Mergers & Acquisitions- Under Provisions of ITA,1961

Mergers & Acquisitions- Under Provisions of ITA,1961 Dear Friends, As you are aware that an organisation in long term on the basis of quality, st…

Table of Contents

Mergers & Acquisitions- Under Provisions of ITA,1961

Dear Friends,

As you are aware that an organisation in long term on the basis of quality, standard, services ,after sales services etc. recognized by the people. In recent time some organisations have become so big that their reserves are bigger than GDPs of some of small countries. A business entity always try to achieve more and more profit and markets. They are exploring new and emerging markets for their products and services in India as well as abroad. Liberalisation and Globalization have brought all world together and use of modern technologies we are able to trade all over the world. An entity acquires resources, technology, finance, markets , infrastructure ,etc. for its growth through various ways. An entity may enter into new market by Acquisition, acquisition, takeover or business restructuring. Acquisitions and acquisitions are manifestations of an inorganic growth process. While mergers can be defined to mean unification of two players into a single entity, acquisitions are situations where one player buys out the other to combine the bought entity with itself. It may be in form of a purchase, where one business buys another or a management buyout, where the management buys the business from its owners. Further, de-mergers, i.e., the division of a single entity into two or more entities also require being recognized and treated on par with mergers and acquisitions regime.

Mergers and acquisitions are used as instruments of momentous growth and are increasingly getting accepted by Indian businesses as critical tool of business strategy. They are widely used in a wide array of fields such as information technology, telecommunications, and business process outsourcing as well as in traditional business to gain strength, expand the customer base, cut competition or enter into a new market or product segment. Mergers and acquisitions may be undertaken to access the market through an established brand, to get a market share, to eliminate competition, to reduce tax liabilities or to acquire competence or to set off accumulated losses of one entity against the profits of other entity.

Mergers and acquisitions (M&A) in India are near an all-time high, led by more first-time buyers than ever before, accounting for more than 80 per cent of the deals closed in 2020 and 2021—a marked increase from less than 70 per cent through 2017 to 2019.[ This is according to Bain & Company's new report - India M&A: Acquiring to Transform.]

There were 85 strategic deals valued at more than $75 million in 2021, out of which the percentage of first-time buyers is almost 80 per cent. There were 80 strategic deals valued at more than $75 million in 2020, out of which the percentage of first-time buyers, is 80 per cent. For the years 2020 and 2021, the percentage of first-time buyers is highest compared to the percentage for the years 2017 till 2019.

The nature of deals is more broad-based, including more mid-sized deals ranging from $500 million- $1 billion, compared to the mega $5 billion deals that drove activity in 2017-19. This greater deal momentum has been driven by an accelerated disruption across sectors, and companies are using M&A to transform their businesses for a post-Covid world. Cash reserves and foreign direct investment inflows at their highest-ever levels, availability of private equity (PE) dry powder is resilient, and interest rates are at a low. Armed with this capital, one of the ways companies are responding to disruption and growth expectations is through acquisitions.

THE CONCEPT OF MERGER & AMALGAMANTION UNDER INCOME TAX ACT, 1961

Amalgamation is a blending of two or more existing companies /undertakings into one company/ undertaking. The shareholders of two blending companies substantially become shareholders of the blended company. There will be an Amalgamation ,when two or more companies/undertakings are acquired by a new company.

WHY COMPANIES AMALGAMATE OR MERGED

TYPES OF MERGERS

THE DIFFERENT TYPES OF MERGERS IN INDIA ARE AS FOLLOWS:

1.HORIZONTAL MERGER: A Horizontal Merger takes place between the companies dealing with similar products. The purpose of merger is to reduce competition, acquire a dominant market position, and expand the market reach. For example, Mergers of Brooke Bond and Lipton India; Hindustan Unilever and Patanjali.

2. VERTICAL MERGER -The main aim of a vertical merger is to combine two companies which deal in the same types of products. However, the stages of production at which they are operating are different. For example, Reliance Industries and FLAG Telecom group.

3. CO-CENTRIC MERGERS - The term Co-centric Merger denotes that the organisations serve the same type of customers. In this case, the products and services of both companies complement each other even if they are entirely different. For example, Axis Bank acquiring Freecharge; Citi Group acquiring Salomon Smith Barney; Flipkart acquiring Walmart India.

4. CONGLOMERATE MERGERS - When two or more unrelated industries/ companies merge with each other, it is termed as Conglomerate Mergers. The aims and objectives of both companies are completely different from each other. However, the main purpose of this type of merger is to boost business in terms of operations, profits and size. For example, Voltas Ltd and L&T.

5.CASH MERGERS- When the shareholders are offered cash in place of the shares of the newly formed company, it is known as Cash Mergers.

