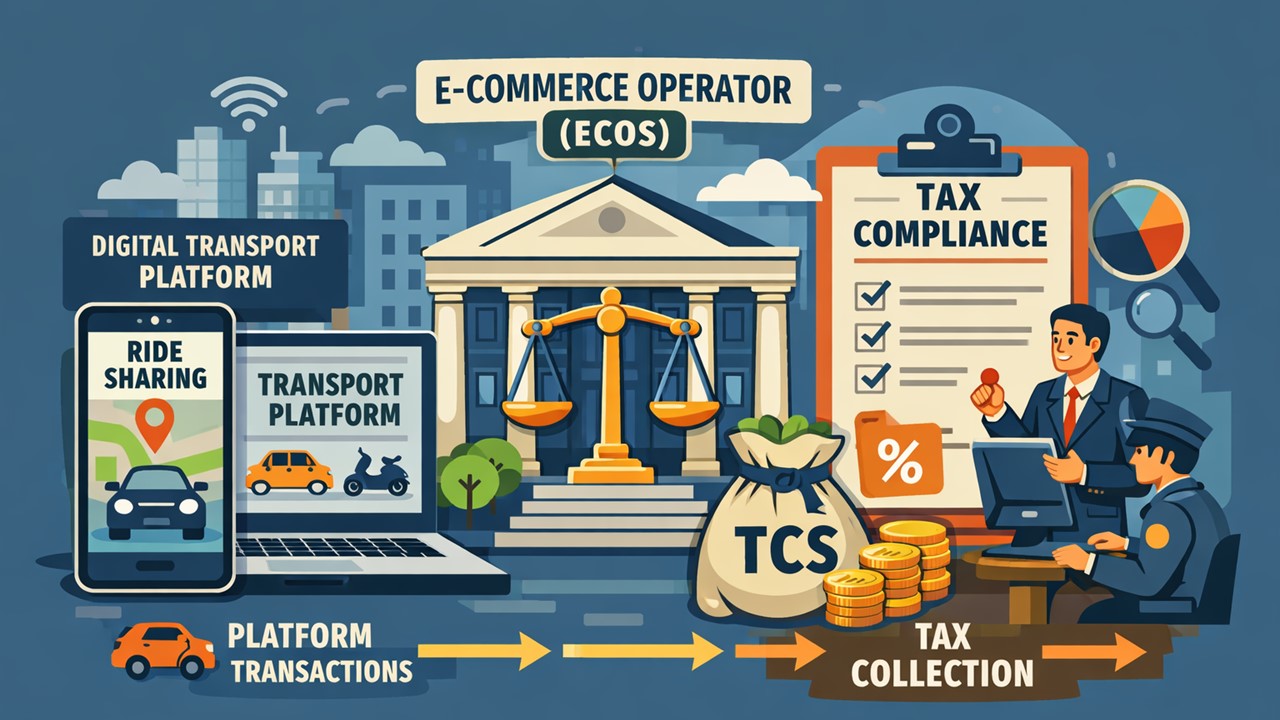

AAR Rules Digital Transport Facilitators As Ecos, Liable For TCS On Platform Transactions:

Digital Transport Platform Classified as E-Commerce Operator, TCS Liability Confirmed

Platform-based Transport Facilitators Treated As ECO, Not GTA Services

AAR Rules Digital Transport Facilitators As Ecos, Liable For TCS On Platform Transactions

The applicant in this matter developed a digital platform and mobile app designed to bridge the gap between customers and vehicle owners for goods transportation. A key factual point is that the applicant does not own a fleet or perform the actual transport; its role is strictly limited to facilitating bookings. For providing this digital infrastructure, it earns a commission from the transporters. Seeking to resolve its GST obligations, the applicant approached the Authority to determine whether it should be classified as a Goods Transport Agency (GTA) or an E-commerce Operator (ECO), and whether tax applies to the total freight or just the commission.

Upon reviewing the platform's operational model, the Authority highlighted that the applicant does not issue a "consignment note" which is the primary legal benchmark for GTA classification. Instead, the platform simply acts as a conduit for transactions between independent service providers and their clients.

Issue Raised: The central question was whether the applicant meets the definition of an E-commerce Operator under GST law and, consequently, whether it is mandated to collect Tax Collected at Source (TCS) under Section 52.

Tribunal's Ruling: The Authority ruled that the applicant functions as an E-commerce Operator (ECO) rather than a Goods Transport Agency. Because the business model revolves entirely around facilitating services via a digital interface, it falls squarely within the statutory definition of an ECO. As a result, GST is only applicable to the commission the applicant earns, not the gross freight charges paid by the customer.

Furthermore, as an ECO, the applicant is legally required to collect TCS on the net value of all supplies processed through its platform. The ruling also mandates full compliance with related procedural duties, including the consistent filing of all prescribed returns under the GST framework.

To Read Full Order, Download PDF Given Below

About Author

Meetu Kumari

Content Manager

Meetu Kumari is an Experienced Advocate and Content Writer with 4+ years of demonstrated history of working in the law practice industry. Skilled in Developing Content, Researching, and Drafting. Strong professional with a Bachelor of Science (B.Sc.) focused on Law from Gujarat National Law University.

Meetu Kumari is an Experienced Advocate and Content Writer with 4+ years of demonstrated history of working in the law practice industry. Skilled in Developing Content, Researching, and Drafting. Strong professional with a Bachelor of Science (B.Sc.) focused on Law from Gujarat National Law University.

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2260

2260My Recent Articles

- ITAT Quashes Reassessment Over Unsigned Section 148 Notice Issued to AssesseePremium

- ITAT Sends Software and SaaS FTS Dispute Back for Fresh Review, Rules DTAA Tax Capping Includes Surcharge and CessPremium

- ITAT Orders Entity-Level Benchmarking for McCain India’s Transfer Pricing DisputePremium

- ITAT Deletes Rs 8.49 Crore Additions, Says CIT(A) Can Admit Evidence to Grant ReliefPremium

- ITAT Restores Appeal After Condoning Delay, Says Substantial Justice Must Prevail Over TechnicalitiesPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts