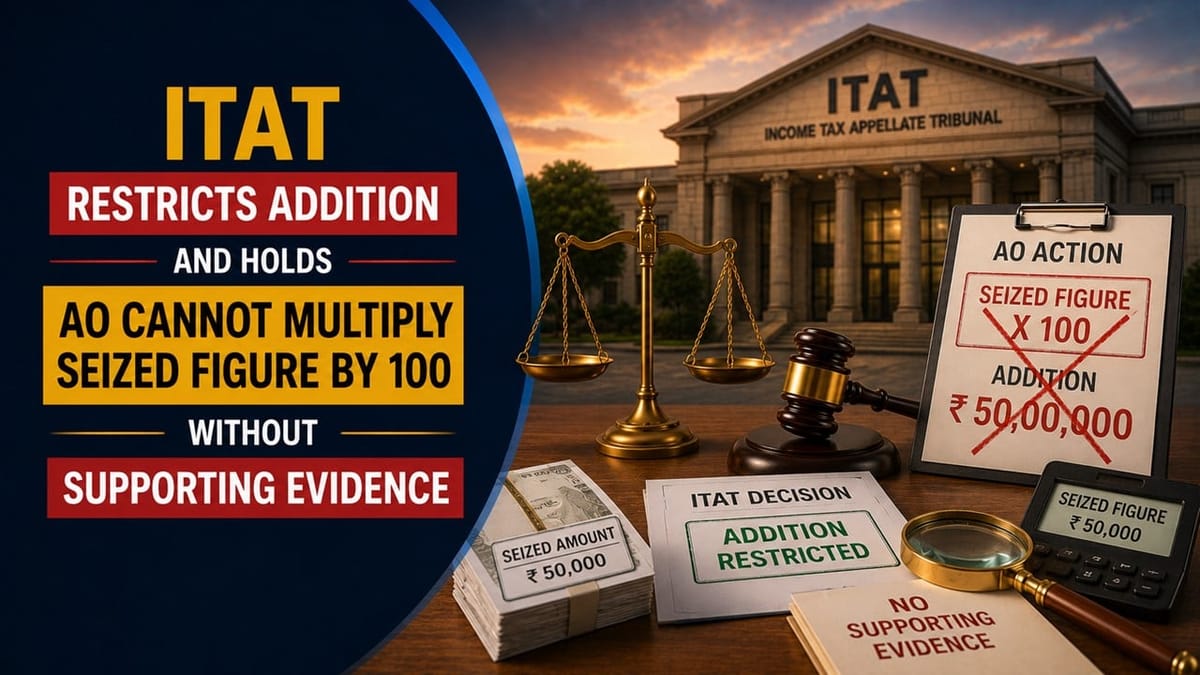

The Income Tax Appellate Tribunal (ITAT) Delhi has held that the AO was not justified in treating Rs 14,800 appearing in a seized document as Rs 14.80 lakh merely by multiplying the figure by 100.

Saima | Jun 24, 2026 |

ITAT Restricts Addition And Holds AO Cannot Multiply Seized Figure by 100 Without Supporting Evidence

The Income Tax Appellate Tribunal (ITAT) Delhi held that an addition under Section 69 of the Income Tax Act cannot be based on extrapolation of figures found in seized documents. If there is no supporting evidence, only the actual amount appearing in the seized material can be brought to tax.

The assessee is Parul Suyal, who had filed her return of income for assessment year 2020-21 declaring income of Rs 2.10 lakh. Later, a search under Section 132 of the Income Tax Act was conducted in the Omaxe Group cases on 14 March 2022, during which Excel sheets having details of cash payments by customers were seized. Based on the information received from the Investigation Wing, the AO initiated reassessment proceedings under Section 147 and issued notice under Section 148. According to the Revenue, an amount of Rs 14,800 appearing against the assessee’s name in the seized Excel file actually represented Rs 14.80 lakh and, accordingly, an addition of Rs 14,80,000 was made under Section 69 of the Act towards unexplained investment.

The addition was upheld by the CIT(A), following which the assessee approached the Tribunal.

The assessee contended that the addition had been made solely on the basis of third-party information without any independent inquiry or verification. It was argued that there was no basis for multiplying the amount of Rs 14,800 by 100 to arrive at Rs 14.80 lakh. It was further submitted that, in response to a notice issued under Section 133(6), Omaxe Group had itself denied receiving any cash payment from the assessee. The assessee also submitted that no opportunity for cross-examination had been granted despite his requests.

After examining the material available on record, the Tribunal observed that the Revenue had failed to produce any evidence supporting the assumption that the amount shown in the seized documents was required to be multiplied by 100. The Tribunal held that in the absence of any corroborative evidence, the AO was not justified in converting the figure of Rs 14,800 into Rs 14.80 lakh. Accordingly, the Tribunal directed the AO to restrict the addition under Section 69 of the Income Tax Act to Rs 14,800 and delete the balance addition. The appeal of the assessee was partly allowed.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"