All About Form "ITR-U" or Updated Return

All About Form "ITR-U" or Updated Return This article discusses the Filing of ITR Form " ITR-U " or Updated Return. ITR 1 to 7 (as applicable) is to …

Table of Contents

All About Form "ITR-U" or Updated Return

This article discusses the Filing of ITR Form "ITR-U" or Updated Return. ITR 1 to 7 (as applicable) is to be filed along with the ITR-U for AY 2020-21, AY 21-2022, and subsequent years.

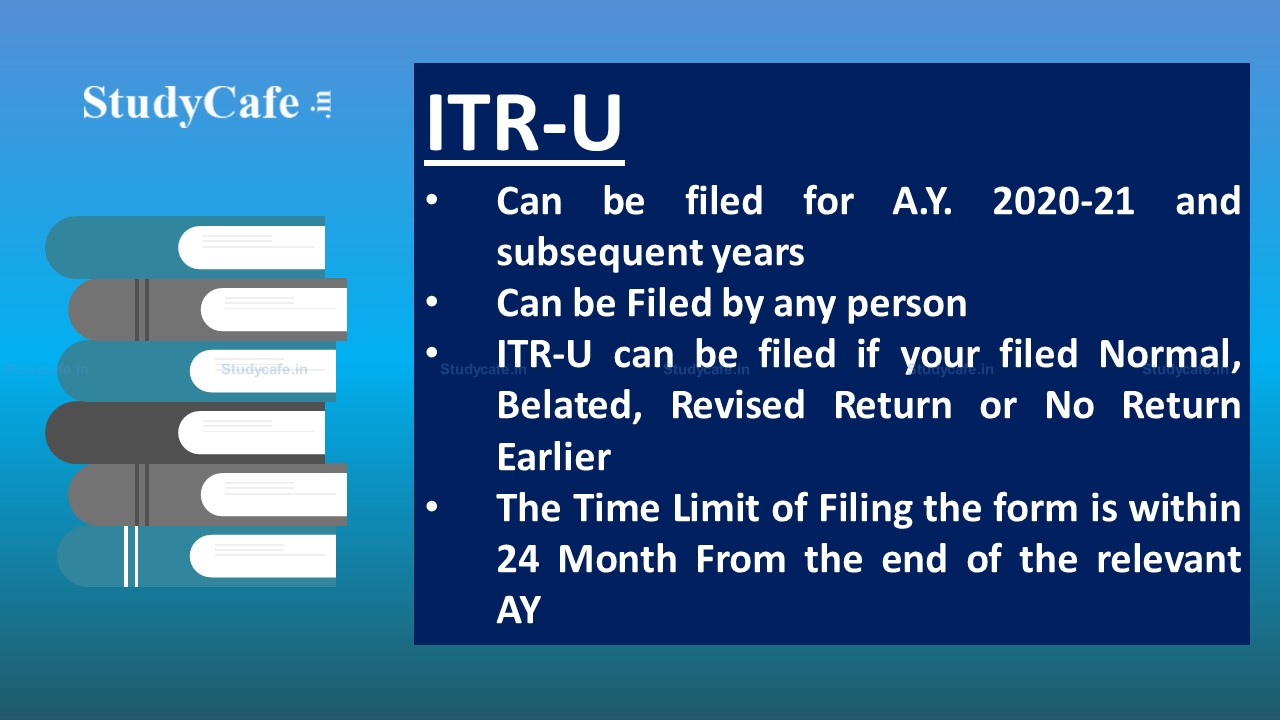

Updated Return ("ITR-U") can be filed for which Assessment Year?

It can be filed for Assessment Year (A.Y.) 2020-21, AY 21-2022, and subsequent yearsWho can file it?

Any PersonIf Return is filed u/s 139 (1) or (4) or (5), can we file an updated return or ITR-U?

Yes, ITR-U can be filed if you filed Normal, Belated, or Revised Return Earlier.Can a file Fresh Return, if no Income Tax Return ("ITR") was filed earlier?

Yes, you can file it as Fresh Return u/s 139(8A).What is the Time Limit for Filing this Form?

The Time Limit of Filing the form is within 24 Month From the end of the relevant A. Y.When I am not eligible to File an Updated Return?

- If it is a Return of a loss

- If it has an effect of decreasing the total tax liability determined on the basis of earlier return filed

- If it results in the refund or increases the refund due on the basis of return filed earlier

What are the various Reasons for updating your Income Tax Return?

- Return previously not filed

- Income not reported correctly

- Wrong heads of income chosen

- Reduction of carried forward loss

- Reduction of unabsorbed depreciation

- Reduction of tax credit u/s 115JB/115JC

- Wrong rate of tax

- Others

- 25% of the aggregate of tax and interest payable, after the expiry of the time available u/s 139(4) or (5) and before completion of the period of 12 months from the end of the relevant A.Y. or

- 50% of the aggregate of tax and interest payable, after the expiry of 12 months from the end of the relevant A.Y. but before completion of the period of 24 months from the end of the relevant A.Y.

Is Interest u/s 234A/234B/234C applicable?

YesAbout Author

Sushmita Goswami

Content Manager

Sushmita Goswami is a content writer with 2+ years of experience in Finance, Recruitment, Education and career Related Content. She is a Graduate from Delhi University in Journalism and Mass Communication

Sushmita Goswami is a content writer with 2+ years of experience in Finance, Recruitment, Education and career Related Content. She is a Graduate from Delhi University in Journalism and Mass Communication

Studycafe

Studycafe  New Delhi , Delhi, India

New Delhi , Delhi, India 886

886My Recent Articles

- What to Consider When Choosing an Online Trading Platform?

- Post Office Franchise Scheme: Take Post Office Franchise at Rs 5000 and Earn Commission upto 20%; Check Details Here

- IAN invests INR 4.5 crore in Fintech NBFC Indium Finance

- UPI a Digital Public Good, No Charges in Consideration: Finance Ministry

- ITR Filing Penalty: Check Taxpayers Exempt from Paying a Late Fee even Missing the Deadline

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts