Summary of Parameters for Scrutiny of GST returns (FY 17-18 & 18-19) as per SOP Issued

Summary of Parameters for Scrutiny of GST returns (FY 17-18 & 18-19) as per SOP issued Central Board of Indirect Taxes and Customs ( CBIC ) has r…

Summary of Parameters for Scrutiny of GST returns (FY 17-18 & 18-19) as per SOP issued

Central Board of Indirect Taxes and Customs (CBIC) has released Standard Operating Procedure (SOP) for Scrutiny of returns for FY 2017-18 and 2018-19.

The returns to be scrutinized will be chosen based on specific risk parameters.

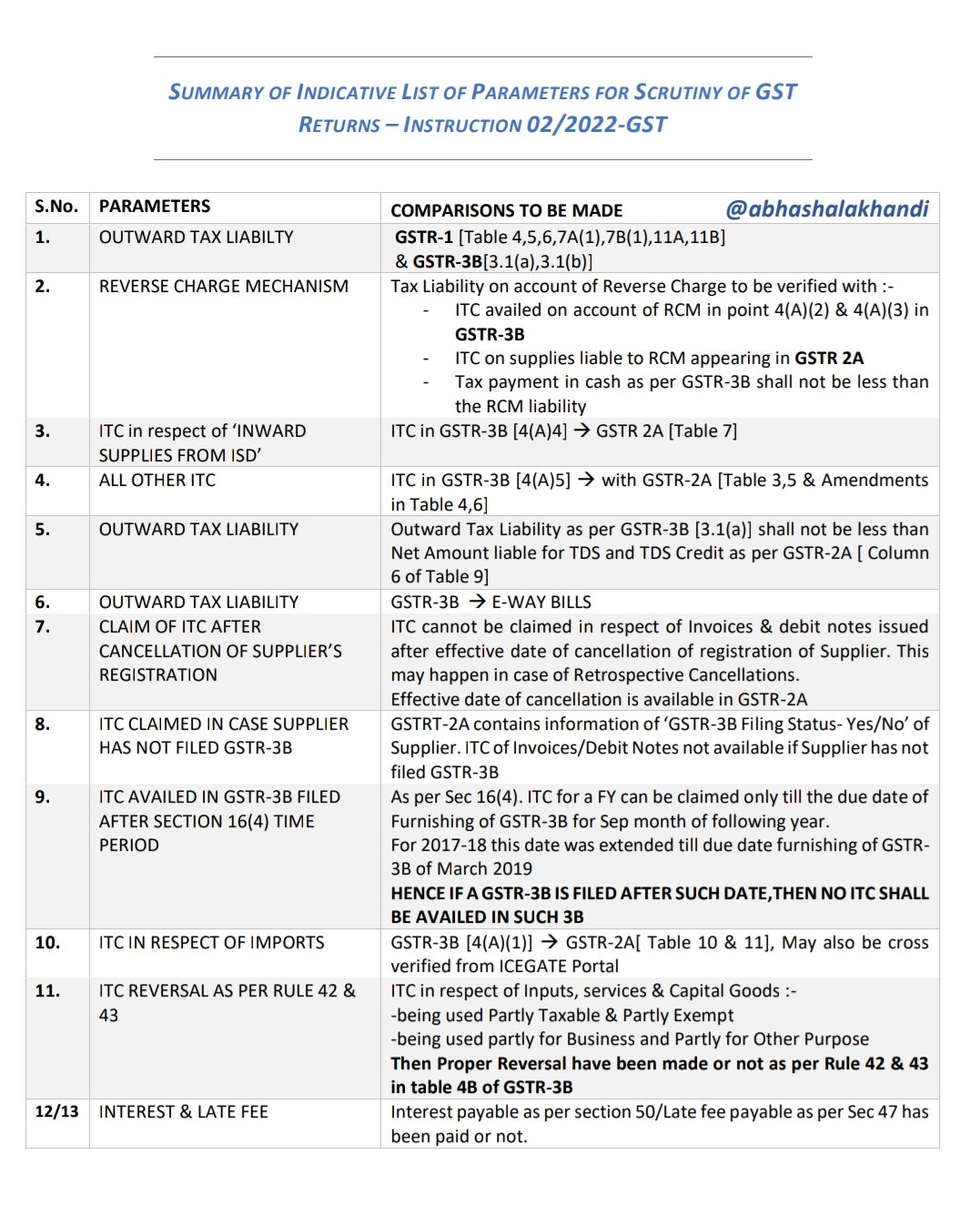

CA Abhas Halakhandi has shared 13 Parameters for Scrutiny of returns for FY 2017-18 and 2018-19.

1. Outward Tax Liability

GSTR-1 [Table 4,5,6,7A(1),7B(1),11A,11B] & GSTR-3B (3.1(a),3.1(b)]

2. Reverse Charge Mechanism

Tax Liability on account of Reverse Charge to be verified with :-

CA Abhas Halakhandi has shared 13 Parameters for Scrutiny of returns for FY 2017-18 and 2018-19 in his Twitter Account.

CA Abhas Halakhandi has shared 13 Parameters for Scrutiny of returns for FY 2017-18 and 2018-19 in his Twitter Account.

- ITC availed on account of RCM in point 4(A)(2) & 4(A)(3) in GSTR-3B

- ITC on supplies liable to RCM appearing in GSTR 2A

- Tax payment in cash as per GSTR-3B shall not be less than the RCM liability

- being used Partly Taxable & Partly Exempt

- being used partly for Business and Partly for Other Purpose

CA Abhas Halakhandi has shared 13 Parameters for Scrutiny of returns for FY 2017-18 and 2018-19 in his Twitter Account.

About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts