Taxation of digital economy and other key updates

Taxation of digital economy and other key updates Expansive interpretation of existing source-based taxing rights by Indian tax authorities

Taxation of digital economy and other key updates

Expansive interpretation of existing source-based taxing rights by Indian tax authorities

Taxation of digital economy and other key updates[/caption]

Taxation of digital economy and other key updates[/caption]

- Payments for several digital goods / services sought to be treated as royalty / FTS

- PE asserted based on websites / other digital activities

Domestic law changes

- Introduction of an ‘Equalisation Levy’ on online advertising / provision of digital advertising space (2016)

- New nexus rule - ‘Significant Economic Presence’ (‘SEP’)(2018)

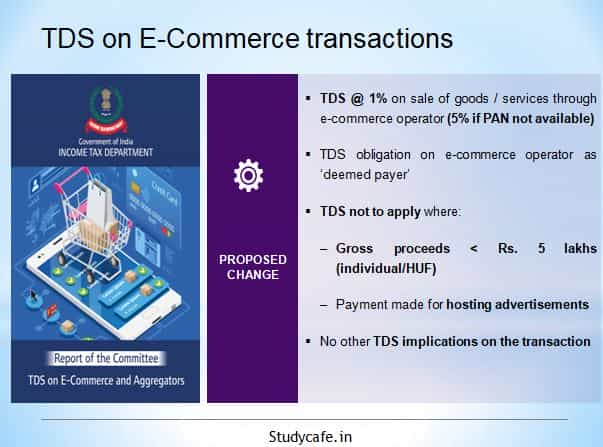

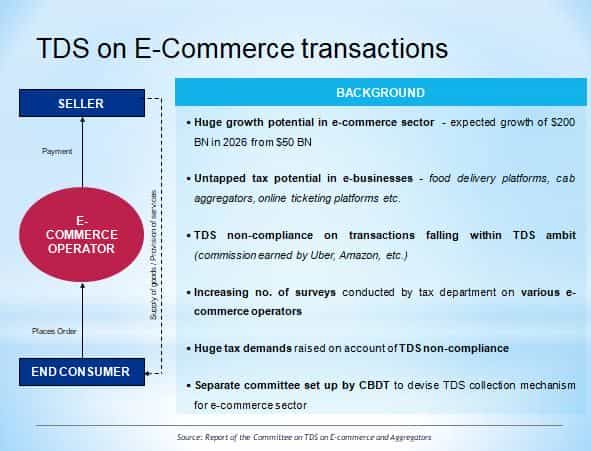

- Introduction of withholding tax on e-commerce transactions (2020)

- Deferral of SEP and expansion of Equalisation levy (2020)

Active participation in global initiatives

- Key player in the OECD BEPS initiatives on taxing the digitalised economy (Pillars One and Two)

- Proponent of expanded source based taxation

Expanding scope of business connection to include Significant Economic Presence

- Business connection to include significant economic presence (‘SEP’) in India

- SEP to cover the following:

- Transaction in respect of goods, services, property by NR in India including provision of download of data or software in India, if aggregate of payments during the year exceed the prescribed amount

- Systematic and continuous soliciting of business in India through digital means

- Engaging in interaction with prescribed number of users in India

- Taxation to be restricted to income attributable to activities leading to SEP in India

Changes to the SEP regime

- Existing SEP provisions omitted from AY 2021-22 and modified provisions to be inserted from AY 2022-23

- Source Rule expanded and modified w.e.f. AY 2021-22 to include income from:

- Advertisement that targets India customers

- Sale of data collected from India

- Sale of goods and services using such data collected from India

- Ongoing work at the OECD / G20 cited in the Budget Memorandum while deferring the SEP provisions

Taxation of digital economy and other key updates[/caption]

Applicability of Equalization Levy

As originally introduced w.e.f. 1 June 2016 ‘Specified services’ i.e.- Online advertisement;

- Any provision for digital advertising space; or

- Any other facility or service for the purpose of online advertisement

- Rate-6%

- Sale of goods owned by an e-commerce operator Online

- Provision of services provided by an e- commerce operator

- Online sale of goods or provision of services or both, facilitated by an e-commerce operator; or

- Any combination of the above

- Rate-2%

About Author

Pratibha Goyal

Admin

This Account belongs to Admistrator of Studycafe.

This Account belongs to Admistrator of Studycafe.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.