6.FORWARD MERGERS- When a company chooses to merge with its customers, it is known as Forward Merger. For example, ICICI Bank acquired Bank of Mathura.

7. REVERSE MERGERS - In Reverse Mergers, a company decides to merge with its suppliers. For example, Gujarat Godrej Innovative Chemicals acquired Godrej soap.

TYPES OF AMALGAMATIONS

The two main types of amalgamation are amalgamation in the nature of a merger and amalgamation in the nature of a purchase. To understand both these types in detail let us go through them one by one.

TYPES OF MERGERS

THE DIFFERENT TYPES OF MERGERS IN INDIA ARE AS FOLLOWS:

1.HORIZONTAL MERGER: A Horizontal Merger takes place between the companies dealing with similar products. The purpose of merger is to reduce competition, acquire a dominant market position, and expand the market reach. For example, Mergers of Brooke Bond and Lipton India; Hindustan Unilever and Patanjali.

2. VERTICAL MERGER -The main aim of a vertical merger is to combine two companies which deal in the same types of products. However, the stages of production at which they are operating are different. For example, Reliance Industries and FLAG Telecom group.

3. CO-CENTRIC MERGERS - The term Co-centric Merger denotes that the organisations serve the same type of customers. In this case, the products and services of both companies complement each other even if they are entirely different. For example, Axis Bank acquiring Freecharge; Citi Group acquiring Salomon Smith Barney; Flipkart acquiring Walmart India.

4. CONGLOMERATE MERGERS - When two or more unrelated industries/ companies merge with each other, it is termed as Conglomerate Mergers. The aims and objectives of both companies are completely different from each other. However, the main purpose of this type of merger is to boost business in terms of operations, profits and size. For example, Voltas Ltd and L&T.

5.CASH MERGERS- When the shareholders are offered cash in place of the shares of the newly formed company, it is known as Cash Mergers.

6.FORWARD MERGERS- When a company chooses to merge with its customers, it is known as Forward Merger. For example, ICICI Bank acquired Bank of Mathura.

7. REVERSE MERGERS - In Reverse Mergers, a company decides to merge with its suppliers. For example, Gujarat Godrej Innovative Chemicals acquired Godrej soap.

TYPES OF AMALGAMATIONS

The two main types of amalgamation are amalgamation in the nature of a merger and amalgamation in the nature of a purchase. To understand both these types in detail let us go through them one by one.

GOVERNING LAWS FOR MERGER AND AMALGAMATION

UNDER INCOME TAX ACT, 1961 SECTION 2(1B) OF INCOME TAX ACT defines ‘Amalgamation’ as merger of one or more companies with another company or merger of two or more companies to form one company in such a manner that:-- All the property of the amalgamating company or companies immediately before the amalgamation becomes the property of the amalgamated company by virtue of the amalgamation.

- All the liabilities of the amalgamating company or companies immediately before the amalgamation becomes the liabilities of the amalgamated company by virtue of the amalgamation.

- Shareholders holding at least three-fourths in value of the shares in the amalgamating company or companies (other than shares already held therein immediately before the amalgamated company or its nominee) becomes the shareholders of the amalgamated company by virtue of the amalgamation.

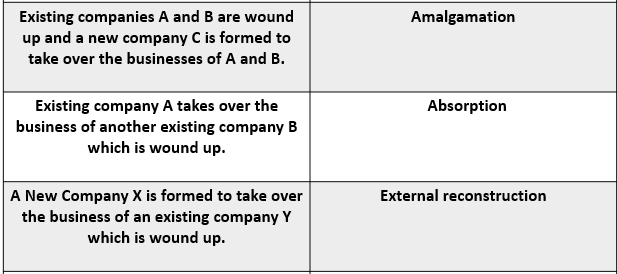

- Amalgamation is the combination of two or more companies into a brand-new entity by combining the assets and liabilities of both entities into one.

- This differs from a traditional merger in that neither of the two companies involved survives as an entity.

- The transferor company is absorbed into the stronger, transferee company, leading to an entity with a stronger customer base and more assets.

- Amalgamation can help increase cash resources, eliminate competition, and save companies on taxes.

- But it can lead to a monopoly if too much competition is cut out, scale down the workforce, and increase the new entity's debt load.

TYPES OF MERGERS

THE DIFFERENT TYPES OF MERGERS IN INDIA ARE AS FOLLOWS:

1.HORIZONTAL MERGER: A Horizontal Merger takes place between the companies dealing with similar products. The purpose of merger is to reduce competition, acquire a dominant market position, and expand the market reach. For example, Mergers of Brooke Bond and Lipton India; Hindustan Unilever and Patanjali.

2. VERTICAL MERGER -The main aim of a vertical merger is to combine two companies which deal in the same types of products. However, the stages of production at which they are operating are different. For example, Reliance Industries and FLAG Telecom group.

3. CO-CENTRIC MERGERS - The term Co-centric Merger denotes that the organisations serve the same type of customers. In this case, the products and services of both companies complement each other even if they are entirely different. For example, Axis Bank acquiring Freecharge; Citi Group acquiring Salomon Smith Barney; Flipkart acquiring Walmart India.

4. CONGLOMERATE MERGERS - When two or more unrelated industries/ companies merge with each other, it is termed as Conglomerate Mergers. The aims and objectives of both companies are completely different from each other. However, the main purpose of this type of merger is to boost business in terms of operations, profits and size. For example, Voltas Ltd and L&T.

5.CASH MERGERS- When the shareholders are offered cash in place of the shares of the newly formed company, it is known as Cash Mergers.

6.FORWARD MERGERS- When a company chooses to merge with its customers, it is known as Forward Merger. For example, ICICI Bank acquired Bank of Mathura.

7. REVERSE MERGERS - In Reverse Mergers, a company decides to merge with its suppliers. For example, Gujarat Godrej Innovative Chemicals acquired Godrej soap.

TYPES OF AMALGAMATIONS

The two main types of amalgamation are amalgamation in the nature of a merger and amalgamation in the nature of a purchase. To understand both these types in detail let us go through them one by one.

- AMALGAMATION IN THE NATURE OF A MERGER- As the name suggests, this is the type of amalgamation which works as a merger. In this, the transferee or the stronger company absorbs the transferor or the weaker company and the two entities pool their shareholders’ interest, as well as the assets and liabilities. Businesses of both the companies continue to rununder the newly formed entity and if the shareholders of the transferor meet the minimum requirements, then they can become shareholders in the new company as well.When both the Transferor and Transferee Company decide to combine their shareholders’ interest along with their assets and liabilities, it is known as Amalgamation in the nature of Merger. In this kind of amalgamation, alterations are made to the book values of the assets and liabilities. Moreover, the shareholders of the Transferor Company become the shareholders of the Transferee Company with at least 90% shareholding.

- the manufacture or processing of goods, or

- the manufacture of computer software, or

- the business of generation or distribution of electricity or any other form of power, or mining, or

- the construction of ships, aircrafts or rail systems, or

- the business of providing telecommunication services, whether basic or cellular, including radio paging, domestic satellite service, network of trunking, broadband network and internet services.

- Specified bank means the State Bank of India constituted under the State Bank of India Act, 1955 or

- a subsidiary bank as defined in the State Bank of India (Subsidiary Bank) Act, 1959 or

- a corresponding new bank constituted under section 3 of the Banking Companies (Acquisition and Transfer of Undertaking) Act, 1980.

- Unabsorbed Depreciation includes -Unabsorbed Capital Expenditure on Scientific Research/ Family Planning.

- Production is not important to eligible for Section 72A ,since Section 72A (2)(i) clearly uses the word “ engaged in business”.

- The Appointed Day or Date of amalgamation given in the scheme of amalgamation ( as approved by High Court) is taken as the date of amalgamation for the purpose of Sectionn72A.

- Substantial would mean the foreign shares/interest would need to derive at least 50% of their value from Indian Assets. In case of amalgamation of a foreign company having shares of Indian company with other foreign company.[ Finance Bill 2015].

- The term “ Undertaking” would include any part of an undertaking , any unit or division of an undertaking or a business activity as whole , but does not include individual assets or liabilities which do not constitute a business activity. The term “ liabilities” would include liabilities and specific loans/borrowings incurred or raised for the specific business activity of the undertaking. In case of a multipurpose loan , such value of the loan will be included , that bears the same proportion as the value of the demerged assets of the total assets of the company.

About Author

FCS DEEPAK P. SINGH

Manager Legal & Compliance

SBI GENERAL INSURANCE COMPANY LIMITED

SBI GENERAL INSURANCE COMPANY LIMITED Mumbai, Maharashtra, India

Mumbai, Maharashtra, India 53

53My Recent Articles

- Surveyor Cannot Apply Deductions Arbitrarily On Amount Of Assessed Loss: Supreme Court Of India

- Insurance Company Cannot Impose Condition That Will Impossible To Comply By Insured

- The Disputes between Landlord & Tenant Governed by Transfer of Property Act 1882 are Arbitrable in Nature

- Damage Caused by the Insurers Taking Possession of Insured Premises & Judicial Opinions

- Disputes Between Landlord & Tenant Governed by Transfer of Property Act, 1882 Arbitrable: HC

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts