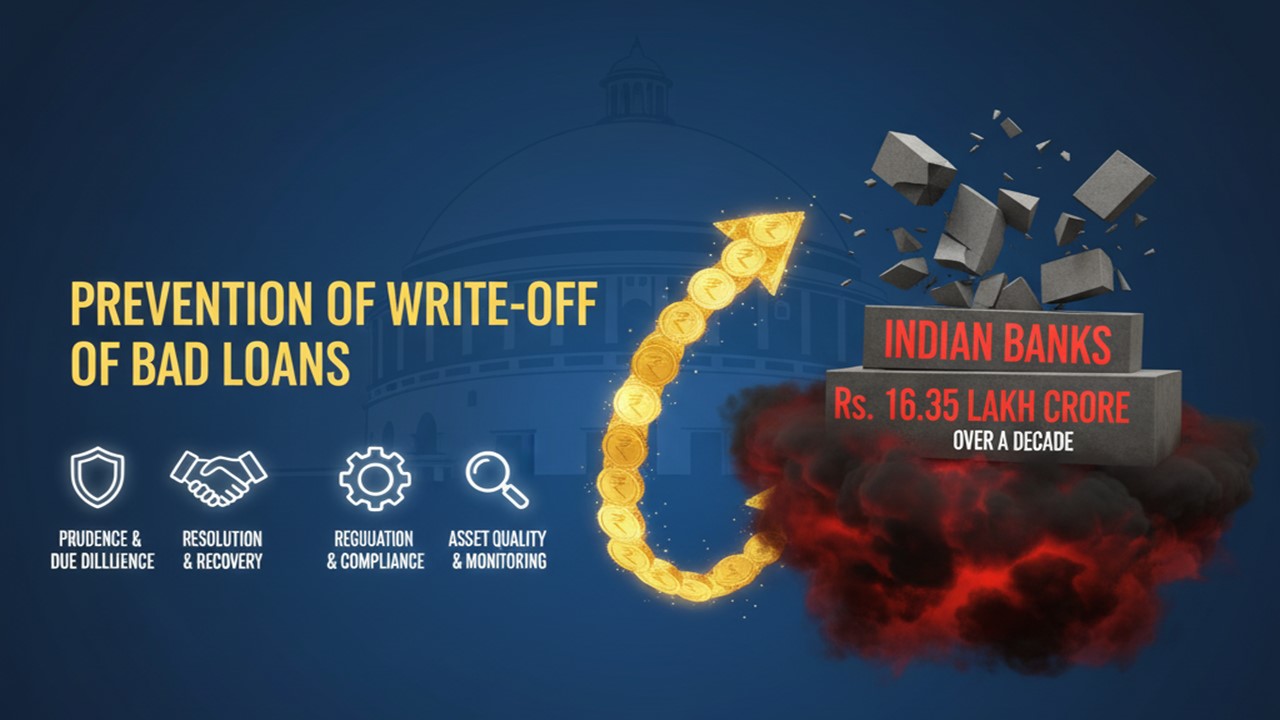

Prevention Of Write Off Of Bad Loans Indian Banks Wrote Off Rs. 16.35 Lakh Crore In Bad Loans Over a Decade:

The Reserve Bank of India (RBI) clarified that these write-offs are in line with regulatory norms, requiring banks to fully provision NPAs.

Rs.16.35 Lakh Crore Bad Loans Written Off in 10 Years

Prevention Of Write Off Of Bad Loans Indian Banks Wrote Off Rs. 16.35 Lakh Crore In Bad Loans Over a Decade

T. R. Radhakrishnan,

Banking & Management Consultant,

NPA Resolution Consultant,

H. R. Trainer: Corporates, Colleges & Schools, & Freelance Writer,

No. 8, Morya Gardens,

Kanadia Road,

Indoe.452016 (Madhya Pradesh)

Mobile: (0)9229248048

E-mail: [email protected]

PREVENTION OF WRITE OFF OF BAD LOANS

Indian banks wrote off Rs. 16.35 lakh crore in bad loans over a decade

The Government of India, Finance Ministry recently presented in Parliament the data regarding the staggering Rs. 16.35 lakh crore written off bad loans over the last 10 financial years. “The Reserve Bank of India (RBI) clarified that these write-offs are in line with regulatory norms, requiring banks to fully provision NPAs.” Further it is explained that “the move is aimed at strengthening financial stability while ensuring recoveries remain a priority”.

As per RBI source

Clarifications by RBI and Finance Ministry.

RBI clarifies that the aforesaid action of writing off the bad loans are coming under regulatory norms which will enable the banks to clean up their balance sheets after fully providing for NPAs, but will not absolve the defaulters and the recovery of defaulted amounts will continue unabated and their recovery will be the key focus. Finance Minister clarified, “Such write-offs do not result in waiver of liabilities of borrowers and therefore, it does not benefit the borrower,”. However, the recovery efforts should continue through legal means by approaching DRTs, DRATs and initiating legal proceeding through courts by invoking loan recovery laws or any other law for the time being in force and not being in derogation any such law. Yet another way of recovery of the defaulted liability is by way of One Time Settlement (OTS).

Points to ponder over

The RBI Annual Report for FY 2024–25, released on May 30, 2025, revealed that the RBI imposed 353 penalties totalling Rs.54.78 crore. These were related to non-compliance with several critical frameworks and regulatory mandates across different banking and financial sectors.

RBI has clarified that “Banks need to ensure compliance to all applicable statutory provisions, rules and regulations, various codes of conducts (including the voluntary ones) and their own internal rules, policies and procedures. It is, however, reiterated that compliance is a shared responsibility of the business units and the compliance function. Therefore, adherence to applicable statutory provisions and regulations needs to be the responsibility of each staff member of the bank and it is the work of the compliance function to ensure the same.” RBI further states, “In some banks, there may be separate departments looking after compliance to different statutory and other requirements while the compliance function may be responsible for monitoring compliance with the regulations, internal policies and procedures and reporting to Management. The concerned departments would hold the prime responsibility for their respective areas, which should be clearly outlined, while compliance function would need to ensure overall oversight. If serious gaps are observed in such compliances, the compliance function should take necessary action to correct the compliance culture. There should also be appropriate mechanisms for co-operation among departments and with the Chief Compliance Officer.”

The OBJECTIVE OF SUPERVISION as stated in the RBI report is ensuring “Along with protection of depositors’ interests and ensuring financial health of individual banks / FIs, an implicit overarching objective of RBI’s supervisory process should also be to ensure financial stability and customer protection.”

RBI observations on compliance function and audit

The most important observation made by RBI is, “The compliance function in banks however, has not received the required attention by banks, as a number of instances of non-compliance and lack of proper interpretation of regulatory guidelines are being reported in successive RBI inspection reports. Further, in the absence of a comprehensive compliance structure, policy and manual for addressing compliance risk in most of the banks, compliance processes remain weak and the role of the Compliance Officer has not been an effective instrument for which it was created.” Such wanton violations by banks and regulated entities are found out only when inspections and audits are undertaken at random or on account of specific reasons and not on a regular and continuous basis because of which many such incidents are swept under the carpet. Concurrent audit has been introduced in banks which “aims at shortening the interval between a transaction and its independent examination. It is, therefore, integral to the establishment of sound internal accounting functions and effective controls and is regarded as part of a bank’s early warning system to ensure timely detection of serious errors and irregularities, which also helps in averting fraudulent transactions and preventive vigilance in banks.” It is also observed that the auditors were negligent or deficient which sometimes include falsification of accounts in conducting the audit to enable the ICAI to examine and fix accountability of the auditors.

Borrowers’ role in the creation of NPA

Apart from the wrong doings and unbecoming acts of regulated entities and auditors, the borrowers also are responsible for the creation of NPAs. Lack of financial discipline and good governance and non-compliance of statutory provisions and banking norms more particularly diversion of funds in conducting the account contribute to the slippage of accounts as NPA. Besides, lack of understanding and absence of effective communication between the lender and borrower also facilitate accounts becoming non-recoverable NPAs. It may be noted that the borrowers should not come under the category of a wilful defaulters or fraudsters.

Applicable remedies.

Banks’ and other Regulated Entities’ responsibilities and accountabilities.

| Financial Year | Total NPAs written-off in Rs. Crores. | NPAs written-off ‘for large industries and services In Rs. Crores. |

| 2014-2015 | 58,786 | 31,723 |

| 2015-2016 | 70,413 | 40,416 |

| 2016-2017 | 1,08,373 | 68,308 |

| 2017-2018 | 1,61,328 | 99,132 |

| 2018-2019 | 2,36,265 | 1,48,753 |

| 2019-2020 | 2,34,170 | 1,59,139 |

| 2020-2021 | 2,04,272 | 1,27,050 |

| 2021-2022 | 1,75,178 | 69,532 |

| 2022-2013 | 2,16,324 | 1,14,528 |

| 2023-2024 | 1,70,270 | 68,366 |

| Total | 16,35,379 | 9,26,947 |

- “The move is aimed at strengthening financial stability while ensuring recoveries remain a priority”. How can financial stability be achieved against massive write offs and that too when recoveries remain the priority? Are not financial stability and recovery of loans complementary to each other?

- Writing off the bad loans coming under regulatory norms will enable the banks to clean up their balance sheets. Can writing off bad loans without realisation of the defaulted amount be construed as an act of window dressing by bank as per banking terms?

- Even if the bank legally proceeds to recover the outstanding loan liability under the written off loans, the point raised is whether the realised amount through the legal proceedings would cover the written off liability along with interest till date of realisation? Practically speaking, the bank may have to undergo a haircut between 30% to 70% of the total realisable amount of the written off loan liability. If so, who is the beneficiary, the bank or the borrower?

- Finance Minister clarified, “Such write-offs do not result in waiver of liabilities of borrowers and therefore, it does not benefit the borrower.” Considering the aforesaid facts neither the bank balance sheet is cleaned up nor the borrower is a loser. On the contrary, the borrower becomes the beneficiary to the extent of the hair cut under went by the lender.

- One Time Settlement (OTS) of the outstanding liability under the loan account with the mutually negotiated and agreed settlement between the lender and borrower is an option for the recovery of the outstanding overdue of the written off loans and also other stressed loans. RBI recognises compromise settlements as a valid resolution plan. Compromise proposals also involve sacrifice by the banks. In this connection what former RBI Governor Raghuram Rajan said on NPA recovery is worth recalling. “We have to improve the efficiency of the recovery system, especially at a time of economic uncertainty like the present. Recovery should be focused on efficiency and fairness – presenting the value of underlying assets and jobs where possible, even while redeploying unviable assets to new uses and compensating fairly. All this should be done while ensuring that contractual priorities are met. The system has to be tolerant of genuine difficulties while coming down on mismanagement or fraud,” Is the advisory of former RBI Governor being followed?

| Period | No of regulated entities | Penalty Amount imposed Rs. in Crores. |

| December 2021 to May 2022 | 74 | 9.98 |

| June 2022 to November 2022 | 105 | 24.57 |

| December 2022 to May 2023 | 122 | 26.34 |

| June 2023 to November 2023 | 146 | 57.07 |

| December 2023 to May 2024 | 161 | 22.83 |

| Total | 608 | 140.79 |

- Strict enforcement of compliance functions as per RBI guidelines which includes prevention of accounts slipping in to NPA even before classification as NPA particularly accounts coming under the category of MSME. Implementation of the provisions of MSME Act is also to be ensured.

- ‘Due Diligence’ audit should be undertaken as and when required as per RBI guidelines.

- Diligent appraisal, assessment, and timely sanction and release of appropriate and adequate credit needs of the borrower as per RBI directions. The banks and financial institutions should ensure the borrower entity to maintain adequate cash flow to meet their financial commitments.

- Effective and efficient credit monitoring and periodical effective evaluation of performance result and taking immediate remedial steps in case of adverse features found in consultation with and the participation of the borrower.

- Timely action to redress the grievances of the borrower, if any, with regard to credit needs or any other banking services. Customer rights are to be protected as per Charter of Customer Rights.

- Effective and consistent communication with the borrowers regarding the loan accounts and undertaking periodical credit counselling meetings with the borrowers duly minuted and singed by all participants and to be followed up and completed till the objectives of the minutes of the counselling meetings are achieved.

- Strict compliance of terms and conditions of sanction.

- Proper and timely execution of all loan agreements and papers.

- Submission of periodical controlling statements as per bank’s requirements.

- Timely servicing of interest and payment loan instalments.

- Effective communication and transparent business dealings.

- Not to indulge in diversion of funds.

- Payment of all statutory dues on time.

- Effective working capital management for achieving envisaged results.

- Practicing good governance.

- Operating any business in today’s economic environment means managing cash flow. Companies looking only at their earnings and not managing cash flow cannot and will not survive in today’s economy where short-term operational loans are not often readily available. Hence, managing a very positive cash flow is an essential and an inevitable necessity for any business organisation.

- Undertaking any action that may be required by the bank / financial institutions, auditors or any stake holders at any point of time as and when any adverse features are detected in the conduct of the account.

- Borrower should be made to understand that there is no remedy available for those borrowers who are proved to be wilful defaulters and fraudsters.

About Author

trradhakrishnan

Chief Consultant, Banking, Management and NPA Resolution.

freelancer

freelancer Indore, Madhya Pradesh, India

Indore, Madhya Pradesh, India 7

7Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts