5 Activities which are NOT taxable under the GST regime!

5 Activities which are NOT taxable under the GST regime! Introduction The new GST regime will bolster the rapid growth of our nation and als

5 Activities which are NOT taxable under the GST regime!

Introduction

The new GST regime will bolster the rapid growth of our nation and also shall support the seamless flow of input tax credit. This is the reason behind very few exemptions under GST regime so that credit can be adjusted against the credit and it does not result into cascading effect.

However, it is imminent that exemption will be there as to control the inflation and to remove the genuine hardship.

So, there can be two types of cases where GST shall not apply:

- Case where GST is applicable but has been exempted via notification.

- Case where GST is not applicable at all.

- Activities specified in schedule III

- Activities or transaction undertaken by the government

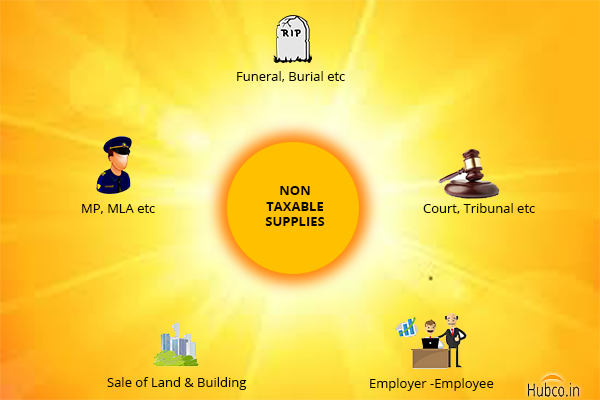

- Services by Employee to Employers: Had it been covered under GST, then the whole country would have liable to GST registration. Hence, it is very natural that services by employee to employer should b excluded from list of taxable services.

- Contract for Service: If a person is a employee then he must have signed the contract for service. Further, the person shall be paid fixed monthly remuneration, and the TDS shall be deducted under section 192 of the Income tax act.

- In Charge of: Another check is that the employer should be in charge of the employee and he sets the terms out there like how the thing is to be done. Further, some employers let the employee dictates the term but that does not mean that there is no employer employee relationship.

- No risk no reward: In case of employee-employer relationship, it is the employer who undertakes all the risk and also the related profit and loss. In any case, employee is not impacted by profit or loss.

- Part time employee: No where it is written or understood that employee can only be full time. Employee can be part time or can work on casual basis as well. There may be following factors deciding whether a person working is a part time employee or a service provider:

- In case of employee, there exists a master and servant relationship, however, between service providers the relationship is like between the professionals.

- In case of employees, the one person controls another person to fulfill his economic objectives, however, in case of service provider, both parties are independent.

- Difference between agent and employee: Employee and agent may look similar but they are not. There is a difference between the two terms. Further, it is very important from the GST point of view because the taxability is very different in both the cases.

- Sale of land and Building: This is another very important point to be discussed as GST is not applicable on sale of land or building, however, it is applicable if a service of construction of building is provided by one person to another.

- Services by Member of Parliament, MLA and others: Services provided by MP, MLA, person holding constitutional post are not liable for GST on their remuneration. This is because services provided by them have been excluded from the definition of supply.

- Election Commission of India

- Committee on infrastructure

- Law Commission of India

- National Commission on Farmers (NCF)

- National Commission for Women (NCW)

- National Commission for Minorities (NCM)

- Competition Commission of India (CCI)

- Service by Court or Tribunal: There are various types of court and tribunals working in our country. From Supreme Court of India to high court, district courts, tax tribunals etc are all example of courts and tribunal in India.

- Services of funeral, burial etc: The services of funeral, burial, crematorium or mortuary including the transportation of the deceased.

About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.