TCS Rates under Income Tax Act: TCS Rate Chart FY 22-23

TCS Rates under Income Tax Act: TCS Rate Chart FY 22-23 1. Tax collection at source (TCS) is an additional amount collected as tax by a seller of spe…

Table of Contents

6. Classification of Sellers and Buyers for TCS

(a) Under TCS mechanism a Seller is defined as any of the following:

(1) Central Government

(2) State Government

(3) Local Authority

(4) Statutory Corporation or Authority

(5) Company registered under Companies Act

(6) Partnership firms

(7) Co-operative Society

(8) Any person or HUF who is subjected to an audit of accounts under Income-tax Act for a particular financial year.

(b) A buyer is classified as a person who obtains goods or the right to receive goods in any sale, auction, tender or any other mode.

7. TCS is not necessary for the following buyers:

a. Public Sector Companies

b. Central Government, State Government, Embassy or High Commission

c. Consulate and other Trade Representative of a Foreign Nation

d. Clubs such as Sports Clubs and Social Clubs

e. Local authority for the purpose of purchase of vehicle

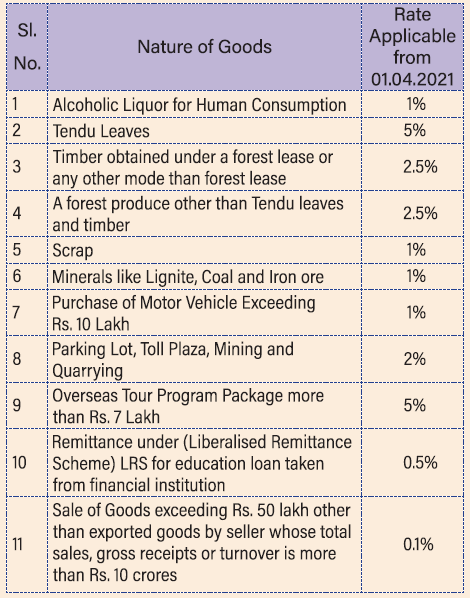

8. Goods transactions covered under TCS provisions and rates applicable to them. The rate of TCS is different for goods specified under different categories:

Note:

Note:

1. If the payer does not furnish PAN/ Aadhaar to TCS collector then rate of TCS is double or 5% whichever is higher for SI. No. 1 to 10 and for SI. No. 11 it is 5%.

2. With effect from 01.07.2021 if the payer (other than Non-resident who does not have Permanent Establishment in India) and has not filed the IT Return for last 2 Assessment Years, TCS rate is double or 5% whichever is higher.

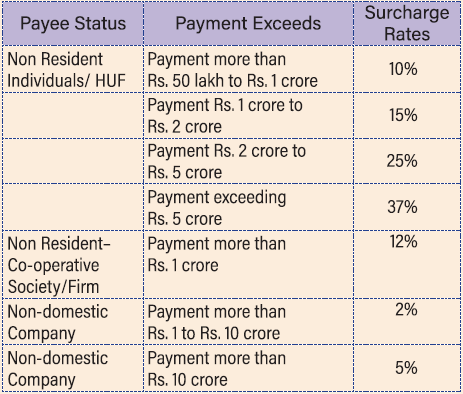

9. Health & Education Cess & Surcharge on TCS Rates

Health & Education Cess @ 4% on TCS + Surcharge as applicable.

Health & Education Cess @ 4% on TCS + Surcharge as applicable.

10. TCS Payments

(a) The seller shall deposit the TCS amount in Challan 281 within one week of the last day of the month in which the tax was collected. This remittance can be made in any branch of RBI, SBI or any other authorized bank or the same can also be remitted electronically.

(b) All sums collected by any Government office should be deposited on the same day of collection.

11. Failure to remit the TCS to Government Account shall attract following consequences:

a. If the tax collector responsible for collecting the tax and depositing the same to the Government does not collect the tax, then he will be liable to pay interest at the rate of 1% per month or part of the month in addition to the amount of TCS which he fails to collect. If, after collecting the TCS, he does not remit the same to the Government within due dates, then he is liable for interest at the rate of 1% per month of delay.

b. The person would also be liable for penalty u/s 271CA of the Act, which would be equal to amount of tax liable to be collected.

c. The person will also be liable for prosecution u/s 27688 of the Act, the term of which is upto 7 years of imprisonment.

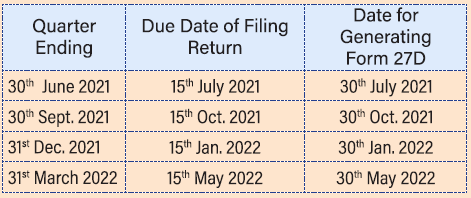

12. TCS Returns & Certificate of TCS

It is mandatory for all collectors of tax at source to furnish Quarterly TCS returns (Form 27EQ) to CPCTDS in electronic mode within the prescribed time. The collector can also file correction statement for rectification of any mistake, add/delete or update the information already furnished. Note: The Late Filing Fee of Rs. 200/- per day is chargeable for delay in filing ofTCS returns. The Collector of TCS has to provide a TCS certificate in Form 27D to the purchaser of the goods. The due dates for filing TCS quarterly returns and issue of TCS certificates is as under: Note: Failure to furnish certificate may attract penalty of Rs. 100/for every day of delay.

Note: Failure to furnish certificate may attract penalty of Rs. 100/for every day of delay.

13. TCS Exemptions

Tax collection at source is exempt in the following cases:(a) When the eligible goods are used for personal consumption

(b) The purchaser buys the goods for manufacturing, processing or production and not for the purpose of trading of those goods.

14. Lower Rate of TCS

The buyer (licensee) can apply to the Assessing Officer {TDS) for a lower rate Certificate by filing Form No. 13. Subject to the provisions of the Act, if the AO is convinced that the total income of the buyer (licensee) justifies the lower rate, the AO may issue a certificate specifying the rate of collection u/s 206C. This Certificate will be issued by the AO online through the TRACES portal.About Author

Reetu

Content Manager

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts