AAR Rejects Concessional GST Rate on Mining Lease Services; Upholds 18% GST on Mineral Extraction Royalty:

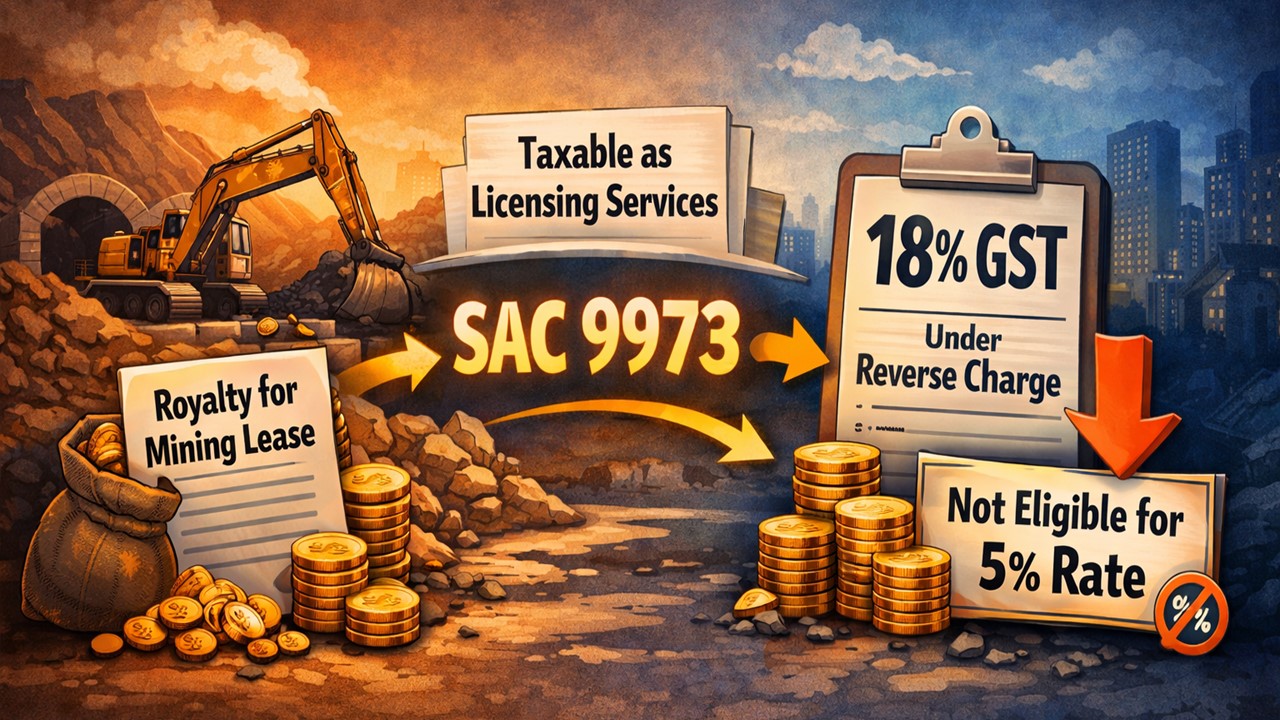

AAR held that royalty paid for a mining lease is taxable as licensing services under SAC 9973 at 18% GST under reverse charge and not eligible for the concessional 5% rate.

Mining Lease Royalty Attracts 18% GST Under Reverse Charge: AAR

Table of Contents

AAR Rejects Concessional GST Rate on Mining Lease Services; Upholds 18% GST on Mineral Extraction Royalty

The company, Ramandeep Upkarsingh Bindra (Black Rock Crusher), has filed an application dated August 19, 2020, seeking the Maharashtra Authority for Advance Ruling (AAR) under Section 97 of the Central Goods and Services Tax Act, 2017, and the Maharashtra Goods and Services Tax Act, 2017.

The applicant is registered under the Goods and Services Tax Act 2017 and has a registered address at Haladgaon, Panchgaon Road, Nagpur, Maharashtra, 440103. The applicant is engaged in the business of extracting minerals, crushing them, and then selling them.

The applicant wanted to obtain a mining lease from the state government for the exploration of minerals like black rock, stones, and other minerals against consideration in the form of royalty/dead rent to the state government. In the context of the same applicant, they entered into a lease transfer agreement. But the applicant obtained a title to the land under the mining operation through a sale agreement, enforced on April 29, 2015.

Questions Asked Before Maharashtra AAR:

The applicant has asked the following questions seeking the Maharashtra Authority for Advance Ruling (AAR): "Question 1. Whether the services of leasing of mines for which royalty is charged by the government merit classification under the heading No. 9973, specifically under subheading No. 997337 (licensing services for the right to use minerals, including their exploration and evaluation)? Question 2. Whether the said service can be classified under SL No. 17(iii) of the notification no. 11/2017 central tax (rate) dated 28/06/2017, attracting a rate of 5 per cent (the same rate of central tax as on the supply of like goods involving the transfer of title of goods)?"Answers Given by Maharashtra AAR:

The Maharashtra Authority for Advance Ruling (AAR) has given the following answers to the questions asked by the applicant: Answer 1: The royalty paid to the government in respect of the service of leasing of mines is a part of the consideration payable for the licensing services for the right to use minerals, including exploration and evaluation, falling under the Head 9973, which is liable to be taxed at 18% GST (9% CGST and 9% SGST) under the entry at Serial No. 17(viii) of the Notification No. 11/2017-Central Tax dated June 28, 2017. As services supplied by the government to a business located in the taxable territory are classified under the entry at Serial No. 17(viii) of the Notification No. 11/2017-Central Tax dated June 28, 2017, the recipient of such services becomes liable to pay tax on it under the reverse charge mechanism, as the licensing services are provided by the state government to a business entity, i.e., the applicant in the present case. Answer 2: As per the authority, the said service cannot be classified under serial no. 7(iii) of the notification no. 11/2017 central tax (rate) dated June 28, 2017, attracting GST at 5%.About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2489

2489My Recent Articles

- ITAT Rules in Taxpayer's Favour, Holds Delay in Filing Form 67 Cannot Be Sole Ground to Deny Foreign Tax CreditPremium

- ITAT Revives Tax Appeals for Six AYs After Finding Insufficient Hearing Time and Ignored Adjournment RequestPremium

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

- Trust’s Sections 12AB and 80G Registration Cannot Be Denied Before Charitable Project Is Completed, Holds ITATPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts