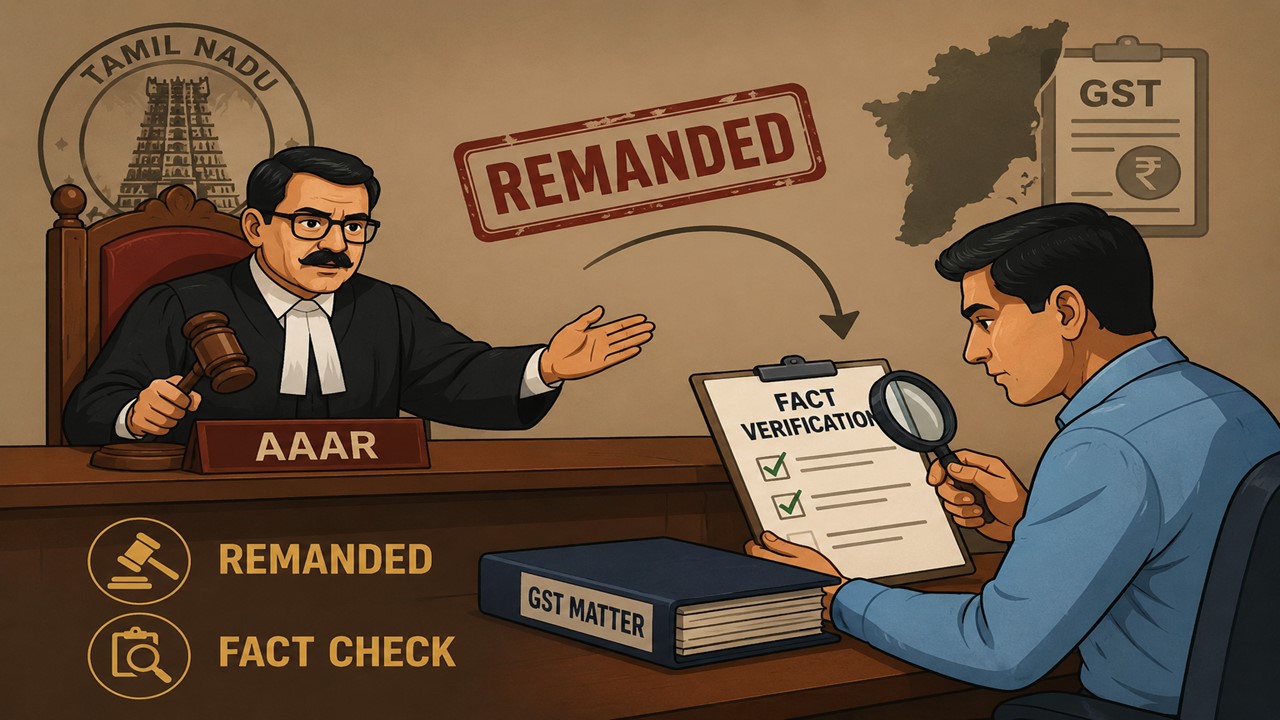

Tamil Nadu AAAR Remands GST Matter for Fresh Fact Verification:

Tamil Nadu AAAR remands GST appeal after finding contradictory factual submissions during appellate proceedings.

Appellate Authority found factual matrix materially changed during personal hearing

The Tamil Nadu State Appellate Authority for Advance Ruling (AAAR), in the case of M/s. Karthik & Co. (Order-in-Appeal No. AAAR/05/2026 (AR)), on 24 April 2026 remanded the matter back to the original Authority for Advance Ruling after observing substantial divergence between the facts presented in the original application and those argued during the appellate proceedings. The Appellate Bench comprising Member (CGST) Madan Mohan Singh and Member (SGST) S. Nagarajan held that such inconsistencies prevented a conclusive adjudication on merits.

The appellant had initially approached the Authority for Advance Ruling seeking clarification regarding GST implications arising out of certain non-monetary benefits. Aggrieved by the ruling passed by the lower authority, the appellant preferred an appeal before the AAAR. However, during the course of personal hearing and appellate submissions, the Authority noticed that the factual position projected before it was materially different from the facts originally placed before the AAR.

The AAAR observed that the facts furnished at the appellate stage were “completely different and divergent” from those contained in the original advance ruling application, thereby affecting the very basis on which the initial ruling had been rendered.

The Bench held that in the absence of factual consistency, it would not be appropriate to adjudicate the appeal on merits or determine the correctness of the earlier ruling. It emphasized that advance ruling proceedings are fundamentally fact-dependent and any substantial deviation in factual submissions requires fresh examination by the original authority itself.

The Authority further noted that proper adjudication would require verification and appreciation of the revised factual matrix, which could not be effectively undertaken for the first time at the appellate stage.

Thus, the AAAR set aside the impugned ruling and remanded the matter back to the original Authority for Advance Ruling for fresh consideration. The lower authority was directed to examine the matter afresh in light of the revised factual submissions and pass a fresh order in accordance with law after granting adequate opportunity of hearing to the appellant.

To Read Full Order, Download PDF Given Below.

About Author

Meetu Kumari

Content Manager

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2260

2260My Recent Articles

- ITAT Quashes Reassessment Over Unsigned Section 148 Notice Issued to AssesseePremium

- ITAT Sends Software and SaaS FTS Dispute Back for Fresh Review, Rules DTAA Tax Capping Includes Surcharge and CessPremium

- ITAT Orders Entity-Level Benchmarking for McCain India’s Transfer Pricing DisputePremium

- ITAT Deletes Rs 8.49 Crore Additions, Says CIT(A) Can Admit Evidence to Grant ReliefPremium

- ITAT Restores Appeal After Condoning Delay, Says Substantial Justice Must Prevail Over TechnicalitiesPremium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts