Mapping of turnover from GSTR9 to GSTR9C | GST Annual Return

Mapping of turnover from GSTR9 to GSTR9C | GST Annual Return : In this article we have discussed theMapping of turnover from GSTR9 to GSTR9C

Table of Contents

Mapping of turnover from GSTR9 to GSTR9C | GST Annual Return :In this article we have discussed theMapping of turnover from GSTR9 to GSTR9C. We will discuss all the mapping one by one. But in this particular write up we will cover the turnover only.

Mapping of turnover from GSTR9 to GSTR9C | GST Annual Return

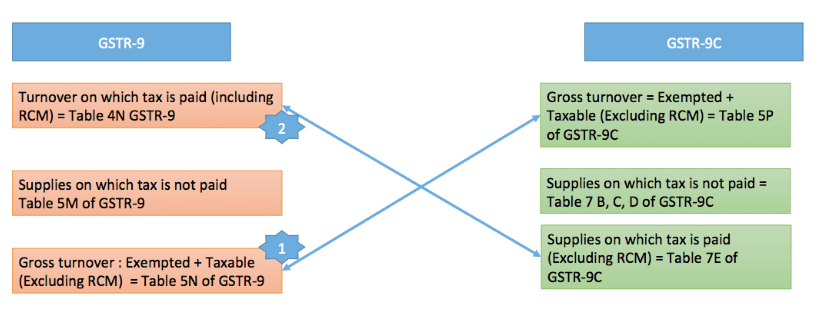

Flow of turnover data in GSTR9 | GST Annual Return In GSTR9 it start from the supplies on which tax has been paid. Then Inward supplies on which tax is paid in RCM is added in Table 4G. Next table is for supplies on which tax is not paid. It is covered in Table 5 of GST Annual return form GSTR9. Then 5N is calculated. 5N= 4N+5M-4G It is the value of outward supplies on which tax has been paid excluding RCM. Flow of data in GSTR9C In GSTR9C the flow of data is reverse. Table 5 start with turnover in financials. Then this data is drilled down to reach at the total turnover. Table 7 compiles all the outward supplies on which tax is not paid. After that the amount of supplies on which tax is paid is calculated in table 7E. Matching of turnover in GSTR9 & GSTR9C The data of 7E of GSTR9C is matched with 4N of GST Annual return

The data in table 5P of GSTR9C is matched with 5N+10+11 of GSTR9.

Let us have a look what they were.

7E= Supplies on which tax is paid (excluding RCM inward supplies)

4N= Supplies on which tax is paid (Including RCM inward supplies)

Eg.

Precision industries had following data in their GSTR9 & GSTR9C. Pls fill their table 8 of GSTR9C.

in GSTR9:

Table 4:

The data of 7E of GSTR9C is matched with 4N of GST Annual return

The data in table 5P of GSTR9C is matched with 5N+10+11 of GSTR9.

Let us have a look what they were.

7E= Supplies on which tax is paid (excluding RCM inward supplies)

4N= Supplies on which tax is paid (Including RCM inward supplies)

Eg.

Precision industries had following data in their GSTR9 & GSTR9C. Pls fill their table 8 of GSTR9C.

in GSTR9:

Table 4:

| A. |

Supplies made to un-registered persons (B2C) |

5,00,000 |

| B. |

Supplies made to registered persons (B2B) |

2,00,000 |

| C. |

Zero rated supply (Export) on payment of tax (except supplies to SEZs) |

|

| D. |

Supply to SEZs on payment of tax |

|

| E. |

Deemed Exports |

|

| F. |

Advances on which tax has been paid but invoice has not been issued (not covered under (A) to (E) above) |

25000 |

| G. |

Inward supplies on which tax is to be paid on reverse charge basis |

100000 |

| H. |

Sub-total (A to G above) |

825000 |

| I. |

Credit Notes issued in respect of transactions specified in (B) to (E) above (-) |

25000 |

| J. |

Debit notes issued in respect of transactions specified in (B) to (E) above (+) |

|

| K. |

Supplies / tax declared through Amendments (+) |

|

| L. |

Supplies / tax reduced through Amendments (-) |

|

| M. |

Sub-total (I to L above) |

|

| N. |

Supplies and advances on which tax is to be paid (H + M) above |

8,00,000 |

CA Shaifaly Girdharwal is a GST consultant, Author, Trainer and a famous You tuber. She has taken many seminars on various topics of GST. She is Partner at Ashu Dalmia & Associates and heading the Indirect Tax department.

About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.