List of Goods Notified Under RCM for GST:

Here is a List of Goods Notified Under Reverse Charge Mechanism under GST RCM on supply of Goods Here is a List of Goods Notified Under Reverse Charge Mechanism under GST

RCM on supply of Goods

Table of Contents

Provision of RCM under GST

The reverse charge scenarios for intrastate transactions are governed by Sections 9(3), 9(4), and 9(5) of the Central GST and State/Union Territories GST Acts. Sections 5(3), 5(4), and 5(5) of the Integrated GST Act govern reverse charge scenarios for interstate transactions. The provisions of Section 9(4) of the CGST Act, 2017, will not be applicable to supplies made to a TDS deductor in terms of notification no.9/2017-Central Tax (Rate) dated 28.06.2017. Thus, government entities that are TDS deductors under Section 51 of the CGST Act, 2015, need not pay GST under reverse charge in cases of procurements from unregistered suppliers.RCM on Specified Goods

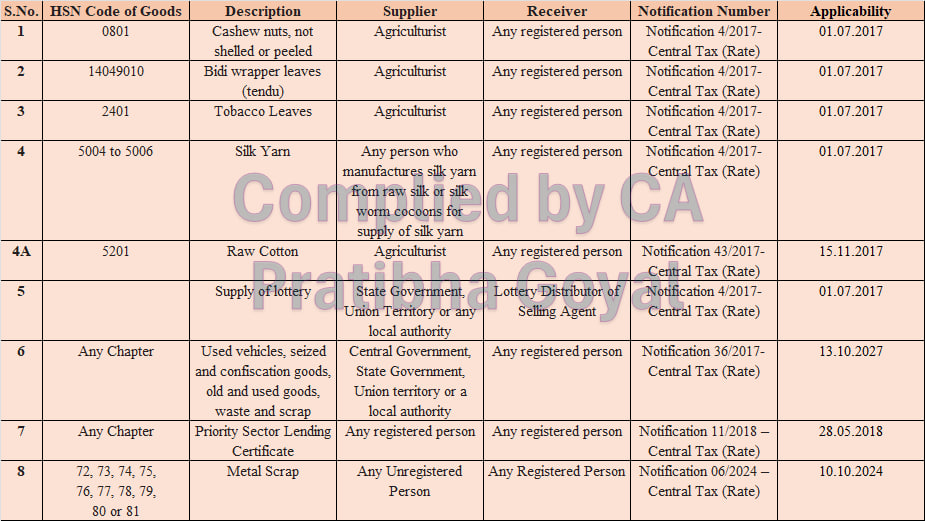

1. Cashew Nuts, not Shelled or Peeled The RCM levied on Cashew nuts, not shelled or peeled, when the supplier is an "agriculturist" and the receiver is "any registered person." This is notified by Master Notification 4/2017-Central Tax (Rate). 2. Bidi Wrapper Leaves (Tendu) The RCM levied on Bidi wrapper leaves (tendu), when the supplier is an "agriculturist" and the receiver is "any registered person." This is notified by Master Notification 4/2017-Central Tax (Rate). 3. Tobacco Leaves In the case of Tobacco Leaves, the RCM is levied when the supplier is an "agriculturist" and the receiver is "any registered person." This is notified by Master Notification 4/2017-Central Tax (Rate). 4. Silk Yarn In the case of Silk Yarn, the RCM is levied when the supplier is "any person who manufactures silk yarn from raw silk or silk worm cocoons for supply of silk yarn" and the receiver is "any registered person." This is notified by Master Notification 4/2017-Central Tax (Rate). 5. Raw Cotton The RCM is imposed on specified goods, like Raw Cotton, when the supplier is "agriculturist" and the receiver is "any registered person." This was added in Master Notification 4/2017-Central Tax (Rate) by Notification 43/2017-Central Tax (Rate) 6. Supply of Lottery In the case of Supply of Lottery, the RCM is levied when the supplier is "State Government, Union Territory or any local authority" and the receiver is "Lottery Distributor of Selling Agent". This is notified by Notification 4/2017-Central Tax (Rate). 7. Used vehicles, Seized and Confiscated Goods, Old and Used Goods, Waste and Scrap On the goods like Used vehicles, seized and confiscated goods, old and used goods, waste and scrap, RCM is levied when the supplier is "Central Government, State Government, Union territory or a local authority" and the receiver is "any registered person." This was added in Master Notification 4/2017-Central Tax (Rate) by Notification 36/2017-Central Tax (Rate). 8. Priority Sector Lending Certificate In the case of the Priority Sector Lending Certificate, the RCM is levied when the supplier is "any registered person" and the receiver is also "any registered person." This was added in Master Notification 4/2017-Central Tax (Rate) by Notification 11/2018 Central Tax (Rate). 9. Metal Scrap The RCM is imposed on specified goods, like Metal Scrap, when the supplier is "Any Unregistered Person" and the receiver is "any registered person." This was added in Master Notification 4/2017-Central Tax (Rate) by Notification 6/2024 Central Tax (Rate).

