CBIC has notified the new procedure for registered persons engaged in the manufacturing of tobacco, pan masala etc.

Reetu | Jan 6, 2024 |

![CBIC notifies new procedure for registered person engaged in manufacturing of tobacco [Read Notification]](/cdn-cgi/image/fit=contain,format=webp,gravity=auto,metadata=none,quality=80,width=1200,height=730/wp-content/uploads/2024/01/New-procedure-for-registered-person-engaged-in-manufacturing-of-tobacco.jpg)

CBIC notifies new procedure for registered person engaged in manufacturing of tobacco [Read Notification]

The Central Board of Indirect Taxes and Customs (CBIC) has notified the new procedure for registered persons engaged in the manufacturing of tobacco, pan masala etc.

The Notification Read as follows:

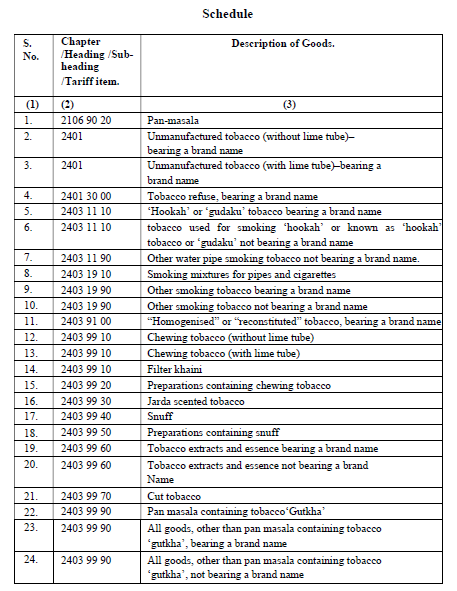

In exercise of the powers conferred by section 148 of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereinafter referred to as the said Act), the Central Government, on the recommendations of the Council, hereby notifies the following special procedure to be followed by a registered person engaged in manufacturing of the goods, the description of which is specified in the corresponding entry in column (3) of the Schedule appended to this notification, and falling under the tariff item, sub-heading, heading or Chapter, as the case may be, as specified in the corresponding entry in column (2) of the said Schedule.

(1) All the registered persons engaged in manufacturing of the goods mentioned in Schedule to this notification shall furnish the details of packing machines being used for filling and packing of packages in FORM GST SRM-I, electronically on the common portal, within thirty days of coming into effect of this notification.

(2) Any person intending to manufacture goods as mentioned in the Schedule to this notification, and who has been granted registration after the issuance of this notification, shall furnish the details of packing machines being used for filling and packing of packages in FORM GST SRM-I on the common portal, within fifteen days of grant of such registration.

(3) The details of any additional filling and packing machine being installed at the registered place of business shall be furnished, electronically on the common portal, by the said registered person within twenty-four hours of such installation in PART (B) of Table 6 of FORM GST SRM-I.

(4) If any change is to be made in the declared capacity of the machines, the same shall be furnished, electronically on the common portal, by the said registered person within twenty-four hours of such change in Table 6A of FORM GST SRM-I.

(5) Upon furnishing of such details in FORM GST SRM-I, a unique registration number shall be generated for each machine, the details of which have been furnished by the registered person, on the common portal.

(6) In case, the said registered person has submitted or declared the production capacity of his manufacturing unit or his machines, to any other government department or any other agency or organisation, the same shall be furnished by the said registered person in Table 7 of FORM GST SRM-I on the common portal, within fifteen days of filing such declaration or submission: Provided that where the said registered person has submitted or declared the production capacity of his manufacturing unit or his machines, to any other government department or any other agency or organisation, before the issuance of this notification, the latest such certificate in respect of the manufacturing unit or the machines, as the case may be, shall be furnished by the said registered person in Table 7 of FORM GST SRM-I on the common portal, within thirty days of issuance of this notification.

(7) The details of any existing filling and packing machine disposed of from the registered place of business shall be furnished, electronically on the common portal, by the said registered person within twenty-four hours of such disposal in Table 8 of FORM GST SRM-I.

The registered person shall submit a special statement for each month in FORM GST SRM-II, electronically on the common portal, on or before the tenth day of the month succeeding such month.

(1) The taxpayer shall upload a certificate of Chartered Engineer FORM GST SRM-III in respect of machines declared by him, as per para 1 of this notification, in Table 6 of FORM GST SRM-I.

(2) If details of any machine are amended subsequently, then a fresh certificate in respect of such machine shall be uploaded.

This notification shall come into effect from the 1st day of April 2024.

Explanation.– (1) In this Schedule, “tariff item”, “heading”, “sub-heading” and “Chapter” shall mean respectively, a tariff item, heading, sub-heading and Chapter as specified in the First Schedule to the Customs Tariff Act, 1975 (51 of 1975).

(2) The rules for the interpretation of the First Schedule to the said Customs Tariff Act, 1975, including the section and chapter notes and the General Explanatory notes of the First Schedule shall, so far as may be, apply to the interpretation of this notification.

(3) For the purposes of this notification, the phrase “brand name” means brand name or trade name, whether registered or not, that is to say, a name or a mark, such as symbol, monogram, label, signature or invented word or writing which is used in relation to such specified goods for the purpose of indicating, or so as to indicate a connection in the course of trade between such specified goods and some person using such name or mark with or without any indication of the identity of that person.

To Read More Download PDF Given Below:

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"