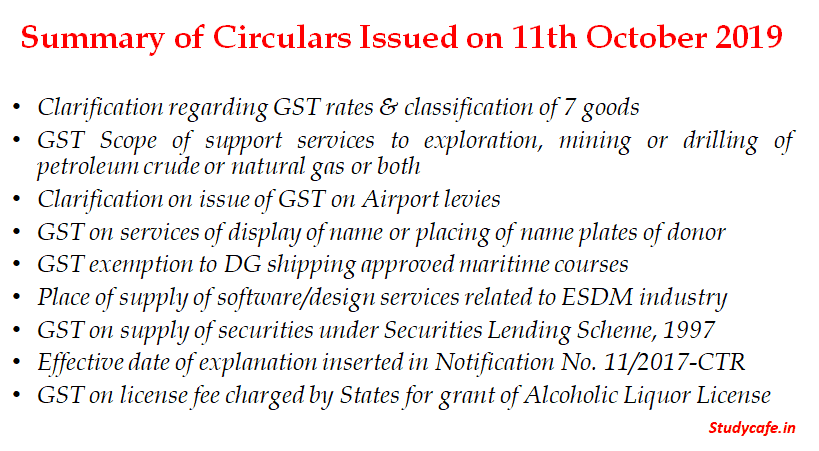

Summary of Circulars Issued on 11th October 2019

Summary of Circulars Issued on 11th October 2019 Circular No. 113/32/2019-GST Clarification regarding GST rates & classification of 7 go

Summary of Circulars Issued on 11th October 2019

Clarification regarding GST rates & classification of 7 goods :

(i) Classification of leguminous vegetables such as grams when subjected to mild heat treatment

Leguminous vegetables which are subjected to mere heat treatment for removing moisture, or for softening and puffing or removing the skin, and not subjecting to any other processing or addition of any other ingredients such as salt and oil, would be classified under HS code 0713. Such goods if branded and packed in a unit container would attract GST at the rate of 5%. In all other cases such goods would be exempted from GST.

(ii) Almond Milk

Almond milk is classified under the residual entry in the tariff item 2202 99 90 and attract GST rate of 18%.

(iii) Applicable GST rate on Mechanical Sprayer

Mechanical sprayers of all types whether or not hand operated (other than fire extinguishers, whether or not charged) would attract GST rate of 12%

(iv) Taxability of imported stores by the Indian Navy

Imported stores for use in navy ships are exempted from GST.

(v) Taxability of goods imported under lease : Goods imported under lease are exempted from IGST.

(vi) Applicable GST rate on parts for the manufacture solar water heater and system : Parts including Solar Evacuated Tube for the manufacture of solar water heater and system will attract GST rate of 5%.

(vii) Applicable GST on parts and accessories suitable for use solely or principally with a medical device : Parts and accessories used with a medical device (Ophthalmic equipment) should be classified with the

ophthalmic equipment only and shall attract GST rate of 12%.

GST Scope of support services to exploration, mining or drilling of petroleum crude or natural gas or both

- New entry has been inserted under heading 9983 w.e.f 1-10-2019 vide Notification No. 20/2019- Central Tax (Rate) dated 30-09-2019; - (ia) Other professional, technical and business services relating to exploration, mining or drilling of petroleum crude or natural gas or both

- Relevant Explanatory Notes for Heading 9983: 998341 Geological and geophysical consulting services 998343 Mineral exploration and evaluation

- Explanatory Notes for Heading 9986:

- 998621 Support services to oil and gas extraction

- 998622 Support services to other mining n.e.c

- Sr. 24 (ii) under heading 9986 will be governed by service codes 998621 and 998622

- Sr. No. 21 (ia) under heading 9983 will be governed by service codes 998341 and 998343

Clarification on issue of GST on Airport levies

The airport operators shall pay GST on the PSF and UDF collected by them from the passengers through the airlines.

Airline can act as pure agent (provided all conditions are satisfied under rule 33) on the airport services like Passenger Service Fee (PSF) and User Development Fees (UDF) provided by Airport Operators to the passengers.

The airline (pure agent) shall not take ITC of GST payable or paid on PSF and UDF. The airline would only recover from the passengers the actual PSF and UDF and GST payable on such PSF and UDF by the airline operator

Airlines shall be liable to pay GST on the collection charges under forward charge. ITC of the same will be available with the airport operator.

GST on services of display of name or placing of name plates of donor

GST shall not be leviable if 3 conditions are satisfied which are: 1. gift or donation is made to a charitable organization 2. the payment has the character of gift or donation 3. the purpose is neither commercial gain nor advertisement

GST exemption to DG shipping approved maritime courses

The Maritime Institutes are educational institutions under GST and the courses conducted by them are exempt from GST.

The exemption is subjected to meeting the condition specified at SL. No.66 of the notification No.12/2017 CTR dated 28-06-2017

The aforesaid clarification applies, mutatis mutandis, to corresponding entries of respective IGST, UTGST, SGST exemption notifications.

Place of supply of software/design services related to ESDM industry

Software/design services by supplier located in taxable territory to service recipient located in nontaxable territory by using sample prototype hardware / test kits in a composite supply, where such testing is an ancillary supply.

Place of supply is the location of the service recipient as per Section 13(2) of the IGST Act.

GST on supply of securities under Securities Lending Scheme, 1997

With effect from 1st Oct 2019, the borrower of securities shall be liable to discharge GST as per Sl. No 16 of Notification No. 22/2019-Central Tax (Rate) dated 30.09.2019 under RCM.

The nature of GST to be paid shall be IGST under RCM.

Effective date of explanation inserted in Notification No. 11/2017-CTR

The explanation having been inserted u/s 11(3) CGST Act, is effective from the inception of the entry at SL. No. 3(vi) of the Notification no. 11/2017 (CTR) Dated 28-06-2017 and 24/2017 (CTR) dated 21-09- 2017.

The line in Notification No. 17/2018(CTR) Dated 26-07-2018 mentioning effective date of notification as 27-07-2018 does not alter the operation of the notification in terms of Sec.11(3).

GST on license fee charged by States for grant of Alcoholic Liquor License

Granting of alcoholic liquor license, against consideration in the form of license fee or application fees by State Government has notified as neither a supply of goods nor supply of service as per Notification No. 25/2019(CTR) Dated 30-09-2019.

This notification is specifically applied to granting of alcoholic liquor license and has no applicability in relation to grant of other licenses for fees where GST is payable.

Click here to follow us on Telegram :https://t.me/studycafe

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

About Author

Pratibha Goyal

Admin

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts