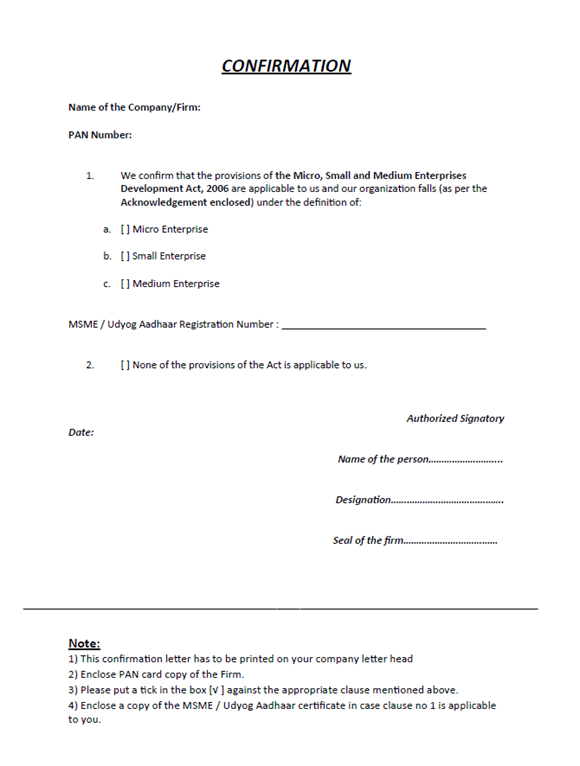

Note: Supplier should be registered on UIDAI Portal for claiming MSME Benefit.

Note: Supplier should be registered on UIDAI Portal for claiming MSME Benefit.

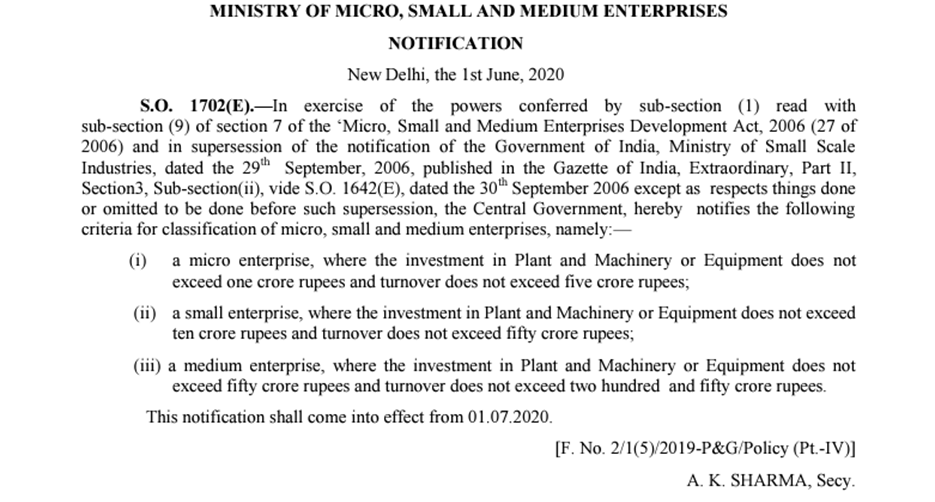

Definition of “Micro”, “Small” & “Medium” Enterprise

Consequences of Failure to Pay MSMEs within the Time Limit

- In case of Late Payment to MSME, Interest is applicable.

- Rate of Interest: Compound interest at 3 times of the bank rate notified by the Reserve Bank.

- Date from which interest is payable: Appointed day or the date as per the agreement as the case may be.

- Deduction of this interest is not allowed as an expense as per the Income Tax Act.

Payment to MSME: Expense allowed in year of payment if payment not made within Due Date

Take annual declarations and perform ageing for the selected list of suppliers on a regular basis.

Take annual declarations and perform ageing for the selected list of suppliers on a regular basis.

About Author

Reetu

Content Manager

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts