CS Lalit Rajput | May 31, 2019 |

Corporate Compliance Calendar for the m/o June, 2019

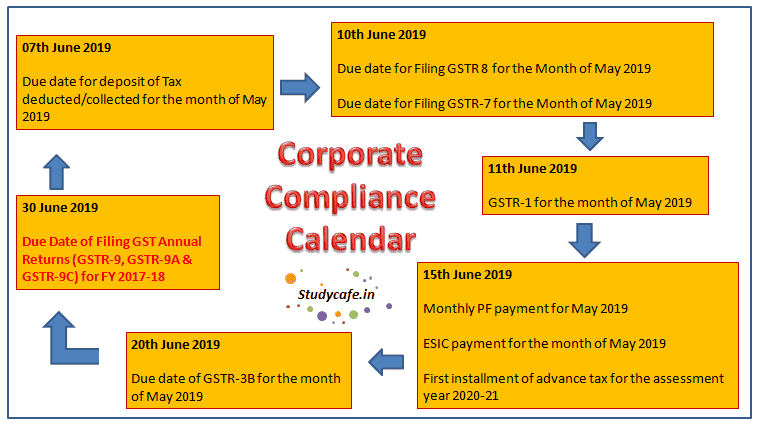

CORPORATE Compliance CALENDAR For the month of June, 2019

About Article :

This article contains various Compliance requirements under Statutory Laws. Compliance means adhering to rules and regulations.

Compliances under:

1.) Compliance Requirement Under Income Tax Act, 1961

2.) Compliance Requirement Under Goods & Services Act, (GST) 2017

3.) Compliance Under Other Statutory Laws

4.) Compliance Requirement Under SEBI (Listing Obligations And Disclosure Requirements) (LODR) Regulations, 2015

5.) Compliance Requirement For Companies Act, 2013

1.) Compliance requirement under Income Tax act, 1961

| Applicable Laws/Acts | Due Dates | Compliance Particulars | Forms/ (Filing mode) |

| Income Tax Act, 1961 | 07.06.2019 | Due date for deposit of Tax deducted/collected for the month of May, 2019.However, all sum deducted/collected by an office of the government shall be paid to the credit of the Central Government on the same day where tax is paid without production of an Income-tax Challan | TDS & TCS |

| Income Tax Act, 1961 | 14.06.2019 | Due date for issue of TDS Certificate for tax deducted under section 194-IA in the month of April, 2019 | TDS Certificate u/s 194-IA |

| Income Tax Act, 1961 | 14.06.2019 | Due date for issue of TDS Certificate for tax deducted under section 194-IB in the month of April, 2019 | TDS Certificate u/s 194-IB |

| Income Tax Act, 1961 | 15.06.2019 | Due date for furnishing of Form 24G by an office of the Government where TDS/TCS for the month of May, 2019 has been paid without the production of a challan | Form 24G |

| Income Tax Act, 1961 | 15.06.2019 | Quarterly TDS certificates (in respect of tax deducted for payments other than salary) for the quarter ending March 31, 2019 | |

| Income Tax Act, 1961 | 15.06.2019 | First installment of advance tax for the assessment year 2020-21 | |

| Income Tax Act, 1961 | 15.06.2019 | Certificate of tax deducted at source to employees in respect of salary paid and tax deducted during Financial Year 2018-19 | |

| Income Tax Act, 1961 | 15.06.2019 | Due date for furnishing statement in Form no. 3BB by a stock exchange in respect of transactions in which client codes been modified after registering in the system for the month of May, 2019 | Form 3BB |

| Income Tax Act, 1961 | 29.06.2019 | Due date for e-filing of a statement (in Form No. 3CEK) by an eligible investment fund under section 9A in respect of its activities in financial year 2018-19. | Form No. 3CEK |

| Income Tax Act, 1961 | 30.06.2019 | Due date for furnishing of challan-cum-statement in respect of tax deducted under section 194-IA in the month of May, 2019 | challan-cum-statement u/s 194-IA |

| Income Tax Act, 1961 | 30.06.2019 | Due date for furnishing of challan-cum-statement in respect of tax deducted under section 194-IB in the month of May, 2019 | challan-cum-statement u/s 194-IB |

| Income Tax Act, 1961 | 30.06.2019 | Return in respect of securities transaction tax for the financial year 2018-19 | |

| Income Tax Act, 1961 | 30.06.2019 | Quarterly return of non-deduction of tax at source by a banking company from interest on time deposit in respect of the quarter ending March 31, 2019 | |

| Income Tax Act, 1961 | 30.06.2019 | Statement to be furnished (in Form No. 64C) by Alternative Investment Fund (AIF) to units holders in respect of income distributed during the previous year 2018-19 | Form No. 64C |

| Income Tax Act, 1961 | 30.06.2019 | Report by an approved institution/public sector company under Section 35AC(4)/(5) for the year ending March 31, 2019 | |

| Income Tax Act, 1961 | 30.06.2019 | Due date for furnishing of statement of income distributed by business trust to its unit holders during the financial year 2018-19. This statement is required to be furnished to the unit holders in form No. 64B | form No. 64B |

2.) Compliance Requirement under Goods & Services Act, (GST) 2017

| Applicable Laws/Acts | Due Dates | Compliance Particulars | Forms / (Filing mode) |

| GST, Act, 2017 | 10.06.2019 | Form GSTR-7 for the month of May, 2019 (TDS Deductor) | GSTR-7 |

| GST, Act, 2017 | 10.06.2019 | TCS Collector (for the month of May, 2019) | GSTR – 8 |

| GST, Act, 2017 | 11.06.2019 | Return of outward supplies of taxable goods and/or services for the Month of May 2019 (for Assesses having turnover exceeding 1.5 Cr.) Monthly Return. | GSTR 1 |

| GST, Act, 2017 | 13.06.2019 | Due date for Furnishing return of May 2019 by Input Service Distributors (ISD) | GSTR – 6 |

| GST, Act, 2017 | Payment of tax shall be made by 20th of the month succeeding the month to which the liability pertains. | Payment of self-assessed tax | PMT-08 |

| GST, Act, 2017 | 18 months after end of the quarter for which refund is to be claimed | Application for Refund | RFD-10 |

| GST, Act, 2017 | 20.06.2019 | Summary of outward taxable supplies and tax payable by Non-Resident taxable person & OIDAR respectively.(for the month of March, 2019) | GSTR-5 & GSTR – 5A |

| GST, Act, 2017 | 20.06.2019 | Simple GSTR return for the month of May, 2019 | GSTR 3B |

| GST, Act, 2017 | 30.06.2019 | Annual Returns for FY 2017-18 | GSTR-9, GSTR-9A & GSTR-9C |

Note:

April GST return filing deadline extended till 20 June in parts of Odisha

Government extends the deadline of GSTR-3B and GSTR-1 for the specified 14 districts in Odisha to June 20 and June 10, respectively.

14 Specified Districts:

| Angul | Balasore | Bhadrak | Cuttack | Dhenkanal | Ganjam | Jagatsinghpur |

| Jajpur | Kendrapara | Keonjhar | Khordha | Mayurbhanj | Nayagarh | Puri |

Link: https://finance.odisha.gov.in/notifications/2019/24.pdf

and https://finance.odisha.gov.in/notifications/2019/23.pdf

3.) Compliance under Other Statutory LAws

| Applicable Laws/Acts | Due Dates | Compliance Particulars | Forms / (Filing mode) |

| EPF (The Employees Provident Funds And Miscellaneous Provisions Act, 1952) | 15.05.2019 | PF Payment for April, 2019 | ECR |

| ESIC (Employees’ State Insurance Act, 1948) | 15.05.2019 | ESIC Payment for April, 2019 | ESI Challan |

| PF Return – Monthly | 25.06.2019 | Pf Return Filling For May 2019 (Including Pension & Insurance Scheme Forms | PF Return |

4.) Compliance Requirement under SEBI (Listing Obligations and Disclosure Requirements) (LODR) Regulations, 2015

| FILING MODE(s) : For BSE : BSE LISTING CENTRE For NSE : NEAPS Portal |

Annual Compliances

| Sl. No. | Regulation No. | Compliance Particular | Compliance Period(Due Date) |

| 1 | Regulation 14 | Listing fees & other Charges | Payment manner as specified by the Board of by Recognised Stock Exchange. |

| 2 | Regulation 34*(shall be amended w.e.f. April 2019) | Annual Report | Within 21 working days from the AGM Date |

Event based Compliances

| Sl. No. | Regulation No. | Compliance Particular | Compliance Period(Due Date) |

| 1. | Regulation 7 (5) | Intimation of appointment / Change of Share Transfer Agent. | Within 7 days of Agreement with RTA. |

| 2. | Regulation 17(2) | Meeting of Board of Directors | The board of directors shall meet at least 4 times a year, with a maximum time gap of 120 days between any two meetings. |

| 3. | Regulation 18(2) | Meeting of the audit committee | The audit committee shall meet at least 4 times in a year and not more than 120 days shall elapse between two meetings. |

| 4. | Regulation 29 | Notice for Board Meeting to consider the prescribed matters. | The Company shall give an advance notice of:a) at least 5 days for Financial Result as per Regulation 29 1 (a) b) in case matters as stated in regulation 29 1 (b) to (f) 2 Working days in advance (Excluding the date of the intimation and date of the meeting) to Stock Exchange. c) 11 working days in case matter related to alteration in i) Securities ;ii) date of interest or redemption of Debenture / bond as per regulation 29(3) (a) ,(b). |

| 5 | Regulation 30 | Outcome of Board Meeting (Schedule III Part A- (4) | within 30 minutes of the closure of the meeting |

| 6. | Regulation 31 | Holding of specified securities and shareholding pattern | Reg. 31(1)(a): 1 day prior to listing of its securities on the stock exchange(s);Reg. 31(1)(c): within 10 days of any capital restructuring of the listed entity resulting in a change exceeding 2 % of the total paid-up share capital. |

| 7 | Regulation 46 | Company Website:. Listed entity shall disseminate the information as stated in Regulation 46 (2) | Shall update any change in the content of its website within 2 working days from the date of such change in content. |

| 8 | Regulation 33 | Financial Results(along with Limited review report/ Auditors report for the quarter ended December 2018) | Within 45 days from quarter end(except in case of Annual Financial Result, within 60 days from end of Financial Year) |

SEBI (Prohibition of Insider Trading) Regulations, 2015

| Sl. No. | Regulation No. | Compliance Particular | Compliance Period(Due Date) |

| 1 | Regulation 7(2) Continual Disclosures | Every promoter, employee and director of every company shall disclose to the company the number of such securities acquired or disposed of within two trading days of such transaction if the value of the securities traded, whether in one transaction or a series of transactions over any calendar quarter, aggregates to a traded value in excess of ten lakh rupees (10,00,000/-) or such other value as may be specified. | Every company shall notify; within two trading days of receipt of the disclosure or from becoming aware of such information |

SEBI Takeover Regulations 2011

Disclosure of Acquisition and Disposal

| Sl. No. | Regulation No. | Compliance Particular | Compliance Period (Due Date) |

| 1 | Regulation 29(1) | Any acquirer who acquires shares or voting rights in a target company which taken together with shares or voting rights, if any, held by him and by persons acting in concert with him in such target company, aggregating to five per cent (5%) or more of the shares of such target company, shall disclose their aggregate shareholding and voting rights in such target company in such form as may be specified | Reg. 29(3): The disclosures required under Reg. 29 (1) and Reg. 29 (2) shall be made within two working days of the receipt of intimation of allotment of shares, or the acquisition of shares or voting rights in the target company to, i) every stock exchange where the shares of the target company are listed; and ii) the target company at its registered office. |

| 2 | Regulation 29(2) | Any acquirer, who together with persons acting in concert with him, holds shares or voting rights entitling them to five per cent(5%) or more of the shares or voting rights in a target company, shall disclose every acquisition or disposal of shares of such target company representing two per cent(2%) or more of the shares or voting rights in such target company in such form as may be specified. |

