Special Conditions in Certain Cases Regarding Issue of Capital Instruments in FDI

Streamlining of Issue of shares through Rights Issue and Bonus Issue The NEW FDI Regulations have streamlined the issue of shares under the

Table of Contents

Streamlining of Issue of shares through Rights Issue and Bonus Issue

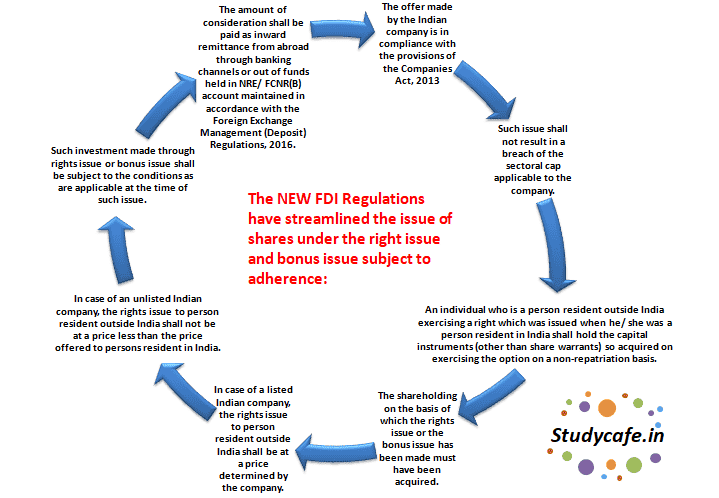

The NEW FDI Regulations have streamlined the issue of shares under the right issue and bonus issue subject to adherence:

1.) The offer made by the Indian company is in compliance with the provisions of the Companies Act, 2013

2.) Such issue shall not result in a breach of the sectoral cap applicable to the company.

3.) An individual who is a person resident outside India exercising a right which was issued when he/ she was a person resident in India shall hold the capital instruments (other than share warrants) so acquired on exercising the option on a non-repatriation basis.

4.) The shareholding on the basis of which the rights issue or the bonus issue has been made must have been acquired.

5.) In case of a listed Indian company, the rights issue to person resident outside India shall be at a price determined by the company.

6.) In case of an unlisted Indian company, the rights issue to person resident outside India shall not be at a price less than the price offered to persons resident in India.

7.) Such investment made through rights issue or bonus issue shall be subject to the conditions as are applicable at the time of such issue.

8.) The amount of consideration shall be paid as inward remittance from abroad through banking channels or out of funds held in NRE/ FCNR(B) account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016.

Special Conditions in Certain Cases Regarding Issue of Capital Instruments in FDI

Special Conditions in Certain Cases Regarding Issue of Capital Instruments in FDI

Where the original investment has been made on a non-repatriation basis, the amount of consideration may also be paid by debit to the NRO account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016.

One major change introduced is that the right shares can now be renounced by a person resident outside India in favour of another person resident outside India. Such renunciation of right shares was not possible in the earlier regime. This will result in much convenience in issuing shares through rights issue to a non resident (in whose favour the rights have been renounced), even if he is not an existing shareholder.

Issue of shares under Employees Stock Options Scheme to persons resident outside India

An Indian company may issue employees stock option and/ or sweat equity shares to its employees/ directors or employees/ directors of its holding company or joint venture or wholly owned overseas subsidiary/ subsidiaries who are resident outside India. Conditions are:

1.) The scheme has been drawn either in terms of regulations issued under the Securities and Exchange Board of India Act, 1992 or the Companies (Share Capital and Debentures) Rules, 2014 notified by the Central Government under the Companies Act 2013, as the case may be

2.) The employees stock option/ sweat equity shares so issued under the applicable rules/ regulations are in compliance with the sectoral cap applicable to the said company.

3.) Issue of employees stock option/ sweat equity shares in a company where investment by a person resident outside India is under the approval route shall require prior Government approval. Issue of employees stock option/ sweat equity shares to a citizen of Bangladesh/ Pakistan shall require prior Government approval.

4.) The face value of the shares to be allotted under the scheme to the non-resident employees does not exceed 5 per cent of the paid-up capital of the issuing company.

5.) An individual who is a person resident outside India exercising an option which was issued when he/ she was a person resident in India shall hold the shares so acquired on exercising the option on a non-repatriation basis.

Share Swap

In cases of investment by way of swap of shares, irrespective of the amount, valuation of the shares will have to be made by a Category I Merchant Banker registered with SEBI or an Investment Banker outside India registered with the appropriate regulatory authority in the host country. Approval of the Government conveyed through Foreign Investment Promotion Board (FIPB) will also be a prerequisite for investment by swap of shares.

Acquisition of capital instruments under Scheme of Merger/ Demerger/ Amalgamation

Mergers/ demergers/ amalgamations of companies in India are usually governed by an order issued by a competent Court on the basis of the Scheme submitted by the companies undergoing merger/ demerger/ amalgamation has been approved by National Company Law Tribunal (NCLT)/ Competent Authority, the transferee company or new company is allowed to issue shares to the shareholders of the transferor company resident outside India, subject to the conditions that:

i) the percentage of shareholding of persons resident outside India in the transferee or new company does not exceed the sectoral cap, and

ii) the transferor company or the transferee or the new company is not engaged in activities which are prohibited under the FDI policy.

Where a Scheme of Arrangement for an Indian company has been approved by National Company Law Tribunal (NCLT)/ Competent Authority , the Indian company may issue non-convertible redeemable preference shares or non-convertible redeemable debentures out of its general reserves by way of distribution as bonus to the shareholders resident outside India, subject to the following conditions, namely:

i) The original investment made in the Indian company by a person resident outside India is in accordance with these Regulations and the conditions specified in the relevant Schedule.

ii) The said issue is in accordance with the provisions of the Companies Act, 2013 and the terms and conditions, if any, stipulated in the scheme approved by National Company Law Tribunal (NCLT)/ Competent Authority have been complied with.

iii) The Indian company shall not engage in any activity/ sector in which investment by a person resident outside India is prohibited.

Thanks & Regards

CA Sanskriti Jain

Mb. No. 8745961214

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.