The same has been given in Tabular Form below for your reference:

| S.No. | HSN Code of Goods | Description | Supplier | Receiver | Notification Number | Applicability |

| 1 | 0801 | Cashew nuts, not shelled or peeled | Agriculturist | Any registered person | Notification 4/2017- Central Tax (Rate) | 01.07.2017 |

| 2 | 14049010 | Bidi wrapper leaves (tendu) | Agriculturist | Any registered person | Notification 4/2017- Central Tax (Rate) | 01.07.2017 |

| 3 | 2401 | Tobacco Leaves | Agriculturist | Any registered person | Notification 4/2017- Central Tax (Rate) | 01.07.2017 |

| 4 | 5004 to 5006 | Silk Yarn | Any person who manufactures silk yarn from raw silk or silk worm cocoons for supply of silk yarn | Any registered person | Notification 4/2017- Central Tax (Rate) | 01.07.2017 |

| 4A | 5201 | Raw Cotton | Agriculturist | Any registered person | Notification 43/2017-Central Tax (Rate) | 15.11.2017 |

| 5 | -NA- | Supply of lottery | State Government, Union Territory or any local authority | Lottery Distributor of Selling Agent | Notification 4/2017- Central Tax (Rate) | 01.07.2017 |

| 6 | Any Chapter | Used vehicles, seized and confiscation goods, old and used goods, waste and scrap | Central Government, State Government, Union territory or a local authority | Any registered person | Notification 36/2017-Central Tax (Rate) | 13.10.2027 |

| 7 | Any Chapter | Priority Sector Lending Certificate | Any registered person | Any registered person | Notification 11/2018 – Central Tax (Rate) | 28.05.2018 |

| 8 | 72, 73, 74, 75, 76, 77, 78, 79, 80 or 81 | Metal Scrap | Any Unregistered Person | Any Registered Person | Notification 06/2024 – Central Tax (Rate) | 10.10.2024 |

Reverse Charge Entries Under GST:

Entry for Purchase of Goods / Services Availed:

1.) If purchases/services are availed within the state (Intra State)Purchase / Expense A/c. ---------10,000

Input CGST A/c. ------------------- 900

Input SGST A/c. ------------------- 900

To Creditors A/c. or Cash/Bank Ac ------ 10,000

To CGST A/c Payable -----------------------900

To SGST A/c Payable -----------------------900

2.) If purchases / services are availed from other state (Inter State)Purchase / Expense A/c. ---------10,000

Input IGST A/c. -------------------- 1,800

To Creditors A/c. or Cash/Bank A/c. ------ 10,000

To IGST A/c Payable -----------------------1,800

3.) If purchases / services are availed from other Country (Import)Purchase / Expense A/c. ---------10,000

Input IGST A/c. -------------------- 1,800

To Creditors A/c. or Cash/Bank A/c. ------ 10,000

To IGST A/c Payable -----------------------1,800

About Author

Reetu

Content Manager

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.