5.) Compliance Requirement UNDER Companies Act, 2013 and Rules made thereunder;

| Applicable Laws/ Acts | Due Dates | Compliance Particulars | Forms / Filing mode |

| Companies Act, 2013 | Within 180 Days From The Date Of Incorporation Of The Company | As per Section 10 A (Commencement of Business) of the Companies Act, 2013, inserted vide the Companies (Amendment) Ordinance, 2018 w.e.f. 2nd November, 2018, a Company Incorporated after the ordinance and having share capital shall not commence its business or exercise any borrowing powers unless a declaration is filed by the Director within 180 days from the date of Incorporation of the Company with the ROC. Link | MCA E- Form INC 20A |

| Companies Act, 2013 | 30 days from the date of deployment of this form on the website of Ministry/ NFRA | Every existing body corporate other than a company governed by the NFRA Rules (Rule 3(1)), shall inform the (NFRA) about details of the auditor(s) as on 13th November 2018. Link | Form NFRA-1(e-form not yet deployed Ministry (ROC)) / NFRA |

| Companies Act, 2013 | 30.05.2019 (within 30 days of the form being made available by the MCA) | All Specified Companies (i.e. Companies who get supplies of goods or services from micro and small enterprises and whose payments to micro and small enterprise suppliers exceed 45 days from the date of acceptance or the date of deemed acceptance of the goods or services as per section 9 of the Micro, Small and Medium Enterprises Development Act, 2006) to file details of all outstanding dues to Micro or small enterprises suppliers existing on 22.01.2019 within thirty days. Link of the MCA notification : Link | Form MSME -1 a) One Time Return and b) Half Year Return (31.03.2019) |

| Companies Act, 2013 | within 90 days from the date of notification(earlier On or before 8th of May, 2019) | A person having Significant beneficial owner shall file a declaration to the reporting company Link i.e. within 90 days of the commencement of the Companies (Significant Beneficial Owners) Amendment Rules, 2019 | Form BEN-1(e-form not yet deployed by Ministry (ROC)) |

| Companies Act, 2013 | Within 30 Days | Filing of form BEN-2 under the Companies (Significant Beneficial Owners) Rules, 2018. (Within 30 days from the date of receipt of declaration in BEN-1) Link | Form BEN 2 (e-form not yet deployed by Ministry (ROC)) |

| Companies Act, 2013 | On or before 15.06.2019 | Filing of the particulars of the Company & its registered office.(by every company incorporated on or before the 31.12.2017.) Due date extended- Link : Link | Active Form INC -22A |

| Companies Act, 2013 | Within 30 Days from the date of deployment of revised e-form | DIN KYC through DIR 3 KYC Form is an Annual Exercise, however, the e-form presently is not designed in such manner and thus the due date for filing the e-form would be 30 days from the date of deployment of revised e-form. Link Penalty after due date is Rs. 5000/- | E-Form DIR 3 KYC ( Revised E-Form, Not yet deployed) |

| Companies Act, 2013 | within 60 days from the conclusion of each half year | Reconciliation of Share Capital Audit Report (Half-yearly)Pursuant to sub-rule Rule 9A (8) of Companies (Prospectus and Allotment of Securities) Rules, 2014 Applicable w.e.f. 30.09.2019 Link | E-Form PAS 6(E-Form, Not yet deployed) |

| Companies Act, 2013 | 29.06.2019 | First DPT-3 for amounts which are NOT deposits (exempted deposits) outstanding as on 31.3.2019 AND received on or after 1.4.2014 Auditor’s certificate is NOT mandatory. | E Form DPT 3 (One Time Return) |

| Companies Act, 2013 | 30.06.2019 | Transaction during the year, which are deposits as well as and which are not deposits (exempted deposits) Auditor’s Certificate is mandatory. This is to be filled every year. | E Form DPT 3 (Half Yearly Return) |

This article is updated till 31st May, 2019 with all Laws / Regulations and their respective amendments.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"