Recommendations made during the 25th meeting of the GST Council

Recommendations made during the 25th meeting of the GST Council Here is theextract of some of the recommendations made by the GST Council du

Table of Contents

Recommendations made during the 25th meeting of the GST Council

Here is theextract of some of the recommendations made by the GST Council during its 25th meeting held in New Delhi on 18th January:

For complete list of recommendations please refer the press release attached herewith.

A. Policy Changes

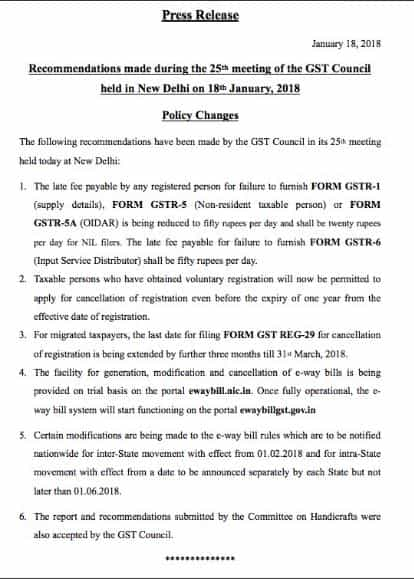

The following recommendations have been made by the GST Council in its 25th meeting held today at New Delhi:

1. The late fee payable by any registered person for failure to furnish FORM GSTR-1 (supply details), FORM GSTR-5 (Non-resident taxable person) or FORM GSTR- 5A (OIDAR) is being reduced to fifty rupees per day and shall be twenty rupees per day for NIL filers. The late fee payable for failure to furnish FORM GSTR-6 (Input Service Distributor) shall be fifty rupees per day.

2. Taxable persons who have obtained voluntary registration will now be permitted to apply for cancellation of registration even before the expiry of one year from the effective date of registration.

3. For migrated taxpayers, the last date for filing FORM GST REG-29 for cancellation of registration is being extended by further three months till 31st March, 2018.

4. The facility for generation, modification and cancellation of e-way bills is being provided on trial basis on the portal ewaybill.nic.in. Once fully operational, the eway bill system will start functioning on the portal ewaybillgst.gov.in (Also seeE-Way Bill Registration)

5. Certain modifications are being made to the e-way bill rules which are to be notified nationwide for inter-State movement with effect from 01.02.2018 and for intra-State movement with effect from a date to be announced separately by each State but not later than 01.06.2018.

6. The report and recommendations submitted by the Committee on Handicrafts were also accepted by the GST Council.

Click here to download the Press Release

B. Recommendations for changes in GST/IGST Rate & Clarifications in respect of GST Rate of Certain goods

LIST OF GOODS ON WHICH GST RATE RECOMMENDED FOR REDUCTION FROM 28% TO 18%:

1.) Old and used motor vehicles [medium and large cars and SUVs] on the margin of the supplier, subject to the condition that no input tax credit of central excise duty/value added tax or GST paid on such vehicles has been availed by him

2.) Buses, for use in public transport, which exclusively run on bio-fuels.

LIST OF GOODS ON WHICH GST RATE RECOMMENDED FOR REDUCTION FROM 28% TO 12%:

All types of old and used motors vehicles [other than medium and large cars and SUVs] on the margin of the supplier of subject to the conditions that no input tax credit of central excise duty /value added tax or GST paid on such vehicles has been availed by him.

LIST OF GOODS ON WHICH GST RATE RECOMMENDED FOR REDUCTION FROM 18% TO 12%:

You May also refer E WAY BILL A BIG BOOST FOR EASE OF DOING BUSINESS All About Electronic Way Bill in GST

TAGS: 25th gst council meeting press release, cbec press release, gstcbec press release, gst council press release,Recommendations made during the 25th meeting of the GST Council ,Recommendations made during the 25th meeting of the GST Council,gst council press release today, press note gst

- Sugar boiled confectionary

- Drinking water packed in 20 litters bottles

- Fertilizer grade Phosphoric acid

- Bio-diesel

- Notified Bio-pesticides

- Drip irrigation system including laterals, sprinklers

- Bamboo Wood building joinery

OTHER RECOMMENDATIONS

On LPG supplied for supply to household domestic consumers by private LPG distributors GST rate has been recommended for reduction from 18% to 5%. On Cigarette filter rods GST rate has been recommended for increase from 12% to 18% OnDiamonds and precious stoneshas been recommended for reduction from 3% to 0.25%. Cess on Old & used motor cars has been abolished. For detailed list of recommendations please refer the press release: Click here to download the Press Release C. Decisions relating to Services Some of the important recommendations are as follows:- To exempt supply of services by way of providing information under RTI Act, 2005 from GST.

- To exempt legal services provided to Government, Local Authority, Governmental Authority and Government Entity.

- To reduce GST rate on construction of metro and monorail projects (construction, erection, commissioning or installation of original works) from 18% to 12%.

- To levy GST on the small housekeeping service providers, notified under section 9 (5) of GST Act, who provide housekeeping service through ECO, @ 5% without ITC.

- To reduce GST rate on tailoring service from 18% to 5%.

- To reduce GST rate on services by way of admission to theme parks, water parks, joy rides, merry-go-rounds, go-carting and ballet, from 28% to 18%.

- To allow ITC of input services in the same line of business at the GST rate of 5% in case of tour operator service.

- To reduce GST rate (from 18% to 12%) on the Works Contract Services (WCS) provided by sub-contractor to the main contractor providing WCS to Central Government, State Government, Union territory, a local authority, a Governmental Authority or a Government Entity, which attract GST of 12%. Likewise, WCS attracting 5% GST, their sub-contractor would also be liable @ 5%.

- To reduce GST rate on transportation of petroleum crude and petroleum products (MS, HSD, ATF) from 18% to 5% without ITC and 12% with ITC

- To exempt (a) services by government or local authority to governmental authority or government entity, by way of lease of land, and (b) supply of land or undivided share of land by way of lease or sub lease where such supply is a part of specified composite supply of construction of flats etc. and to carry out suitable amendment in the provision relating to valuation of construction service involving transfer of land or undivided share of land, so as to ensure that buyers pay the same effective rate of GST on property built on leasehold and freehold land.

- To amend entry 3 of notification No. 12/2017-CT(R) so as to exempt pure services provided to Govt. entity.

- To expand pure services exemption under S. No. 3 of 12/2017-C.T. (Rate) so as to include composite supply involving predominantly supply of services i.e. upto 25% of supply of goods.

- To exempt services relating to admission to, or conduct of examinationprovided to all educational institutions, as defined in the notification. To exempt services by educational institution by way of conduct of entrance examination against consideration in the form of entrance fee

- To exempt governments share of profit petroleum from GST and to clarify that cost petroleum is not taxable.

You May also refer E WAY BILL A BIG BOOST FOR EASE OF DOING BUSINESS All About Electronic Way Bill in GST

TAGS: 25th gst council meeting press release, cbec press release, gstcbec press release, gst council press release,Recommendations made during the 25th meeting of the GST Council ,Recommendations made during the 25th meeting of the GST Council,gst council press release today, press note gst

About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.