Replacement of the machineries cannot be held as repairs or allowable revenue expenditure

Replacement of the machineries cannot be held as repairs or allowable revenue expenditure Relevant Extract of Order is given below: The Reve

"9.I.T.A.Nos.1334 & 1335/Mds/99: These two appeals are filed by the Revenue against the order of the CIT (Appeals) and relate to the assessment years 1993-94 and 1994-95. The solitary issue raised in these appeals relates to the question as to whether cost of replacement of machinery could be claimed as revenue expenditure. The replaced machineries are an assemble of Motor Rollers, Spindles, gears etc. The Assessing Officer observed that the machineries under consideration are indigenous products made in India and are nothing but modernized system of automatic controllers installed to replace manual labour. He, therefore, disallowed the claim of the assessee. The CIT (Appeals), however, allowed the claim of the assessee. We find that the jurisdictional High Court in the case of CIT v. Salem Co-operative Spinning Mills Ltd. (148 ITR 176) (Mad) has held that expenditure on replacement of conventional card clothing by metallie card clothing is revenue expenditure and as such exigible to deduction under Section 37. We do not find any infirmity in the order of the CIT (Appeals). Accordingly, the order of the CIT (Appals) is upheld.

10.In the result, the Revenue's appeal's are dismissed."

3. The present appeals were admitted by the Coordinate Bench of this Court on 30.04.2009 on the following substantial question of law:"Whether on the facts and in the circumstances of the case, the Income Tax Appellate Tribunal was right in holding that expenditure on replacement of old machinery by purchase and installation of machinery was allowable as revenue expenditure"

4. The learned Senior Standing Counsel for the Revenue submitted that the controversies now settled by the Hon'ble Supreme Court in the case of Commissioner of Income Tax, Gujarat Vs. Sarangpur Cotton Mfg. Co. Ltd., [2017] 80 taxmann.com 260 (SC), in which, the Hon'ble Supreme Court has held as under:"8.Learned Additional Solicitor General submitted that the view taken by the Gujarat High Court by relying on two decisions in the case of CIT v. Baroda Industrial Development Corpn. Ltd. [1992] 198 ITR 716/65 Taxman 359 (Guj.) and in the case of CIT v. Satyadev Chemical Ltd. [1997] 226 ITR 95 (Guj.) has been impliedly overruled by this Court in the case of CIT v. Sraavana Spg. Mills (P.) Ltd. [2007] 293 ITR 201/63 Taxman 201 (SC). She submitted that each items for which deduction under the head "current repairs" was sought is a machine by itself and therefore deduction under Section 31(i) cannot be allowed. She invited out attention to paragraphs 9, 10, 12, 13 and 14 of hte judgment in the case of Saravana Spg. Mills (P.) Ltd. (supra) and submitted that if the current repairs related to independent machines itself instead of repairs of a part of that machine, deduction cannot be granted under Section 31(i) of the Income Tax Act, 1961. In Saravana Spg. Mills (P) Ltd. (supra) this Court has held that in a textile mill there are several department/divisions. In each department/division there are several machines and perform different functions. Therefore, when each of the Department/Division perform different functions, repair/substitution of an old machine will not come within the definition of the word "current repairs" and deduction cannot be claimed thereunder.

9.In this view of the matter, we are of the considered opinion that the impugned judgment and order passed by the Gujarat High Court as also the orders passed by the Income Tax Appellate Tribunal and the Commissioner of Income Tax Appeals on this issue cannot be sustained and are thereby set aside. It is held that the respondent is not entitled for any deduction under the head "current repairs" as claimed and allowed by the two authorities."

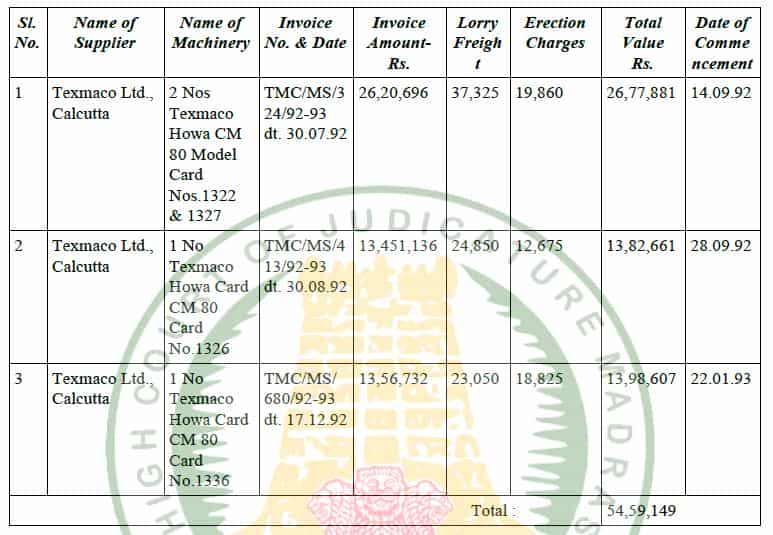

5. None has appeared on behalf of the respondent/Assessee despite service. 6. The replacement of the machineries in the present case which came up for consideration by the Assessing Authority as per the details of Replacement of Machinery submitted by the Assessee himself, which form part of the Assessment Order are quoted below for ready reference.

7. The total replacement cost of three machineries in question purchased by the Assessee amounting to Rs.54,59,149/- came to be allowed by the Tribunal as 'repairs maintenance expenditure' or 'revenue expenditure'. The said findings of the learned Tribunal are clearly contrary to the decision of the Hon'ble Supreme Court (cited supra) and therefore, the view of the Tribunal cannot be sustained and the replacement of the machineries as a whole by the Assessee cannot be held to be current repairs or allowable revenue expenditure.

8. Therefore, respectfully following the binding precedent of the Hon'ble Supreme Court in the case of Commissioner of Income Tax, Gujarat V. Sarangpur Cotton Mfg. Co. Ltd., the present Appeals filed by the Revenue deserves to be allowed and the substantial question of law framed is answered in favour of the Revenue and against the Assessee, we accordingly do so.

The Appeals are accordingly allowed. No order as to costs.

Click here to Download the Order

For Regular Updates Join : https://t.me/Studycafe

Tags : Judgement, High CourtAbout Author

Pratibha Goyal

Admin

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts