Set-off and carry forward of Losses in Income Tax:

Set-off and carry forward of Losses in Income Tax Some important points about Set-off and carry forward of Losses: As there can never be a loss under…

Set-off and carry forward of Losses

Table of Contents

Set-off and carry forward of Losses in Income Tax

Some important points about Set-off and carry forward of Losses:

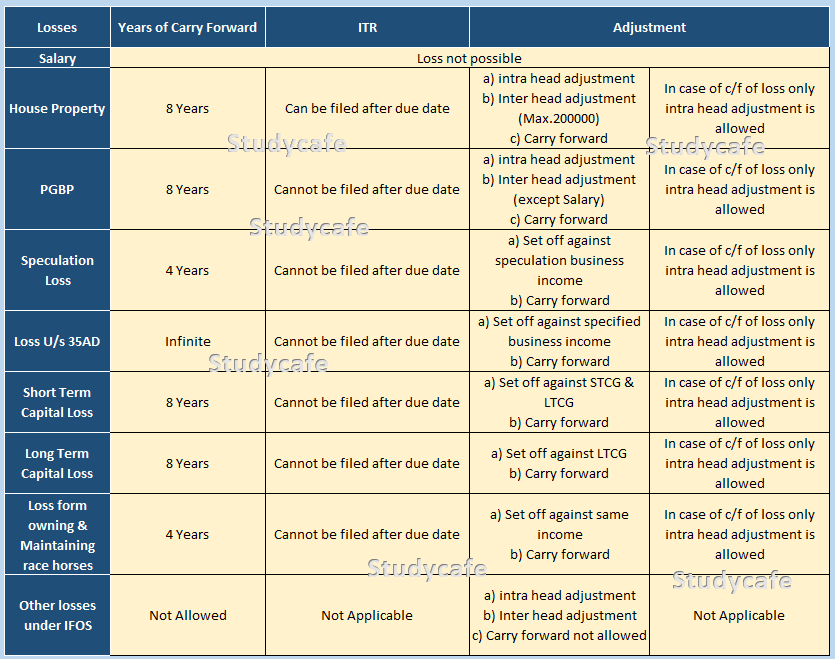

- As there can never be a loss under the head salary, set off or carry forward of the same is not possible.

- Carry forward and Set off of the losses under Income from Other Sources is not allowed.

- The losses which could not be set off either by way of Intra head adjustments or Inter head adjustments are allowed to be carried forward to the future years

- There is no restriction on setting off the losses if the return is filed after the due date.

- Set of can be Intra-head and Inter-head.

Intra Head Adjustment

- Losses from speculative business cannot be set off against income from non speculative business. But Losses from non speculative business can be set off with income from speculative business.

- Long Term Capital Loss cannot be set off with Short Term Capital Gain.

- No Loss can be Set off with any casual income i.e., Income from lotteries, crossword puzzles, race including horse race, card game, and any other game of any sort or from gambling or betting of any form or nature.

- Losses from the business of owning and maintaining racehorses cannot be set off against any income other than income from the business of owning and maintaining racehorses.

- Losses from the business specified under Section 35AD (Specified Business) cannot be set off against Incomes other than income from business specified under Section 35AD. But Losses from Non-Specified Business can be set off against Income of Specified Business

Inter Head Adjustment

- Losses from speculative business cannot be set off against income under any other head.

- Losses under the head PGBP cannot be set off against Salary Income.

- Losses under the head Capital Gain cannot be set off against any other head. But Losses under any other head can be set off with Income under the head Capital Gain.

- No loss can be set off against casual incomes.

- Losses from the business of owning and maintaining racehorses cannot be set off against any other head.

- Loss from the business specified under section 35AD cannot be set off against any other head of income.

- Loss from House property can be set off from any head of income but maximum to the extent of Rs. 200000

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts