Amendment to CGST Rules : Due date of filing Tran 1 Extended in certain cases

Amendment to CGST Rules : Due date of filing Tran 1 Extended in certain cases CBIC has again notified amendment to CGST Rules. So Summary of

Amendment to CGST Rules : Due date of filing Tran 1 Extended in certain cases

CBIC has again notified amendment to CGST Rules.

So Summary of The amendment are as follows:

1. Due date of filing Tran 1 has been Extended to 30th March, 2020 in certain cases where recommendations of GST the Council has been provided. Similarly Due Date of Filing Tran 2 has been extended to 30th April, 2020 in those cases.

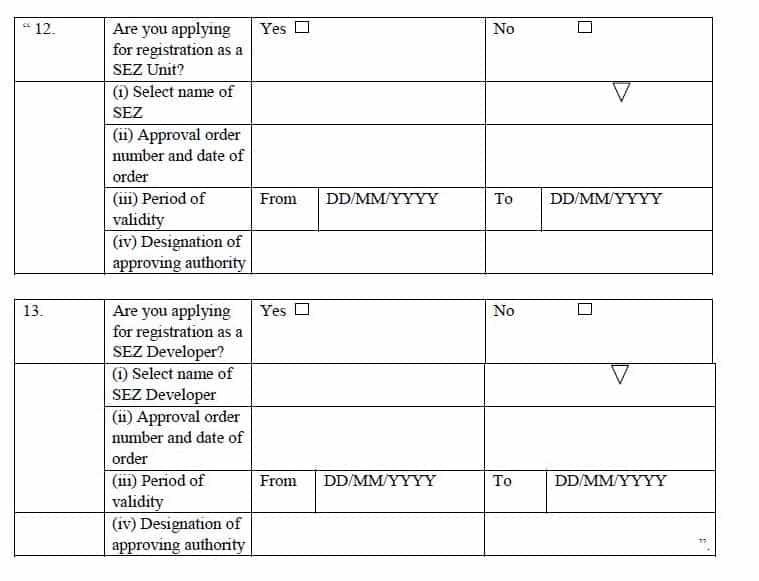

2. Changes made in Form FORM REG-01 when Registration application is made as SEZ Unit. Now you need to provide Period of validity. Same was not there earlier.

3. Changes made in FORM GSTR-3A, Notice to Return Defaulter.

4. Changes made in Form INV-01.

Click here to Discuss the Notification

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]

4. In the said rules, in FORM GSTR-3A,-

(a) in serial number 2 under the heading “Notice to Return Defaulter u/s 46 for not filing Return”, for the words “tax liability will” , the words “tax liability may” shall be substituted;

(b) after serial number 4 under the heading “Notice to Return Defaulter u/s 46 for not filing Return” , the following serial number shall be inserted, namely:-

“5. This is a system generated notice and does not require signature.”;

(c) in serial number 3 under the heading “Notice To Return Defaulter U/S 46 For Not Filing Final Return Upon Cancellation Of Registration”, for the words “tax period will”, the words “tax period may” shall be substituted;

(d) after serial number 4 under the heading “Notice To Return Defaulter U/S 46 For Not Filing Final Return Upon Cancellation Of Registration” , the following serial number shall be inserted, namely:-

“5. This is a system generated notice and does not require signature.”.

5. In the said rules, for FORM INV-01, the following form shall be substituted, namely:-

“Note: Cardinality Means occurance of field in the schema. Below are the the meaning of various symbol used in this column:

0..1 : It means this item is optional and even if mentioned can not be repeated 1..1: It means that this item is mandatory and can be mentioned only once.

1..n: It means this item is mandatory and can be repeated more than once

0..n: It means this item is optional but can be repated many times. For example: Previous invoice reference is optional but if required one can mention many previous invoice reference.

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

Click here to read the whole notification

Tags : GST, GST Notification

For Regular Updates Join : https://t.me/Studycafe

4. In the said rules, in FORM GSTR-3A,-

(a) in serial number 2 under the heading “Notice to Return Defaulter u/s 46 for not filing Return”, for the words “tax liability will” , the words “tax liability may” shall be substituted;

(b) after serial number 4 under the heading “Notice to Return Defaulter u/s 46 for not filing Return” , the following serial number shall be inserted, namely:-

“5. This is a system generated notice and does not require signature.”;

(c) in serial number 3 under the heading “Notice To Return Defaulter U/S 46 For Not Filing Final Return Upon Cancellation Of Registration”, for the words “tax period will”, the words “tax period may” shall be substituted;

(d) after serial number 4 under the heading “Notice To Return Defaulter U/S 46 For Not Filing Final Return Upon Cancellation Of Registration” , the following serial number shall be inserted, namely:-

“5. This is a system generated notice and does not require signature.”.

5. In the said rules, for FORM INV-01, the following form shall be substituted, namely:-

“Note: Cardinality Means occurance of field in the schema. Below are the the meaning of various symbol used in this column:

0..1 : It means this item is optional and even if mentioned can not be repeated 1..1: It means that this item is mandatory and can be mentioned only once.

1..n: It means this item is mandatory and can be repeated more than once

0..n: It means this item is optional but can be repated many times. For example: Previous invoice reference is optional but if required one can mention many previous invoice reference.

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

Click here to read the whole notification

Tags : GST, GST Notification

For Regular Updates Join : https://t.me/Studycafe

Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs

Notification No. 02/2020 – Central Tax

New Delhi, the 01st January, 2020

G.S.R……(E). - In exercise of the powers conferred by section 164 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government hereby makes the following rules further to amend the Central Goods and Services Tax Rules, 2017, namely:- 1. (1) These rules may be called the Central Goods and Services Tax (Amendment) Rules, 2020. (2) Save as otherwise provided in these rules, they shall come into force on the date of their publication in the Official Gazette. 2. In the Central Goods and Services Tax Rules, 2017 (hereinafter referred to as the said rules), in rule 117,- (a) in sub-rule (1A), with effect from the 31st December 2019, for the figures, letters and word “31st December, 2019”, the figures, letters and word “31st March, 2020” shall be substituted; (b) in sub-rule (4), in clause (b), in sub-clause (iii), in the proviso, for the figures, letters and word “31st January, 2020”, the figures, letters and word “30th April, 2020” shall be substituted. 3. In the said rules, in FORM REG-01, in Part-B, for serial numbers 12 and 13 and the entries relating thereto, the following shall be substituted, namely:-

4. In the said rules, in FORM GSTR-3A,-

(a) in serial number 2 under the heading “Notice to Return Defaulter u/s 46 for not filing Return”, for the words “tax liability will” , the words “tax liability may” shall be substituted;

(b) after serial number 4 under the heading “Notice to Return Defaulter u/s 46 for not filing Return” , the following serial number shall be inserted, namely:-

“5. This is a system generated notice and does not require signature.”;

(c) in serial number 3 under the heading “Notice To Return Defaulter U/S 46 For Not Filing Final Return Upon Cancellation Of Registration”, for the words “tax period will”, the words “tax period may” shall be substituted;

(d) after serial number 4 under the heading “Notice To Return Defaulter U/S 46 For Not Filing Final Return Upon Cancellation Of Registration” , the following serial number shall be inserted, namely:-

“5. This is a system generated notice and does not require signature.”.

5. In the said rules, for FORM INV-01, the following form shall be substituted, namely:-

“Note: Cardinality Means occurance of field in the schema. Below are the the meaning of various symbol used in this column:

0..1 : It means this item is optional and even if mentioned can not be repeated 1..1: It means that this item is mandatory and can be mentioned only once.

1..n: It means this item is mandatory and can be repeated more than once

0..n: It means this item is optional but can be repated many times. For example: Previous invoice reference is optional but if required one can mention many previous invoice reference.

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

Click here to read the whole notification

Tags : GST, GST Notification

For Regular Updates Join : https://t.me/StudycafeAbout Author

Pratibha Goyal

Admin

This Account belongs to Admistrator of Studycafe.

This Account belongs to Admistrator of Studycafe.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts