arpithaldia | Apr 28, 2019 |

Presentation on GST Annual Return Containing complete analysis of GSTR-9

RELEVANT SECTION, RULE, NOTIFICATIONS AND ORDERS

Relevant Section: Section 44 read with Rule 80

Relevant Notification: Notification No. 74/2018-Central Tax Dated 31st December 2018

Order No. 1/2018 – Central Tax- Removal of difficulty order regarding extension of due date for filing of Annual return (in FORMs GSTR-9, GSTR-9A and GSTR-9C) for FY 2017-18 till 31st March, 2019

Order No. 2/2018 – Central Tax- Seeks to extend the due date for availing ITC on the invoices or debit notes relating to such invoices issued during the FY 2017-18

Order No. 3/2018 – Central Tax- Seeks to amend Removal of Difficulty Order No. 1/2018 dated 11.12.2018 so as to extend the due date for furnishing of annual returns in FORM GSTR-9, FORM GSTR-9A and reconciliation statement in FORM GSTR-9C for the FY 2017-2018 till 30.06.2019.

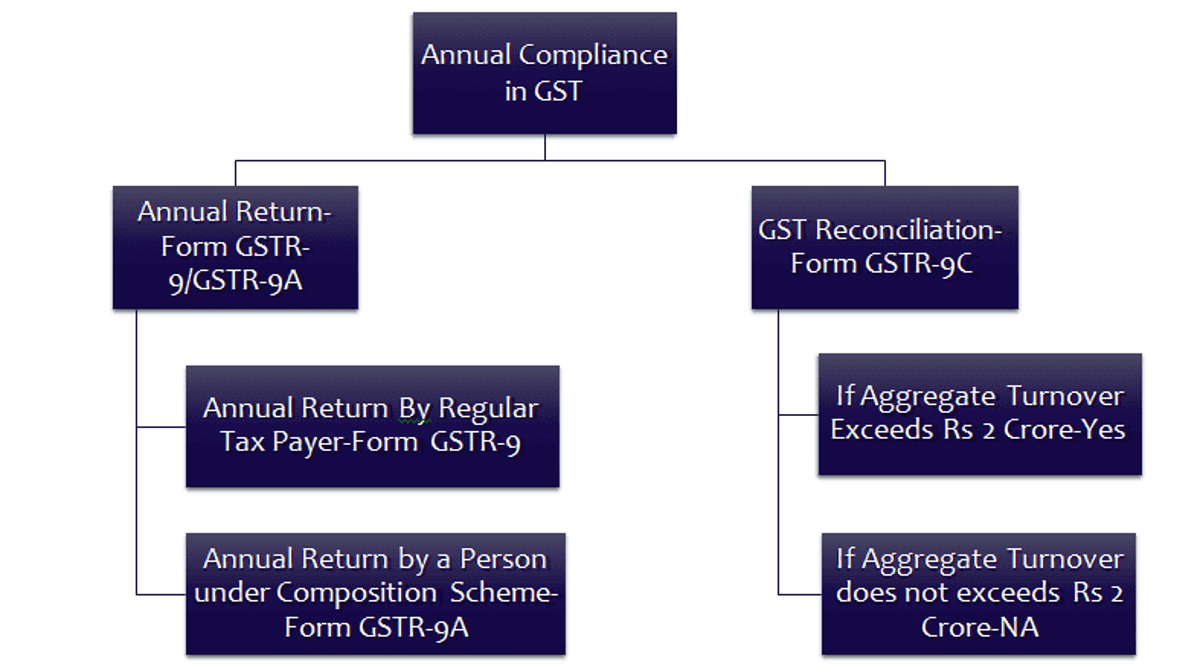

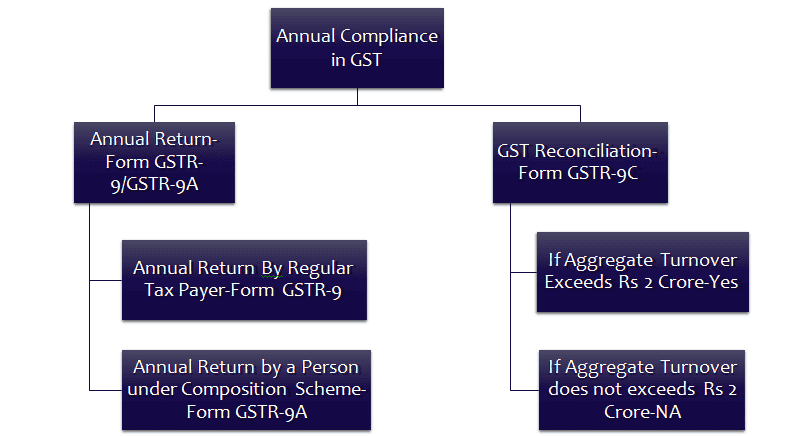

RELEVANT FORMS FOR THE PURPOSE OF ANNUAL RETURN AND RECONCILIATION FORMAT

a) GSTR-9 – Annual Return

b) GSTR-9A – Annual Return for (Composition Tax Payers)

c) GSTR-9C – Reconciliation Statement

WHO IS NOT REQUIRED TO FILE ANNUAL RETURN

1) Input Service Distributor,

2) A person paying tax under section 51 or section 52,

3) A casual taxable person and

4) A non-resident taxable person

5) Department of Central Government or State Government or local authority, whose books of account are subject to audit by the Comptroller and Auditor-General of India or an auditor appointed for auditing the accounts of local authorities under any law for the time being in force.

RELEVANT SECTION AND RULE

SECTION 44(1) ANNUAL RETURN

Every registered person, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non- resident taxable person, shall furnish an annual return for every financial year electronically in such form and manner as may be prescribed on or before the thirty-first day of December following the end of such financial year.

RULE 80(1) ANNUAL RETURN

Every registered person other than those referred to in the proviso to sub-section (5) of section 35, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non-resident taxable person, shall furnish an annual return as specified under sub-section (1) of section 44 electronically in FORM GSTR- 9 through the common portal either directly or through a Facilitation Centre notified by the Commissioner:

Provided that a person paying tax under section 10 shall furnish the annual return in FORM GSTR-9

Some FAQ’s on GST Annual Return

| Q. N | Question | Answer |

| 1 | Is this return to be furnished by person whose registration has been cancelled during the year 2017-18 | Yes, Annual return would have to be furnished by a person whose registration has been cancelled during the Year 2017-18. Further, if a person had applied for cancellation of registration and his application for cancellation of registration was pending as on 31st March 2018, he also would be required to file Annual Return. |

| 2 | Is Annual return to be filed by the person who had migrated to GST Regime provisionally but they had not cancelled their registration by filing REG-29 under Rule 24(4) of the CGST Rules, 2017 with effect from 1st July 2017 | No, such persons would not be required to file Annual Return for the Year 2017-18. |

| 3 | Whether Annual Return can be filed without filing GSTR-1 and GSTR-3B for the Year 2017-18 | No, it is mandatory to file FORM GSTR-1 and FORM GSTR-3B for FY 2017-18 before filing Annual return in FORM GSTR-9 |

| 4 | Whether any additional liability can be declared through GSTR-9 | Yes, Additional liability for the FY 2017-18 not declared in FORM GSTR-1 and FORM GSTR-3B may be declared in this return (Instruction 3) |

| 5 | Whether any additional input tax credit can be claimed through GSTR-9 | No, taxpayers cannot claim input tax credit unclaimed during FY 2017-18 through this return (Instruction 4) |

| 6 | How would Annual Return be filed by a person who was under composition scheme for part of year and under regular scheme for remaining part of the Year | Such persons would have to file GSTR-9 for the period under which they were under Regular Scheme and GSTR-9A for the period under which they were composition scheme. |

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"